|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

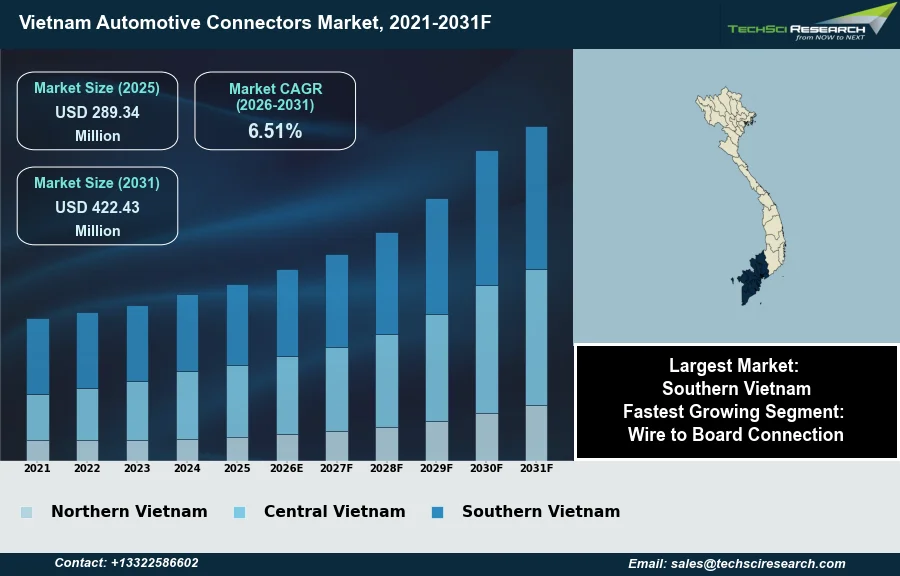

Market Size (2025)

|

USD 289.34 Million

|

|

CAGR (2026-2031)

|

6.51%

|

|

Fastest Growing Segment

|

Wire to Board Connection

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 422.43 Million

|

Market Overview

The Vietnam Automotive Connectors Market will grow from USD 289.34 Million in 2025 to USD 422.43 Million by 2031 at a 6.51% CAGR. Automotive connectors are essential components facilitating the connection of electrical circuits within vehicles, ensuring the seamless transfer of power and signals to various electrical systems for safe and efficient operation. The Vietnam Automotive Connectors Market is primarily driven by the escalating growth in domestic automotive manufacturing and increasing consumer demand for both passenger and commercial vehicles, supported by rising disposable incomes. Further impetus comes from governmental policies promoting local production and the expanding penetration of electric vehicles. According to the Vietnam Automobile Manufacturers' Association (VAMA) and other local associations, Vietnam's automobile sales reached a record high of 604,000 units in 2025, representing a 22.2% increase year-on-year.

This market expansion is also supported by increasing investments in infrastructure. However, a significant challenge impeding market growth is the limited localization rate within the automotive component supply chain, leading to a substantial reliance on imported raw materials and components. This dependence can result in supply chain disruptions and increased operational costs for manufacturers. For instance, the General Statistics Office reported that approximately 484,500 automobiles were assembled in Vietnam in 2025, but the industry continues to face challenges in establishing a comprehensive local supply ecosystem.

Key Market Drivers

Rising EV Adoption Drives Demand for High-Voltage and Data Connectors

Accelerated Electric Vehicle (EV) adoption significantly influences the Vietnam Automotive Connectors Market by increasing the demand for specialized high-voltage and data transfer connectors. EVs necessitate robust, high-power connectors to manage battery charging and power distribution, along with intricate connectors for battery management systems and advanced thermal management. These requirements differ substantially from traditional internal combustion engine vehicles, driving innovation and demand for new connector types. The rapid shift towards electrification is evident; according to Vietnam Investment Review and VNA, in the first quarter of 2026, Vietnam's electric and hybrid vehicle sales reached 162,039 units, an increase of over 36 per cent year-on-year. This surge directly translates to a heightened need for a wider range of automotive connectors, particularly those designed for higher voltages and enhanced durability, contributing to market expansion.

ADAS Expansion Fueled by High-Speed Data Needs and Government Investment

The increasing integration of Advanced Driver-Assistance Systems (ADAS) is another pivotal driver, fostering demand for high-speed data and miniature connectors. ADAS features like adaptive cruise control and automatic emergency braking rely on complex networks of sensors, cameras, radar, and electronic control units, all requiring secure electrical connections. These systems demand connectors capable of handling high data transfer rates with minimal latency for real-time performance. Supporting this, Vietnam's Ministry of Transport dedicated a $50 million fund by 2025 to promote smart vehicle technologies, including ADAS systems, demonstrating governmental commitment to advanced automotive safety. This emphasis on sophisticated in-vehicle electronics, coupled with growing domestic production, stimulates the market. In the first five months of 2026, domestic manufacturers produced an estimated 232,100 vehicles, reflecting a 26.7% year-on-year increase, according to the National Statistics Office under the Ministry of Finance.

Download Free Sample Report

Key Market Challenges

Limited localization and exposure to global supply-chain risks

The limited localization rate within the automotive component supply chain presents a significant impediment to the growth of the Vietnam Automotive Connectors Market. This challenge forces manufacturers to maintain a substantial reliance on imported raw materials and finished components, including complex automotive connectors. Such dependence directly exposes the market to international supply chain vulnerabilities, including geopolitical events, shipping disruptions, and currency fluctuations, which can lead to unpredictable lead times and increased procurement costs for critical parts. This situation complicates long-term production planning and can hinder the competitiveness of locally assembled vehicles.

Rising import dependence elevates costs and hampers local ecosystem development

The need to import a high proportion of components increases the overall cost structure for automotive manufacturers in Vietnam. This elevated cost base subsequently impacts the pricing of domestically produced vehicles, potentially reducing their appeal to consumers and slowing the expansion of local automotive production. According to the Vietnam Automobile Manufacturers' Association (VAMA), in May 2026, sales of completely built-up imported vehicles reached 16,855 units, surpassing the 13,080 units of locally assembled vehicles. This sustained import dependency restricts the development of a robust local ecosystem for automotive connector manufacturing, thereby directly hampering market expansion and reducing opportunities for domestic enterprises to innovate and grow within the sector.

Key Market Trends

Rising Electronic Integration Drives Demand for Miniaturized, High-Density Connectors

The increasing integration of electronic systems across all vehicle platforms is driving a significant demand for miniaturized and high-density connectors in the Vietnam Automotive Connectors Market. As vehicles incorporate more functionalities, the available space for components diminishes, necessitating connectors that carry more signals or power within a smaller footprint. This trend requires suppliers to innovate in compact designs and advanced materials. For instance, according to VietNamNet, in the first four months of 2026, electronics and computer component imports alone surged by 52.3 percent year-on-year, reaching $65.3 billion. This continuous rise in electronic content per vehicle mandates connector solutions prioritizing space-saving and robust performance, directly influencing manufacturing processes and design requirements for automotive connectors in the region.

Infotainment and Connectivity Drive Demand for High-Bandwidth Connectors

Another pivotal trend shaping the Vietnam Automotive Connectors Market is the profound impact of vehicle connectivity and in-vehicle infotainment systems, driven by evolving consumer expectations for a seamless digital experience. Modern consumers seek sophisticated infotainment features, including high-definition displays, advanced navigation, and integrated communication, requiring high-bandwidth and reliable connectors for data transmission. The escalating demand for internet connectivity and smart features necessitates advanced connector designs capable of handling increasing data loads. Supporting this, LG Electronics affirmed its commitment to expanding its Vietnam research and development subsidiary, which now operates with over 1,250 software engineers developing core vehicle software, including infotainment and telematics, as reported by Vietnam Investment Review on June 19, 2026. This focus on local software development for advanced in-vehicle systems underscores the growing need for specialized connectors to support these complex digital ecosystems.

Segmental Insights

Wire-to-Board Connectors: Fastest-Growing Segment Fueled by EV Adoption and ADAS

The key segmental insight for Vietnam's Automotive Connectors Market highlights Wire to Board Connection as the fastest-growing segment, largely propelled by the nation's rapid advancements in vehicle electrification and the increasing integration of advanced driver-assistance systems (ADAS). The significant rise in electric vehicle (EV) adoption, championed by local manufacturers like VinFast and supported by Vietnamese government policies promoting sustainable transportation, necessitates robust wire to board connectors for intricate electrical subsystems and high-voltage applications. Furthermore, escalating consumer demand for sophisticated vehicle connectivity features and enhanced road safety, underscored by government initiatives to mandate basic ADAS features in new vehicles from 2025, drives the demand for these connectors to ensure reliable data and power transmission within increasingly complex electronic architectures.

Regional Insights

Southern Vietnam Emerges as the Automotive Connectors Hub

Southern Vietnam leads the Vietnam Automotive Connectors Market due to its significant concentration of automotive manufacturing operations and robust industrial infrastructure. The region, encompassing Ho Chi Minh City, Dong Nai, and Binh Duong provinces, serves as a primary hub for numerous automotive original equipment manufacturers and component suppliers. This concentration is fostered by the Vietnamese government's supportive policies, including investment incentives and preferential tax structures designed to attract foreign direct investment and bolster domestic production within the automotive sector. Such a business-friendly environment, coupled with strategic logistical advantages, cultivates a strong ecosystem for the automotive components industry, driving the demand and supply for automotive connectors.

Recent Developments

-

In November 2025, Micro Commercial Components (MCC) announced that its Vietnam backend facility was fully operational, supporting the future launch of its automotive-grade SMx Series in 2026. This strategic move aims to strengthen global supply chains by accelerating MCC's commitment to electrification and miniaturization within the automotive sector. The facility’s operational status in 2025 underscores a significant expansion of manufacturing capabilities in Vietnam, directly enabling the production of electronic components and their associated interconnects for electric vehicles. This development positively impacts the Vietnam Automotive Connectors Market by fostering a robust local ecosystem for advanced automotive electronics.

-

In December 2024, Molex, a global leader in electronics and connectivity innovation, shared its projections for 2025, anticipating a steady rise in high-speed connectivity solutions that will drive advancements in various sectors, including the automotive industry. The company highlighted that compact and durable connectors, with a pitch of 2.54mm or less, are expected to become prevalent in electric vehicles and zonal architectures. This strategic focus by Molex on miniaturized and high-performance connectors directly reflects ongoing breakthrough research and product development trends that will influence the Vietnam Automotive Connectors Market as vehicle electrification and advanced driver-assistance systems become more widespread.

-

In November 2024, Greenconn, a prominent manufacturer of connector solutions, announced the completion of its new production facility in Hai Duong, Vietnam, with mass production scheduled to commence in the same month. This strategic expansion marks Greenconn’s fourth factory globally, significantly bolstering its manufacturing capacity for various connector products, including automotive electrical connectors. The facility is equipped with advanced production and testing machinery, aiming to enhance product quality and efficiency while offering more cost-effective interconnect solutions to its global clientele. This development directly contributes to the growth and localization of the automotive connectors market in Vietnam by increasing local production capabilities.

-

In April 2024, Sumitomo Electric Industries Ltd. received approval for a significant investment to establish Sumiden Vietnam Automotive Wire in Hai Duong Province. This initiative involves a capital injection of USD 100 million and is projected to create 8,000 employment opportunities. The new facility is set to become Southeast Asia's largest producer of automotive wire, which is a crucial upstream component for the assembly of automotive connectors. This investment represents a substantial development for the automotive supply chain in Vietnam, enhancing local content production and supporting the increasing demand for connector-related components in the burgeoning automotive sector.

Key Market Players

- TE Connectivity

- Yazaki Corporation

- Sumitomo Electric Industries

- Aptiv PLC

- Amphenol Corporation

- Molex

- JAE Electronics

- Hirose Electric

- Korea Electric Terminal

- Foxconn Interconnect Technology

|

By Vehicle Type

|

By Connection Type

|

By Application

|

By Region

|

- Passenger Car

- Commercial Vehicles

|

- Wire to Wire Connection

- Board to Board Connection

- Wire to Board Connection

|

- Body Control & Interiors

- Fuel & Emission Control

- Safety & Security System

- Engine Control & Cooling System

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam Automotive Connectors Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam Automotive Connectors Market, By Vehicle Type:

-

Passenger Car

-

Commercial Vehicles

-

Vietnam Automotive Connectors Market, By Connection Type:

-

Wire to Wire Connection

-

Board to Board Connection

-

Wire to Board Connection

-

Vietnam Automotive Connectors Market, By Application:

-

Body Control & Interiors

-

Fuel & Emission Control

-

Safety & Security System

-

Engine Control & Cooling System

-

Vietnam Automotive Connectors Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam Automotive Connectors Market.

Available Customizations:

Vietnam Automotive Connectors Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam Automotive Connectors Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com