|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

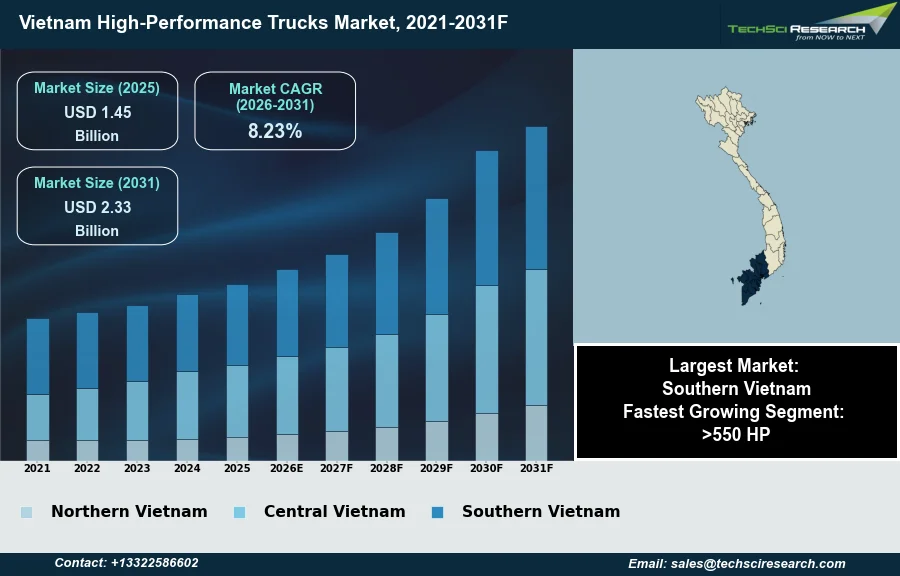

Market Size (2025)

|

USD 1.45 Billion

|

|

CAGR (2026-2031)

|

8.23%

|

|

Fastest Growing Segment

|

>550 HP

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 2.33 Billion

|

Market Overview

The Vietnam High-Performance Trucks Market will grow from USD 1.45 Billion in 2025 to USD 2.33 Billion by 2031 at a 8.23% CAGR. High-performance trucks are robust commercial vehicles engineered for superior power, durability, and efficiency, primarily deployed in demanding applications such as long-haul logistics, heavy construction, and specialized transport. The market's expansion is fundamentally supported by the government's substantial infrastructure development initiatives, including investments exceeding USD 10 billion in 2024 for transport projects, fostering demand for heavy-duty solutions. Simultaneously, Vietnam's increasing role as a manufacturing hub for diverse goods directly elevates the need for efficient and high-capacity freight movement.

The proliferation of e-commerce further propels this demand by necessitating faster and more reliable supply chain operations. According to the Vietnam Automobile Manufacturers' Association, in 2025, truck sales reached 70,746 units, indicating robust market activity. However, a significant impediment to market growth is the high initial acquisition cost of these advanced vehicles, which, coupled with stringent financing requirements, restricts accessibility for a large segment of small and medium-sized fleet operators.

Key Market Drivers

Public Investment and Infrastructure Development Drive High-Performance Truck Demand

Infrastructure development and substantial government investment are primary catalysts for the Vietnam High-Performance Trucks Market. The government's strategic focus on upgrading and expanding national transportation networks, including expressways and major transport corridors, directly fuels demand for heavy-duty and specialized trucks essential for construction and material logistics. These vehicles are critical for handling large volumes of materials and equipment. According to the Vietnam Investment Review, in May 2026, the Prime Minister assigned nearly $39.8 billion in state budget-funded public investment for 2026, marking a record high for the sector. This sustained investment ensures consistent requirement for high-performance trucks in national projects, driving fleet modernization.

Industrial Growth and Manufacturing Activity Drive Heavy-Duty Truck Demand

Complementing infrastructure advancements, Vietnam's rapid industrial growth and its manufacturing hub status significantly propel the high-performance trucks market. Expanding manufacturing output, particularly in sectors requiring efficient freight movement for raw materials and finished goods, necessitates a reliable fleet of high-capacity vehicles. As industries mature, demand for trucks capable of handling diverse cargo and meeting stringent delivery schedules intensifies. According to the National Statistics Office, in June 2026, Vietnam's Industrial Production Index (IIP) rose 9.1 percent year-on-year for the first five months of 2026, indicating robust manufacturing activity. This industrial vigor underpins the consistent need for heavy-duty transportation. Overall, cumulative vehicle sales across Vietnam reached 156,729 units from January through May 2026, representing approximately 22% growth compared to the same period in 2025.

Download Free Sample Report

Key Market Challenges

Financing barriers and high upfront costs constrain SME fleet modernization

The high initial acquisition cost of advanced high-performance trucks, coupled with stringent financing requirements, represents a significant impediment to market growth in Vietnam. This financial barrier directly restricts accessibility for a large segment of small and medium-sized fleet operators, thereby limiting their capacity to modernize and expand their vehicle fleets. These operators often face challenges in securing the substantial upfront capital or meeting the strict eligibility criteria for loans necessary to acquire such expensive, specialized vehicles. Consequently, this constrains their ability to undertake demanding applications like long-haul logistics or heavy construction, even amidst rising infrastructure development and manufacturing activities.

High acquisition costs limit high-performance truck uptake despite overall commercial-vehicle market growth

While the broader market for commercial vehicles exhibits strong activity, the prohibitive cost structure for high-performance models limits their penetration among smaller enterprises. According to the Vietnam Automobile Manufacturers' Association (VAMA), commercial vehicle deliveries in 2025 increased by almost 25% to 94,385 units. Despite this overall growth, the high acquisition costs continue to suppress demand from a crucial demographic of fleet operators, preventing them from upgrading to more powerful and efficient trucks and consequently hindering the full potential expansion of the high-performance truck segment.

Key Market Trends

Rising Electrification of High-Performance Trucks

The Vietnam High-Performance Trucks market is observing an accelerated adoption of electric and hybrid powertrains. This trend stems from increasing environmental awareness, supportive government incentives, and fleet operators recognizing long-term operational cost savings from reduced fuel consumption and maintenance. Despite higher initial acquisition costs, expanding charging infrastructure and technological advancements enhance viability, especially for urban logistics and specialized transport. According to VietNamNet, in June 2026, citing the Deputy Director of the Department of Transport and Traffic Safety under the Ministry of Construction, Vietnam had 3,396 electric trucks in operation as of the end of May 2026. This growing fleet indicates a clear movement towards sustainable trucking solutions.

Expansion of Telematics and Digital Logistics Solutions

Concurrently, the increasing integration of advanced telematics and digital platforms presents another significant trend. This adoption is driven by the imperative for enhanced operational efficiency, real-time tracking, optimized route planning, and predictive maintenance, all contributing to streamlined supply chains. These technologies provide fleet managers with granular insights into vehicle performance and driver behavior, reducing costs and improving delivery reliability. Government initiatives for digital transformation in logistics further accelerate this trend. According to Viet Nam Government News, in October 2025, in the 'Gov't approves logistics services development strategy towards 2025' report, 80 percent of logistics enterprises are expected to adopt digital transformation solutions by 2025. This underscores a firm commitment to modernizing logistical operations through digital tools.

Segmental Insights

Infrastructure growth and logistics demand drive the >550 HP segment

The >550 HP segment is projected to be the fastest-growing power output category within the Vietnam High-Performance Trucks Market. This accelerated growth is primarily driven by the nation's ambitious infrastructure development agenda, exemplified by major projects such as the North-South Expressway and new international airports, which necessitate heavy-duty transport for construction materials and equipment. Furthermore, Vietnam's emergence as a significant manufacturing hub, coupled with evolving logistics demands, intensifies the need for high-capacity, high-torque trucks essential for efficient long-haul and inter-provincial freight movement. Government initiatives, including the National Master Plan on Logistics Development, also advocate for enhanced transport efficiency, further stimulating demand for these powerful vehicles.

Regional Insights

Southern Vietnam's Industrial and Logistics Backbone Fuels High-Performance Truck Demand

Southern Vietnam dominates the high-performance trucks market, primarily driven by its robust industrial base and dense logistics infrastructure, anchored by major economic hubs such as Ho Chi Minh City, Binh Duong, Dong Nai, and Ba Ria–Vung Tau. The region is home to Vietnam's busiest ports, including Cat Lai and Cai Mep–Thi Vai, which manage the majority of the nation's containerized freight movement. These extensive operations, combined with the region's significant manufacturing activities and high consumption centers, necessitate advanced, high-capacity transport solutions. Strategic infrastructure investments by the Vietnamese government, under the guidance of bodies like the Ministry of Transport, further enhance regional connectivity and fuel the demand for efficient trucking.

Recent Developments

-

In December 2025, SHACMAN successfully delivered 102 X3000 8×4 heavy-duty dump trucks to a leading Vietnamese conglomerate. This delivery reinforced a decade-long strategic partnership, solidifying SHACMAN's position as a preferred heavy-duty truck provider for infrastructure development in Vietnam. The X3000 models feature a 400+ HP powertrain with 15% better fuel efficiency compared to previous versions, along with a next-generation comfort cab and a U-shaped wear-resistant tipper body. These high-performance trucks are immediately deployed for road, highway, airport, and urban high-rise construction projects, catering to Vietnam's expanding infrastructure needs.

-

In April 2025, Volvo Trucks, in collaboration with its exclusive distributor T&C Trucks, enhanced its presence in the Vietnam high-performance trucks market by introducing new heavy-duty Volvo truck models, including the Volvo T62 and T64. This strategic partnership aims to advance the domestic transport industry by providing solutions focused on efficiency, safety, and sustainability. The launched trucks feature advanced technology and modern interiors, designed for exceptional operational performance. T&C Trucks emphasized building a robust service foundation, including European-standard service centers and internationally trained technicians, to support these high-performance vehicles and optimize customer operational efficiency.

-

In October 2024, Hino Motors Vietnam launched its XZU Euro5 truck at its factory, signifying a crucial milestone in providing environmentally compliant products for the Vietnam high-performance trucks market. This domestically assembled model meets stringent Euro5 emission standards and integrates the Hino-connect telematics vehicle management system. The system enables businesses to monitor and manage fleets more efficiently, analyze driving behaviors, and ensure optimal vehicle operation. The introduction of the Hino XZU Euro5 underscores Hino Motors Vietnam's dedication to sustainable growth in the automotive industry by offering technologically advanced and environmentally friendly trucking solutions.

-

In January 2024, VinFast, a prominent Vietnamese electric vehicle manufacturer, unveiled its VF Wild electric pickup truck concept at CES 2024. This marked the company's first foray into the pickup truck segment, showcasing an innovative effort to create a vehicle with exceptional performance. Developed in collaboration with Australian design studio GoMotiv, the mid-size concept featured a flexible bed expanding from 5 to 8 feet and a distinctive "Fluid Dynamism" aesthetic. The VF Wild demonstrates VinFast's commitment to expanding its product range and promoting sustainable mobility within the Vietnam high-performance trucks market by targeting consumers seeking eco-friendliness without compromising durability.

Key Market Players

- Thaco (Truong Hai Auto Corporation)

- Hyundai Motor Company

- Isuzu Motors Limited

- Hino Motors Ltd.

- Fuso (Mitsubishi Fuso Truck and Bus Corporation)

- UD Trucks

- Volvo Trucks

- Scania AB

- Dongfeng Motor Corporation

- Tata Motors

|

By Vehicle Type

|

By Power Output

|

By Transmission Type

|

By Region

|

- Light Duty Truck

- Medium Duty Truck

- Heavy Duty Truck

|

- 250-400 HP

- 401-550 HP

- >550 HP

|

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam High-Performance Trucks Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam High-Performance Trucks Market, By Vehicle Type:

-

Light Duty Truck

-

Medium Duty Truck

-

Heavy Duty Truck

-

Vietnam High-Performance Trucks Market, By Power Output:

-

250-400 HP

-

401-550 HP

-

>550 HP

-

Vietnam High-Performance Trucks Market, By Transmission Type:

-

Vietnam High-Performance Trucks Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam High-Performance Trucks Market.

Available Customizations:

Vietnam High-Performance Trucks Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam High-Performance Trucks Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com