|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 5.67 Billion

|

|

CAGR (2026-2031)

|

6.19%

|

|

Fastest Growing Segment

|

Replacement

|

|

Largest Market

|

Dubai

|

|

Market Size (2031)

|

USD 8.13 Billion

|

Market Overview

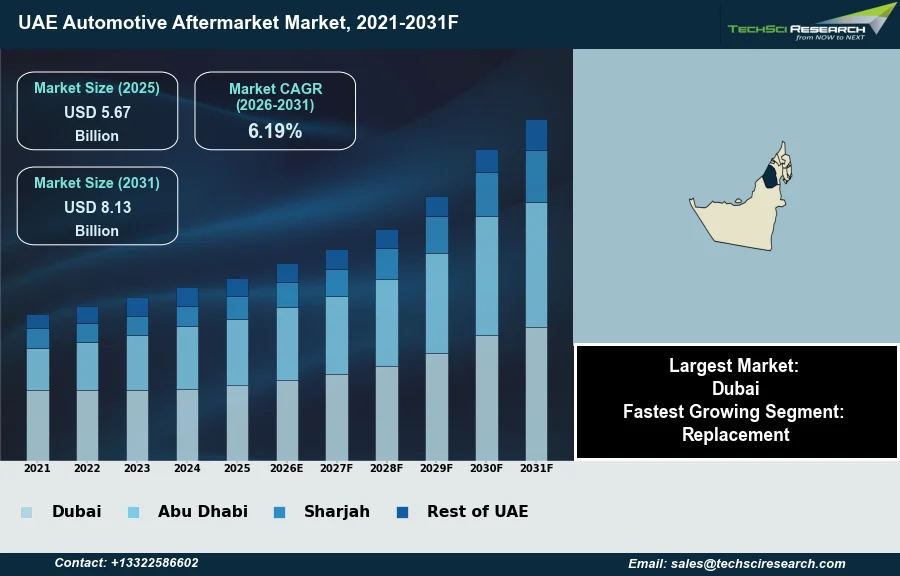

The UAE Automotive Aftermarket Market will grow from USD 5.67 Billion in 2025 to USD 8.13 Billion by 2031 at a 6.19% CAGR. The UAE Automotive Aftermarket Market encompasses the manufacturing, remanufacturing, distribution, retailing, and installation of all vehicle parts, equipment, and other accessories and services following the original sale of an automobile by the original equipment manufacturer to the consumers. This market's expansion is fundamentally driven by several factors, including the increasing vehicle parc and ownership rates, robust economic growth, and the necessity for consistent vehicle maintenance due to the region's demanding climatic conditions. According to AutoData UAE, in the first half of 2025, new car registrations rose to approximately 157,000 units, representing an 11% year-on-year increase, directly contributing to the demand for aftermarket services and parts.

Further supporting market growth are heightened consumer preferences for vehicle customization and an expanding average vehicle age, which necessitates more frequent repairs and component replacements. However, a significant challenge that could impede market expansion is the accelerating depreciation of vehicles. According to DubiCars' UAE Automotive Market Report, looking ahead to 2026, depreciation across the UAE's automotive ecosystem is projected to accelerate, implying an additional annual value erosion of over AED 150 million.

Key Market Drivers

Rising vehicle parc and aging fleets drive aftermarket demand

The expanding vehicle parc and aging fleet significantly fuel the UAE automotive aftermarket. As the number of vehicles on the roads increases and their average age rises, the demand for replacement parts and routine maintenance intensifies. Older vehicles typically require more frequent servicing and component replacements, creating a consistent revenue stream. This trend is bolstered by a thriving used car market, introducing a substantial volume of vehicles requiring post-sale attention. According to ArabWheels, January 01 2026, in the 'The $337M Surge: UAE Solidifies Position in Used Korean Cars Trade' report, the total value of used-vehicle shipments to the UAE reached approximately $337 million during the first 10 months of 2025, indicating a significant inflow that drives aftermarket activity.

Harsh UAE climate accelerates wear, sustaining aftermarket needs

Harsh climatic conditions in the UAE represent another critical driving factor, accelerating wear and tear on various vehicle components. High temperatures and sandy environments place considerable stress on systems like air conditioning, batteries, and tires, necessitating frequent inspections, repairs, and replacements. For example, the demanding climate directly impacts essential systems. According to META MECHANICS, June 16 2025, in 'AC Repair Services in Dubai: What's the Real Cost in 2025?', typical AC compressor repair or replacement costs range from AED 800 to AED 2,500+ in Dubai, highlighting a substantial and recurring aftermarket need. This consistent demand for upkeep is further reflected in broader vehicle utilization. According to dubizzle, in August 2025, Dubai's taxi sector recorded a 7% increase in total trips during the first half of 2025, rising from 55.7 million in H1 2024 to 59.5 million, underscoring constant operational demands and corresponding aftermarket support requirements.

Download Free Sample Report

Key Market Challenges

Impact of Vehicle Depreciation on Aftermarket Spending

A significant challenging factor impeding the expansion of the UAE Automotive Aftermarket Market is the accelerating depreciation of vehicles. This rapid decline in vehicle value directly impacts consumer behavior and investment in aftermarket services. When vehicles depreciate at an accelerated rate, owners often perceive diminished value in allocating substantial funds towards comprehensive maintenance, costly repairs, or premium component replacements. This inclination leads to a shorter vehicle ownership cycle or a preference for more economical, and often lower-quality, aftermarket solutions.

Depreciation-Driven Replacement and Minimal Maintenance Trends

This dynamic curtails the revenue potential for businesses specializing in high-value parts, advanced diagnostics, and extensive repair services. For instance, according to the Roads and Transport Authority (RTA), registered vehicles in the UAE reached 4.56 million by June 2025, indicating a 9.35% year-on-year increase. Despite this growing vehicle parc, the accelerated depreciation encourages owners to either replace their vehicles sooner to mitigate further financial losses or to defer non-essential maintenance. This shifts demand away from long-term vehicle care towards minimal upkeep, directly challenging the growth and profitability of the comprehensive automotive aftermarket sector.

Key Market Trends

Digitalization of aftermarket service channels and growing consumer expectations

The digitalization of aftermarket service channels is profoundly transforming how vehicle owners engage with maintenance and repair providers, driven by demands for convenience and transparency. This trend encompasses online booking, mobile applications, digital inspections, and real-time service tracking, all streamlining the customer journey. This pervasive shift is clearly evidenced by the Roads and Transport Authority (RTA), which generated AED 5.3 billion in revenue through its digital channels in 2025, a 20.6% increase from 2024. Such growth underscores the necessity for aftermarket participants to invest in robust digital infrastructure to meet evolving consumer expectations.

EV adoption drives specialized aftermarket capabilities

The significant expansion of electric vehicle (EV) adoption represents a pivotal trend reshaping the UAE automotive aftermarket, demanding specialized service expertise. EVs require distinct maintenance protocols, including advanced diagnostics for high-voltage systems, battery management, and software updates, differentiating them from conventional servicing. Consequently, aftermarket providers must invest in specialized tools, charging infrastructure, and comprehensive technician training for this emerging segment. This rapid acceleration is evidenced by the electric vehicle market’s substantial 41 percent year-on-year surge in the first half of 2025, with Dubai alone recording over 40,600 registrations. This growing EV parc directly necessitates a sophisticated, technologically adept aftermarket ecosystem.

Segmental Insights

Key Growth Drivers for the Replacement Segment

The Replacement segment is a primary driver within the UAE Automotive Aftermarket Market, experiencing rapid expansion due to several specific factors. The consistent increase in vehicle ownership and the growing average age of vehicles on the road inherently heighten the demand for routine maintenance and part replacements. Furthermore, the UAE's distinct harsh climatic conditions, characterized by high temperatures and prevalent dust, significantly accelerate the wear and tear of essential vehicle components such as tires, batteries, and filters, thereby necessitating more frequent replacements to ensure operational longevity and safety. This sustained need, coupled with the robust economic environment enabling consumers to invest in vehicle upkeep, fuels the segment's accelerated growth.

Regional Insights

Dubai’s logistics and commercial hub underpins the UAE automotive aftermarket.

Dubai leads the UAE Automotive Aftermarket Market due to its status as a significant commercial and logistics hub, supported by extensive infrastructure and a robust distribution network for automotive components. High vehicle ownership rates, driven by sustained economic growth and population expansion, consistently drive demand for maintenance and replacement parts, including luxury components. The emirate’s conducive business environment attracts both local and international automotive entities, stimulating market competition and innovation. Furthermore, regulatory bodies such as the Roads and Transport Authority (RTA) and Emirates Authority for Standardization and Metrology (ESMA) establish and enforce frameworks for vehicle maintenance and modifications, contributing to market integrity.

Recent Developments

-

In December 2025, Buyparts24, a digital platform for automotive spare parts, announced a strategic joint venture with BSG Auto Parts at Automechanika Dubai. This partnership was structured to enhance product offerings for the UAE's existing vehicle fleet, emphasizing high-quality aftermarket brands, and to broaden the distribution of BSG Auto Parts' private label brands. The collaboration sought to accelerate market growth, expand regional presence across the GCC, and establish new standards for efficiency and customer experience within the UAE automotive aftermarket sector.

-

In October 2025, DP World’s National Industries Park revealed a partnership with Cars24 for the development of a substantial automotive refurbishment facility in Dubai, involving an investment of AED 55 million. Construction was slated to commence in November 2025, with operations projected to begin in August 2026. This 220,000 sq. ft. solar-powered facility was designed to process over 100,000 vehicles annually. The project aimed to address increasing demand from electric vehicle manufacturers and Chinese OEMs, bolstering after-sales support and refurbishment capabilities within the UAE automotive aftermarket.

-

In December 2024, AISIN Middle East introduced its new eco-friendly tire brand, AITERRA, during Automechanika Dubai. This product launch was accompanied by a display of various aftermarket components, including wiper blades, lubricants, batteries, tire accessories, and e-mobility tools. The initiative aimed to expand the company's comprehensive service offerings across the UAE automotive aftermarket, demonstrating a strategic commitment to delivering innovative and high-quality solutions for the region's diverse vehicle requirements. This introduction solidified their market position within the competitive UAE landscape.

-

In May 2024, VinFast Auto formally established an exclusive dealership agreement with Al Tayer Motors, a prominent automotive dealership in the UAE. This collaboration was centered on the distribution of VinFast electric vehicles (EVs) throughout the country. The partnership represented a key development for the UAE automotive aftermarket, anticipating increased demand for EV-specific parts, specialized maintenance, and related services as the adoption of electric vehicles accelerated across the Emirates. This strategic alliance aimed to address the evolving landscape of sustainable transportation in the region.

Key Market Players

- Al Futtaim Automotive

- Al Habtoor Motors

- Al Tayer Motors

- Emirates Motors

- Premier Motors

- Auto Spare Parts UAE

- Midas UAE

- Bosch Auto Service UAE

- Euromaster UAE

- Sasoo Auto Parts

|

By Vehicle Type

|

By Component

|

By Demand Category

|

By Region

|

- Passenger Cars

- Commercial Vehicles

|

- Tires

- Spark Plugs

- Air Filter

- Fuel Filter

- Brake Pad

- Brake Shoe

- Brake Calliper

- Batteries

- Others

|

|

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

|

Report Scope:

In this report, the UAE Automotive Aftermarket Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

UAE Automotive Aftermarket Market, By Vehicle Type:

-

Passenger Cars

-

Commercial Vehicles

-

UAE Automotive Aftermarket Market, By Component:

-

Tires

-

Spark Plugs

-

Air Filter

-

Fuel Filter

-

Brake Pad

-

Brake Shoe

-

Brake Calliper

-

Batteries

-

Others

-

UAE Automotive Aftermarket Market, By Demand Category:

-

UAE Automotive Aftermarket Market, By Region:

-

Dubai

-

Abu Dhabi

-

Sharjah

-

Rest of UAE

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the UAE Automotive Aftermarket Market.

Available Customizations:

UAE Automotive Aftermarket Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

UAE Automotive Aftermarket Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com