|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

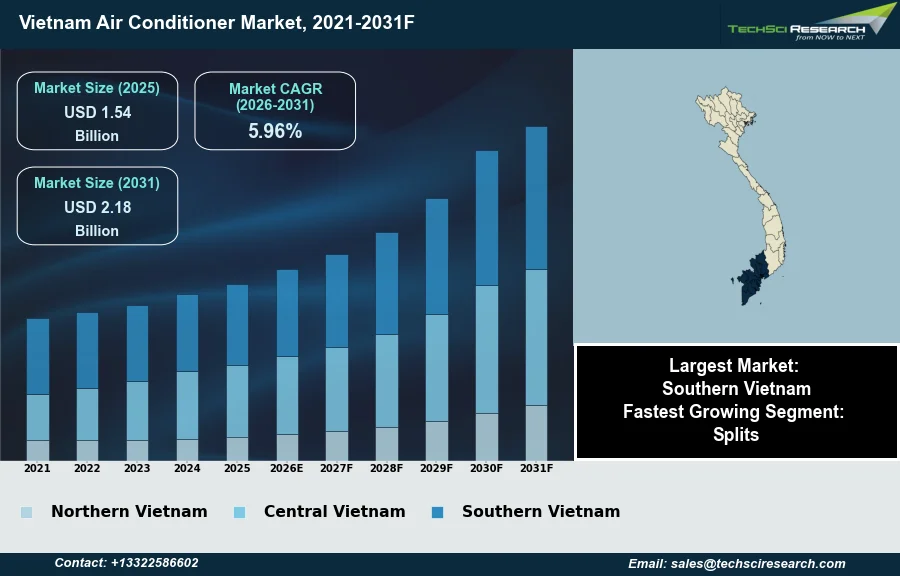

Market Size (2025)

|

USD 1.54 Billion

|

|

CAGR (2026-2031)

|

5.96%

|

|

Fastest Growing Segment

|

Splits

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 2.18 Billion

|

Market Overview

The Air Conditioner Market in Vietnam will grow from USD 1.54 Billion in 2025 to USD 2.18 Billion by 2031 at a 5.96% CAGR. An air conditioner is an electromechanical system designed to regulate indoor air temperature and humidity, primarily for cooling and maintaining thermal comfort within enclosed spaces. The Vietnam Air Conditioner Market's expansion is fundamentally driven by sustained growth in disposable incomes, accelerating urbanization leading to increased residential and commercial construction, and persistently high ambient temperatures exacerbated by climate change. These factors collectively establish a robust demand base.

According to the Vietnam Association of Refrigeration and Air Conditioning Science and Technology, the market size is projected to reach approximately 2.9 billion USD in 2025. A notable challenge impeding market expansion is the implementation of a new special consumption tax on air conditioners with capacities between 24,000 and 90,000 BTU, effective January 1, 2026, which could impact pricing and consumer demand in specific segments.

Key Market Drivers

Climate-Driven Demand for Air Conditioners

Rising temperatures and humidity levels represent a primary catalyst for the Vietnam Air Conditioner Market. The nation's tropical climate consistently presents prolonged periods of heat, intensifying the demand for cooling solutions in both residential and commercial sectors. This escalating heat directly translates to increased usage of air conditioning systems. According to Vietnam Electricity (EVN), in the first five months of 2024, residential electricity consumption in the country increased by 18.08% compared to the same period in 2023, largely driven by the need for cooling during intense heatwaves. Such environmental conditions necessitate air conditioners for maintaining thermal comfort, thereby making them increasingly essential rather than discretionary purchases.

Rising Incomes and Middle-Class Expansion Drive Demand

Concurrently, increasing disposable incomes and an expanding middle class significantly bolster the market's growth. As economic prosperity rises, more Vietnamese households gain the financial capacity to invest in appliances that enhance living standards. This demographic shift leads to a surge in demand for air conditioning units. According to the General Statistics Office, reported by VietNamNet in January 2025, the average monthly income of Vietnamese workers surged by 8.6% annually to 7.7 million VND in 2024. This augmented purchasing power enables consumers to acquire both initial installations and upgrade to more advanced, energy-efficient models. Overall, reflecting this broader economic vitality, Vietnam's total retail sales of goods and services increased by 11.8% year-on-year in May 2024, according to Trading Economics. These factors collectively underscore a robust and evolving consumer base, capable of driving sustained market expansion.

Download Free Sample Report

Key Market Challenges

Impact of the new tax on high-capacity air conditioners

The implementation of a new special consumption tax on air conditioners with capacities between 24,000 and 90,000 BTU, effective January 1, 2026, presents a significant challenge to the growth trajectory of the Vietnam Air Conditioner Market. This special consumption tax is an indirect levy incorporated into the final selling price of affected products, thereby directly increasing their retail cost to consumers. This upward price adjustment is expected to particularly impact commercial applications and larger residential installations where these higher-capacity units are frequently utilized.

Demand reduction and implications for market competitiveness

The increased pricing from this tax may lead to a measurable reduction in consumer purchasing decisions for these specific air conditioner segments. Businesses and individuals might delay planned acquisitions or consider lower-capacity models not subject to the new levy, potentially affecting sales volumes for a substantial portion of the market. This policy, while aiming to reduce electricity consumption and emissions by discouraging high-capacity units, places an additional financial burden on manufacturers and could hinder market competitiveness.

Key Market Trends

Shift Toward Smart, Connected Air Conditioners

The Vietnam Air Conditioner Market is undergoing a notable transformation driven by the rising demand for smart and connected air conditioners. Consumers increasingly prioritize convenience, remote control capabilities, and integration with broader smart home ecosystems, moving beyond basic cooling functionality. These advanced units allow users to manage settings via mobile applications, optimize energy usage, and even integrate with voice assistants, enhancing overall home automation and user experience. This shift reflects a growing technological sophistication among Vietnamese consumers. According to note.com, September 15, 2025, in 'Vietnam's Household Appliance Market Surges at 7.8% CAGR as Smart Homes and E-Commerce Reshape Demand', 35% of all appliances are now classified as smart or connected devices, highlighting a significant market inclination towards intelligent solutions.

Expansion of Online Sales Channels for Air Conditioners

Concurrently, the market is experiencing a substantial expansion of online sales channels for air conditioners. The increasing digital literacy and widespread internet penetration in Vietnam are enabling consumers to research, compare, and purchase appliances through e-commerce platforms. This channel offers benefits such as wider product selections, competitive pricing, and convenient home delivery and installation services, which appeal to modern buyers. The growth of online retail facilitates greater accessibility to a diverse range of air conditioning units from various brands. According to note.com, September 15, 2025, in the same article, Vietnam's e-commerce market experienced remarkable growth in 2025, expanding by 40% and reaching a transaction value of USD 13.82 billion, underscoring the increasing consumer reliance on digital platforms for purchasing decisions.

Segmental Insights

Split AC Segment as a Growth Driver in the Vietnam Air Conditioner Market

The Splits segment is a key driver of growth in the Vietnam Air Conditioner Market, experiencing rapid expansion due to several interconnected factors. Increasing urbanization and a burgeoning middle class, particularly in major cities, are fueling demand for cooling solutions in modern residential and commercial developments. Concurrently, Vietnam's tropical climate, characterized by rising temperatures and intense heatwaves, makes reliable air conditioning a necessity rather than a luxury. Consumers increasingly prefer split units for their energy efficiency, aesthetic appeal, and suitability for individual room cooling in diverse housing structures. Furthermore, regulatory advancements, such as the TCVN 7830:2021 minimum performance thresholds introduced by relevant Vietnamese authorities, are promoting advanced variable-speed technologies often found in modern split systems, reinforcing market demand.

Regional Insights

Climate-driven demand and urban growth propel Southern Vietnam's air conditioner market, supported by rising incomes and efficiency standards.

Southern Vietnam dominates the Vietnam Air Conditioner Market primarily due to its consistently hot and humid tropical climate, which generates year-round demand for cooling solutions, particularly in Ho Chi Minh City. As the country's largest economic hub, the region experiences significant urbanization, marked by extensive residential and commercial construction, including high-rise buildings and shopping centers. This rapid development, coupled with a dense population and rising disposable incomes among a growing middle class, drives substantial adoption of air conditioning systems in both homes and businesses. The Ministry of Industry and Trade, alongside the Ministry of Science and Technology, establishes energy efficiency standards that air conditioners must meet for market circulation.

Recent Developments

-

In June 2025, Samsung Electronics launched a new range of smart system air conditioners across Southeast Asia, including Vietnam. These new models featured built-in Wi-Fi, enabling seamless control through the SmartThings app and support for AI voice assistants. The lineup included advanced functions like AI Energy Mode for optimized power consumption and WindFree operation for comfortable, indirect cooling. This strategic product introduction underscored Samsung's focus on expanding its presence in Vietnam's growing market for intelligent and energy-efficient climate control solutions for both residential and commercial sectors.

-

In June 2025, LG Electronics convened its annual HVAC Leaders' Summit, followed by InnoFest AIR 2025 APAC, which brought together dealers and contractors from various Asian countries, including Vietnam. Participants were introduced to LG's latest residential and commercial air conditioner product lines and gained insights into the company’s manufacturing capabilities. These events served as crucial platforms for fostering collaborations and facilitating technical knowledge exchange, reinforcing LG's strategy to strengthen its business and expand its innovative heating, ventilation, and air conditioning solutions in key markets like Vietnam.

-

In March 2025, Daikin Vietnam introduced its 2025 air conditioner series, notably featuring the innovative Humi Comfort technology. This breakthrough research-driven feature was specifically developed to provide optimal humidity control, creating an ideal indoor environment tailored to Vietnam's unique climate. The launch positioned Daikin's new products as advanced solutions offering more than just cooling, but comprehensive air quality and comfort management. This initiative reinforces Daikin's commitment to delivering localized technological advancements to its Vietnamese customer base.

-

In April 2024, Daikin Vietnam, in collaboration with Petroleum General Distribution Services Joint Stock Company (PSD), unveiled its latest wall-mounted air conditioner products specifically designed for the Vietnamese market. The "Barashi 2024" event served as the platform for this launch, where new product features and stringent quality standards were highlighted. This partnership aimed to leverage PSD's extensive distribution network across the country, enhancing Daikin's market penetration and sales performance, particularly in anticipation of the summer season in Vietnam.

Key Market Players

- Daikin

- Carrier

- LG

- Mitsubishi Electric

- Samsung

- SKM Air Conditioning

- Johnson Controls

- Trane

- Danfoss

- Gree

|

By Type

|

By End User

|

By Region

|

- Splits

- VRFs

- Chillers

- Windows

- Others

|

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam Air Conditioner Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam Air Conditioner Market, By Type:

-

Splits

-

VRFs

-

Chillers

-

Windows

-

Others

-

Vietnam Air Conditioner Market, By End User:

-

Vietnam Air Conditioner Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam Air Conditioner Market.

Available Customizations:

Vietnam Air Conditioner Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam Air Conditioner Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com