|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

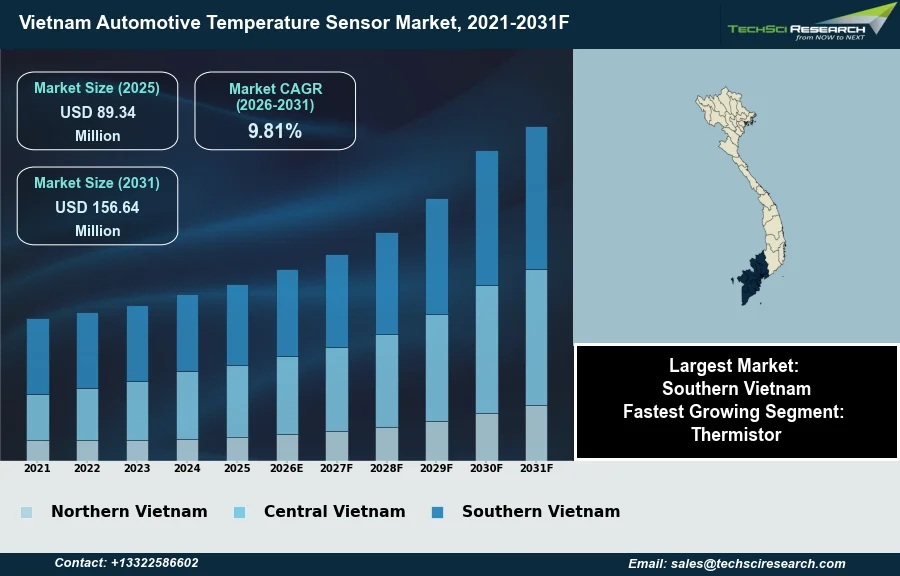

Market Size (2025)

|

USD 89.34 Million

|

|

CAGR (2026-2031)

|

9.81%

|

|

Fastest Growing Segment

|

Thermistor

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 156.64 Million

|

Market Overview

The Vietnam Automotive Temperature Sensor Market will grow from USD 89.34 Million in 2025 to USD 156.64 Million by 2031 at a 9.81% CAGR. Automotive temperature sensors are devices used to measure thermal conditions across various vehicle systems, typically employing thermistors, thermocouples, or resistance temperature detectors to transmit data for optimizing performance, efficiency, and safety. The Vietnam Automotive Temperature Sensor Market's expansion is driven by increasing demand for personal vehicles, spurred by rising disposable incomes and urbanization. Additionally, government policies and incentives attract foreign investment into domestic automotive manufacturing.

According to the Vietnam Automobile Manufacturers' Association (VAMA) and other local associations, Vietnam's total automobile sales reached approximately 604,000 units in 2025, reflecting a 22.2% year-on-year increase. This robust growth indicates a rising vehicle parc, consequently elevating demand for associated sensor technologies. However, a significant challenge impeding market expansion is the automotive component manufacturing's low localization rate, which, excluding VinFast, remains at 10-20% for passenger cars, necessitating reliance on imported parts and increasing production costs.

Key Market Drivers

Rapid expansion of Vietnam's auto market drives temperature sensor demand.

The rapid expansion of the Vietnamese automotive market is a primary catalyst for growth in the temperature sensor segment. As disposable incomes rise and urbanization continues, the demand for new vehicles increases, directly correlating with a higher volume of embedded temperature sensors across various vehicle systems. This market buoyancy is supported by a growing domestic manufacturing base. According to the National Statistics Office under the Ministry of Finance, published in June 2026, domestic manufacturers produced an estimated 232,100 vehicles in the first five months of 2026, marking a 26.7 percent year-on-year increase. This robust production growth, coupled with escalating vehicle parc, inherently drives the need for temperature sensors in engine control, exhaust gas monitoring, and cabin climate management systems to ensure optimal performance and compliance with emission standards.

Electrification boosts demand for automotive temperature sensors.

Simultaneously, the accelerated adoption of electric and hybrid vehicles significantly influences the demand for automotive temperature sensors. These advanced powertrains necessitate a greater number and variety of sensors for critical thermal management functions, particularly within battery packs, electric motors, and power electronics, to prevent overheating and ensure efficient operation. For instance, according to news published by Automechanika Ho Chi Minh City in June 2026, in the first quarter of 2026, Vietnam's electric and hybrid vehicle sales reached 162,039 units, increasing over 36 percent year-on-year. This substantial rise in new energy vehicle sales directly translates into a heightened requirement for specialized temperature sensing solutions. Overall, this market shift is reshaping the demand landscape for high-precision thermal monitoring components. Furthermore, reflecting the broader market dynamism, according to the Traffic Police Department, in 2025, over 624,000 new cars were registered, a 27 percent increase.

Download Free Sample Report

Key Market Challenges

Low Localization Rates Increase Costs and Impede Market Growth

The automotive component manufacturing's low localization rate presents a significant impediment to the growth of the Vietnam Automotive Temperature Sensor Market. With the localization rate for passenger car components, excluding VinFast, remaining at a low 10-20%, domestic vehicle production heavily relies on imported parts. This dependency directly increases production costs for local automotive assemblers, as they incur expenses related to international procurement, logistics, and tariffs, rather than benefiting from more cost-effective local supply chains.

Surging Auto Part Imports Elevate Costs and Limit Domestic Sensor Development

The substantial reliance on external suppliers for automotive components, including temperature sensors, stifles the development of a robust domestic manufacturing ecosystem for these critical parts. According to Vietnam Customs, in the January-April period of 2026, the import value of auto parts and components reached approximately US$2.47 billion, marking a nearly 45% year-on-year increase. This surge in import expenditures highlights the elevated cost structure for vehicle production in Vietnam, consequently impacting the final pricing of vehicles and potentially limiting the integration of advanced sensor technologies due to cost sensitivities. This situation ultimately constrains the expansion opportunities for local temperature sensor manufacturers and the broader automotive component market.

Key Market Trends

ADAs integration drives demand for precise temperature sensing in autonomous systems.

Advanced Driver-Assistance Systems (ADAS) integration represents a significant trend influencing the Vietnam Automotive Temperature Sensor Market. These systems, designed to enhance vehicle safety and driver comfort, rely on a sophisticated network of sensors, including those that monitor temperature. Temperature sensors are critical for ensuring the optimal operational performance and longevity of sensitive ADAS components such as cameras, radar modules, and LiDAR systems, as their accuracy can be compromised by thermal variations. Monitoring their internal temperatures helps maintain system reliability and safety under diverse driving conditions. According to industry news published in September 2025, Vietnam's VinFast partnered with Silicon Valley's Tensor to develop a fully autonomous EV set for a 2026 launch, equipped with advanced ADAS technologies utilizing over 100 sensors.

Predictive maintenance adoption expands temperature sensor demand across OEM and aftermarket.

The burgeoning adoption of predictive maintenance strategies within the Vietnamese automotive sector is another pivotal trend for the temperature sensor market. This approach moves beyond reactive repairs by continuously monitoring the condition of vehicle components, enabling the anticipation of potential failures before they occur. Temperature sensors are instrumental in this process, continuously assessing the thermal profiles of critical parts such as engine components, brakes, and transmission systems. Anomalous readings can serve as early indicators of wear, overheating, or other mechanical degradation, facilitating proactive servicing and preventing costly breakdowns. This shift towards proactive vehicle health management enhances operational efficiency and safety, thereby driving heightened demand for robust and accurate temperature sensing solutions for both original equipment and aftermarket applications. According to the Vietnam Manufacturing Tracker, published in June 2026, Vietnam's Industrial Production Index (IIP) rose 9.1 percent year-on-year in the first five months of 2026, reflecting the country's broader manufacturing expansion that increasingly integrates advanced operational technologies for efficiency and predictive capabilities.

Segmental Insights

Thermistors: Fastest-growing segment driven by EV adoption and thermal-management needs

The thermistor segment is emerging as the fastest-growing component within the Vietnam Automotive Temperature Sensor Market. This rapid expansion is primarily driven by the nation's accelerating transition towards electric vehicles and the increasing integration of advanced driver-assistance systems in modern automobiles. Thermistors are crucial for precise temperature monitoring in electric vehicle battery management systems and power electronics, essential for optimizing performance and extending battery life. Furthermore, escalating demand for improved fuel efficiency and adherence to evolving national environmental regulations, such as those promoting green transportation, necessitate the high accuracy and responsive thermal sensing capabilities that thermistors offer across various vehicle systems.

Regional Insights

Southern Vietnam: Leading Hub for Automotive Temperature Sensors

Southern Vietnam emerges as the dominant region within the Vietnam Automotive Temperature Sensor Market due to its robust economic activity and well-established automotive industry infrastructure. The region, particularly around Ho Chi Minh City, boasts significant automotive manufacturing clusters, attracting major automobile manufacturers to establish production and sales operations. This concentration benefits from developed transportation networks, higher population density, and increased disposable incomes, which collectively drive substantial demand for vehicles and, consequently, their integrated temperature sensors. Furthermore, the presence of a diverse industrial base and proactive government policies from bodies like the Ministry of Industry and Trade, which foster automotive manufacturing and component production, solidifies Southern Vietnam's leadership in this specialized market segment.

Recent Developments

-

In September 2025, Bosch Vietnam, a subsidiary of the Robert Bosch Group, enhanced its strategic commitment to Vietnam's burgeoning semiconductor industry by expanding its focus to include semiconductor chip design in Hanoi. Since 2024, the company has actively cultivated a dedicated team for global projects, concentrating on automotive microchips and advanced MEMS sensors. This initiative supports the development of sophisticated automotive components, which are integral to modern vehicle systems requiring precise environmental monitoring, including temperature regulation within the Vietnamese automotive market. This expansion in design capabilities represents breakthrough research and development within the local industry.

-

In May 2024, Amphenol RF Vietnam established a new manufacturing facility in Tay Ninh Province, a strategic move by its U.S.-based parent company to relocate production to Vietnam. This new factory specializes in the assembly of radio frequency (RF) connectors and RF cables specifically designed for automotive applications. The establishment of this facility by a key automotive component supplier signifies a new product manufacturing launch in Vietnam and contributes to the country's expanding ecosystem of advanced electronic components. These components are foundational for the complex electronic systems in modern vehicles that integrate various sensors, including those for temperature management.

-

In January 2024, Vietnamese electric vehicle manufacturer VinFast launched its innovative MirrorSense technology, slated for integration into its new electric vehicles. Developed by VinAI, a related technology company, this AI-powered system utilizes advanced optical sensors to accurately detect a driver's head and eye movements. This functionality allows for the automatic adjustment of all vehicle mirrors, significantly enhancing driver convenience and safety. The introduction of MirrorSense at CES 2024 highlights VinFast’s commitment to new product launches featuring sophisticated sensor technology, contributing to the advanced sensor ecosystem in the Vietnamese automotive sector.

-

In 2025, Bosch reported securing orders valued at approximately €10 billion for intelligent driver assistance systems, reflecting significant progress in automotive technology development. The company is actively advancing automotive software and artificial intelligence solutions, including a new AI platform designed to personalize the driving experience. This platform optimizes safety systems and adjusts various vehicle settings, such as mirrors and driving modes. This breakthrough research and development in AI-driven automotive solutions, implemented by a company with a strong presence in Vietnam, relies heavily on integrated sensor arrays, thereby impacting the broader automotive sensor market.

Key Market Players

- Bosch

- Continental

- Denso

- Honeywell

- Infineon

- NXP Semiconductors

- Sensata Technologies

- TE Connectivity

- Valeo

- Delphi Technologies

|

By Vehicle Type

|

By Product

|

By Usage

|

By Application

|

By Technology

|

By Region

|

- Passenger Cars

- Commercial Vehicles

|

- Resistance Temperature Detectors (RTD)

- Thermistor

- MEMS

- IC Temperature Sensor

- Thermocouple

- Infrared Temperature Sensor

|

|

- Engine

- Exhaust

- HVAC

- Transmission

- Thermal Seats

- EV Battery

- EV Motor

|

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam Automotive Temperature Sensor Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam Automotive Temperature Sensor Market, By Vehicle Type:

-

Passenger Cars

-

Commercial Vehicles

-

Vietnam Automotive Temperature Sensor Market, By Product:

-

Resistance Temperature Detectors (RTD)

-

Thermistor

-

MEMS

-

IC Temperature Sensor

-

Thermocouple

-

Infrared Temperature Sensor

-

Vietnam Automotive Temperature Sensor Market, By Usage:

-

Vietnam Automotive Temperature Sensor Market, By Application:

-

Engine

-

Exhaust

-

HVAC

-

Transmission

-

Thermal Seats

-

EV Battery

-

EV Motor

-

Vietnam Automotive Temperature Sensor Market, By Technology:

-

Vietnam Automotive Temperature Sensor Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam Automotive Temperature Sensor Market.

Available Customizations:

Vietnam Automotive Temperature Sensor Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam Automotive Temperature Sensor Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com