|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

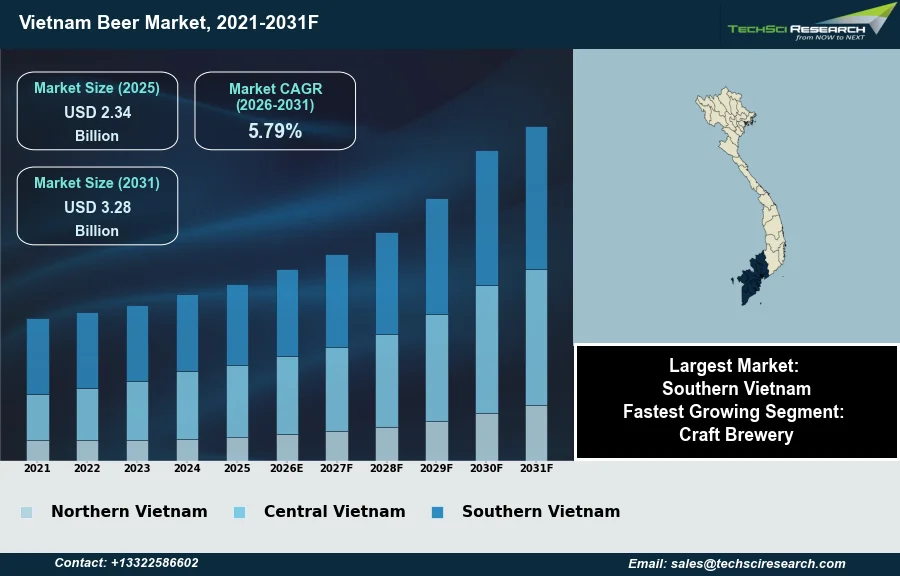

Market Size (2025)

|

USD 2.34 Billion

|

|

CAGR (2026-2031)

|

5.79%

|

|

Fastest Growing Segment

|

Craft Brewery

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 3.28 Billion

|

Market Overview

The Beer Market in Vietnam will grow from USD 2.34 Billion in 2025 to USD 3.28 Billion by 2031 at a 5.79% CAGR. Beer is a fermented alcoholic beverage typically produced from water, malted barley, hops, and yeast. The Vietnam Beer Market continues to experience significant expansion, driven by a confluence of factors including a large and youthful population, steadily rising disposable incomes, and the deep cultural integration of beer consumption into social gatherings and daily life. Rapid urbanization further supports market growth by expanding modern retail channels and consumption occasions. According to Kirin Holdings, in 2024, Vietnam consumed 4.6 billion liters of beer, positioning it as the eighth largest beer-consuming country globally.

However, the market faces notable impediments to its sustained growth. One significant challenge is the increasing regulatory pressure, particularly stringent excise taxes and the strict enforcement of drunk-driving laws, such as Decree 100. These measures elevate product costs for consumers and influence consumption patterns, potentially constraining overall market expansion.

Key Market Drivers

Rising incomes and middle-class growth expand premium beer demand

Growing disposable incomes and the expansion of the middle class significantly bolster the Vietnam Beer Market. As the economic prosperity of Vietnamese citizens rises, consumers possess greater discretionary funds, enabling them to purchase higher-priced and more diverse beer products. This enhanced purchasing power directly translates into increased consumption frequency and a willingness to explore premium offerings beyond traditional mass-market brands. According to VietNamNet, in January 2026, Vietnam's GDP per capita reached approximately USD 5,026, representing an increase of USD 326 from 2024, demonstrating the continuous upward trend in economic well-being. This economic evolution facilitates a shift in consumer preferences, moving towards products that offer perceived higher quality and unique experiences, thereby expanding the market's value proposition.

Premiumization and craft beer drive market innovation and growth

The trend of premiumization and the increasing popularity of craft beer further drive market dynamics. Consumers, particularly younger demographics and urban populations, are seeking differentiated taste profiles and artisanal brewing methods, moving away from conventional lagers. This demand fosters innovation within the industry, encouraging both domestic and international brewers to expand their premium and craft portfolios. According to Heineken N.V.'s 2025 full-year results, published in February 2026, total premium volume across its global brands, including Vietnam, grew by 2.7%, reflecting this preference shift. This segment's growth offers significant opportunities for market players to capture value through product diversification and targeted marketing strategies. Overall, major players continue to show strong performance, with Saigon Beer-Alcohol-Beverage Corporation (SABECO) reporting net revenue of VNĐ6.457 trillion (approximately US$258 million) for Q1 2026, as noted by Longbridge in April 2026.

Download Free Sample Report

Key Market Challenges

Regulatory Pressure Dampens Growth and Shifts Beer Consumption

Increasing regulatory pressure significantly hampers the growth trajectory of the Vietnam Beer Market. Stringent excise taxes directly elevate product costs for consumers, reducing affordability and diminishing overall demand. This financial burden influences purchasing decisions, particularly for discretionary items like beer. Furthermore, the strict enforcement of drunk-driving laws, notably Decree 100, profoundly alters consumption patterns. These regulations discourage on-premise consumption at social gatherings and restaurants, impacting volume sales. According to WifiTalents, Decree 100 on drink-driving reduced beer consumption by an estimated 10 to 15 percent, reflecting a substantial shift in consumer behavior and market dynamics. This regulatory environment creates a challenging landscape for brewers, necessitating strategic adjustments to pricing and distribution in response to constrained market expansion.

Key Market Trends

Health and wellness trend driving demand for low- and non-alcoholic beer

Vietnamese consumers are increasingly prioritizing health and wellness, leading to a notable rise in demand for low and non-alcoholic beer options. This shift is influenced by a global move towards healthier lifestyles and heightened awareness of alcohol's impact on well-being. Brewers are adapting their portfolios to include alternatives with reduced calorie content and lower alcohol levels to cater to this evolving preference. The segment also benefits from regulatory changes, such as increased excise taxes on high-sugar beverages, which encourage a broader shift towards healthier drink choices. According to insider, in June 2026, Vietnam's non-alcoholic beverage sector is projected to maintain an annual growth rate of 7-9 percent between 2023 and 2028, reflecting this overarching consumer trend towards moderation and healthier consumption across the broader beverage market.

Digital commerce and DTC expansion reshaping the Vietnam beer market

The expansion of digital commerce and direct-to-consumer (DTC) channels represents another significant trend transforming the Vietnam Beer Market. The increasing penetration of smartphones and internet access has made e-commerce platforms crucial for beer distribution, offering consumers convenience, greater variety, and competitive pricing. This trend is particularly evident among younger, digitally-savvy demographics who favor online shopping for home consumption and social gatherings. While still in its nascent stages, the digital channel presents substantial growth potential for brewers to enhance market reach and consumer engagement. For example, a Cốc Cốc survey in 2025 indicated that online beer purchases represented approximately 5% of total sales, highlighting the early but promising adoption of digital sales channels.

Segmental Insights

Rapid Growth Fueled by Artisanal Beer Demand and Microbrewery Deregulation

The Craft Brewery segment is currently the fastest-growing within the Vietnam Beer Market. This rapid expansion is primarily fueled by a significant shift in consumer preferences towards unique, high-quality, and artisanal beer experiences, notably among the burgeoning urban middle class and younger demographics with increasing disposable incomes. Additionally, the segment's growth is supported by a conducive regulatory environment, including governmental deregulation of microbreweries and liberal licensing norms, which facilitates the establishment and operation of independent breweries. This allows for greater innovation in product offerings, often incorporating local ingredients, and contributes to the burgeoning craft beer culture across the country.

Regional Insights

Southern Vietnam's Market Leadership: Growth, Tourism, and Distribution Network

Southern Vietnam is a leading region within the Vietnam Beer Market, primarily driven by its robust economic landscape and significant urbanization, particularly centered around Ho Chi Minh City. This area benefits from higher per capita incomes and a dense concentration of hospitality infrastructure, including numerous restaurants and entertainment venues that stimulate consistent demand for both mainstream and premium beer. Furthermore, the region's strong appeal to international tourists considerably boosts consumption. The presence of major domestic brewers like Saigon Beer Alcohol Beverage Corporation (SABECO), deeply rooted in the South, further solidifies its market leadership through extensive distribution and cultural resonance.

Recent Developments

-

In March 2025, SABECO announced the relaunch of Bia Lạc Việt, featuring updated packaging and a new visual identity. This strategic move followed the brand's recognition as "World's Best Lager Light" at the World Beer Awards in 2024. The relaunch formed part of SABECO's broader 2025 growth strategy, which prioritizes innovation and enhancing its product portfolio. This initiative in the Vietnam Beer Market demonstrated the company’s ongoing efforts to refresh its offerings and respond to market dynamics while upholding brand quality.

-

In November 2024, SABECO officially inaugurated its Beer Research and Development Center (SRC) in Ho Chi Minh City. This state-of-the-art facility signifies SABECO's strategic investment in advancing product innovation and technological expertise within Vietnam's beer industry. The center focuses on pioneering new materials, processes, and beer formulations that resonate with Vietnamese culinary traditions and consumer preferences. By enhancing brewing science and technology, the SRC aims to elevate the quality and reputation of Vietnamese beverages on both domestic and international stages.

-

In August 2024, Saigon Beer-Alcohol-Beverage Corporation (SABECO) introduced 333 Pilsner, a new offering in the Vietnamese beer market. This product represented a lighter, smoother iteration of its established 333 brand, developed by Vietnamese brew masters utilizing European technology and premium imported ingredients. The launch aimed to cater to evolving consumer preferences for an extra-smooth drinking experience, marking an expansion of the Bia 333 portfolio. This initiative showcased SABECO's commitment to innovation and delivering high-quality products tailored for local tastes.

-

In June 2024, SABECO renewed its strategic partnership with the Ho Chi Minh Communist Youth Union (HCYU) for a three-year period. This collaboration focuses on joint initiatives across climate action, community empowerment, and public health, including promoting responsible drinking behaviors. The agreement outlined plans to install solar-powered streetlights in border regions, plant trees in twenty provinces, and support local One Commune One Product (OCOP) enterprises. This partnership underscores SABECO's commitment to sustainable development and generating positive socio-economic benefits for communities across Vietnam.

Key Market Players

- Heineken

- SABECO

- Carlsberg

- Bia Saigon

- Budweiser

- AB InBev

- Local Breweries

- Al Futtaim Beverages

- HyperPanda

- Amazon Vietnam

|

By Type

|

By Production

|

By Packaging

|

By Category

|

By End User

|

By Region

|

|

|

- Macro Brewery

- Micro Brewery

- Craft Brewery

|

|

|

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam Beer Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam Beer Market, By Type:

-

Vietnam Beer Market, By Production:

-

Macro Brewery

-

Micro Brewery

-

Craft Brewery

-

Vietnam Beer Market, By Packaging:

-

Vietnam Beer Market, By Category:

-

Vietnam Beer Market, By End User:

-

Vietnam Beer Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam Beer Market.

Available Customizations:

Vietnam Beer Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam Beer Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com