|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 378.59 Million

|

|

CAGR (2026-2031)

|

11.41%

|

|

Fastest Growing Segment

|

ADAS

|

|

Largest Market

|

Dubai

|

|

Market Size (2031)

|

USD 723.96 Million

|

Market Overview

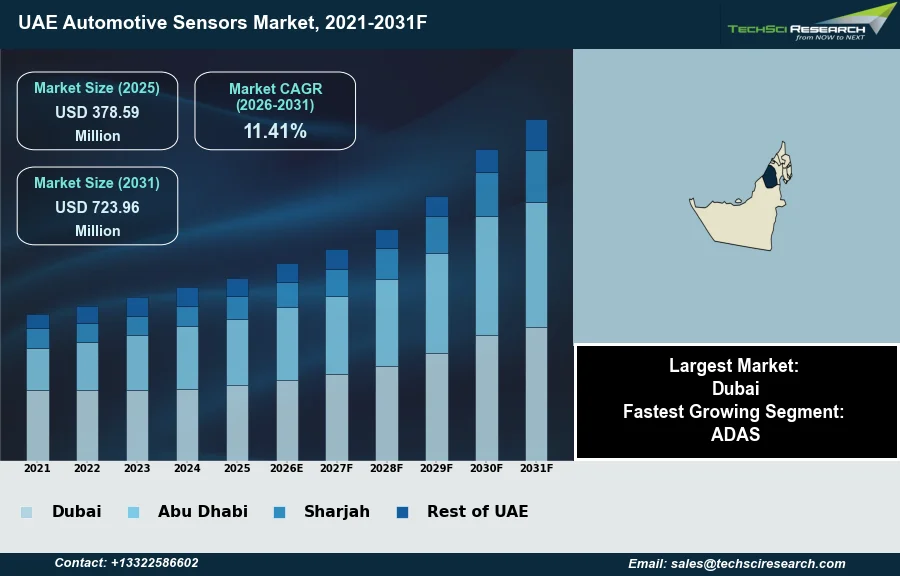

The UAE Automotive Sensors Market will grow from USD 378.59 Million in 2025 to USD 723.96 Million by 2031 at a 11.41% CAGR. Automotive sensors are electronic components integrated into vehicles to monitor various operational parameters, enabling precise system control, enhancing safety features, and supporting advanced driver-assistance functions. The UAE Automotive Sensors Market is primarily driven by robust government initiatives promoting smart city development and sustainable mobility solutions, coupled with increasing consumer demand for advanced driver-assistance systems (ADAS) and vehicle electrification. According to the International Organization of Motor Vehicle Manufacturers (OICA), commercial car sales in the United Arab Emirates reached 37,403 units in 2024, representing an increase from the prior year. This sustained growth in overall vehicle sales, alongside a rising vehicle per capita rate, directly stimulates demand for integrated sensor technologies.

A significant challenge impeding market expansion is the inherent complexity and cost associated with integrating increasingly diverse and intricate sensor systems into existing vehicle architectures and manufacturing processes. Ensuring interoperability across varied sensor types and vehicle platforms, alongside managing the financial implications of high-value component sourcing and specialized installation, presents a notable impediment to broader market penetration.

Key Market Drivers

ADAS Proliferation Drives UAE Automotive Sensor Demand

Advanced Driver-Assistance Systems (ADAS) proliferation significantly drives the UAE Automotive Sensors Market. These systems, encompassing functions from parking assistance to collision avoidance, rely heavily on sophisticated arrays of radar, lidar, camera, and ultrasonic sensors to monitor vehicle surroundings. The increasing integration of ADAS features into new vehicles is prompted by evolving safety regulations and growing consumer demand for enhanced security. For instance, the Dubai Roads and Transport Authority (RTA) is actively implementing advanced intelligent transport systems; according to Dubai Voice, in October 2025, the RTA announced that its Smart Vehicle Network, which integrates Cooperative Intelligent Transport Systems, has reduced traffic delays by 25%. This strategic focus on smarter urban mobility directly fuels the demand for high-performance automotive sensors.

EV/HEV Adoption Raises Automotive Sensor Requirements

The rising adoption of electric and hybrid vehicles constitutes another critical growth factor. Electric vehicles (EVs) and hybrid electric vehicles (HEVs) inherently require a greater number and variety of sensors than conventional vehicles, specifically for battery management, motor control, and regenerative braking. These sensors are vital for optimizing performance, extending range, and ensuring battery safety. This trend is clearly observed; according to electrive.com, in May 2025, Abu Dhabi registered over 15,000 EVs during the first quarter of 2025, marking a 60 percent increase from the prior year. Such strong growth in EV adoption directly translates into heightened demand for specialized automotive sensors. Additionally, reflecting overall market dynamics, according to DubiCars, in March 2026, demand for premium vehicles priced above AED 150,000 grew by 40% year-on-year in 2025, indicating a preference for higher-specification vehicles typically equipped with extensive sensor suites.

Download Free Sample Report

Key Market Challenges

Integration Complexity and Cost Challenges for UAE Automotive Sensors

The inherent complexity and cost associated with integrating increasingly diverse and intricate sensor systems into existing vehicle architectures and manufacturing processes presents a significant challenge for the UAE Automotive Sensors Market. This impediment stems from the need to ensure seamless interoperability across various sensor types and vehicle platforms, coupled with the substantial financial implications of sourcing high-value components and executing specialized installations. Such integration demands sophisticated electronic architectures and rigorous calibration processes, directly elevating overall vehicle production costs.

Costs and Capacity Constraints on UAE Sensor Adoption Amid Regional Growth

The elevated costs and technical difficulties hinder broader market penetration and the accelerated adoption of advanced sensor technologies, despite regional growth. For instance, according to the International Organization of Motor Vehicle Manufacturers (OICA), sales across Asia, Oceania, and the Middle East collectively increased by 7.1% in 2025, reaching 55.02 million units. While demonstrating robust regional demand, the complexity of integrating advanced sensor systems can constrain the UAE's local manufacturing capacity and deter manufacturers from introducing a wider range of sensor-rich vehicles at competitive price points, thereby potentially limiting the nation's full participation in this growth. This complexity particularly affects efforts to develop local automotive assembly capabilities, where, as per the Abu Dhabi Department of Economic Development (ADDED), only a limited number of automotive assembly lines operate with minimal integration into upstream component sourcing.

Key Market Trends

Predictive maintenance and fleet telematics driving UAE automotive sensor market

Growth in predictive maintenance and fleet telematics solutions represents a key trend driving the UAE automotive sensors market, as it moves beyond basic tracking to advanced operational intelligence. This approach utilizes sensor-generated data to monitor vehicle components, predict potential failures, and optimize maintenance schedules proactively. The shift enables fleet operators to enhance efficiency, reduce unexpected downtime, and significantly lower operational expenses, thereby stimulating demand for a diverse range of diagnostic and performance-monitoring sensors. For instance, according to ZAWYA, in June 2026, Dulsco Group equipped all 454 of its vehicles with telematics technology to monitor driving behaviors and provide real-time performance insights. This widespread adoption underscores the increasing reliance on integrated sensor systems for informed decision-making in fleet management.

V2X-enabled smart city infrastructure enabling sensors for autonomous driving

The expansion of smart city infrastructure, particularly supporting Vehicle-to-Everything (V2X) communication, is another critical trend influencing the UAE automotive sensors market. This trend involves the deployment of advanced sensor systems that facilitate instantaneous data exchange between vehicles, other vehicles, roadside infrastructure, and central traffic management systems. Such interconnectedness is essential for developing intelligent transportation networks, improving traffic flow, and bolstering road safety. This framework is fundamental for the broader implementation of autonomous driving technologies within urban environments. Highlighting this advancement, according to Dubai Transport Mega Projects Driving Property Investment Opportunities in 2026, in February 2026, Dubai initiated operations of 100 AI-powered driverless taxis from March 2026. These deployments require sophisticated sensor arrays for comprehensive environmental perception and robust V2X communication capabilities.

Segmental Insights

Drivers of UAE ADAS Growth: Regulations, Demand, and Smart Mobility

The Advanced Driver Assistance Systems (ADAS) segment is experiencing rapid growth within the UAE Automotive Sensors Market. This acceleration is primarily driven by the increasing emphasis on road safety, with the UAE government actively implementing regulations and initiatives that encourage automakers to integrate ADAS features such as lane departure warning and adaptive cruise control into new vehicles. Additionally, consumer demand for enhanced safety and advanced technological features in vehicles is significantly contributing to the segment's expansion. The nation's broader smart mobility vision, including smart city projects, further promotes the adoption of these sensor-intensive systems.

Regional Insights

Dubai's strategic leadership in the UAE automotive sensors market

Dubai commands the UAE Automotive Sensors Market, primarily driven by its position as the nation's commercial and technological center, which fosters a high concentration of luxury vehicles and advanced mobility projects demanding sophisticated sensor technologies. This leadership is significantly reinforced by Dubai's comprehensive smart city initiatives and the Roads and Transport Authority's (RTA) strategic commitment to intelligent transport systems, including its ambitious Autonomous Transportation Strategy. The strong consumer preference for smart, connected vehicles among Dubai residents, coupled with the city's advanced infrastructure and strategic role as a global trade hub for automotive components, collectively underpins its dominance in the automotive sensors sector.

Recent Developments

-

In November 2025, the Integrated Transport Centre (ITC) in Abu Dhabi announced the development of the Abu Dhabi Smart and Autonomous Mobility Systems Testing Centre. This collaborative effort, involving strategic partners Space42, Masdar City, and Emirates Driving Company, will establish the first facility of its kind in the Middle East and North Africa. The center will be equipped with advanced sensor networks and digital twin technologies, integrating real-time monitoring and data analysis. This initiative is pivotal for the UAE automotive sensors market as it provides a dedicated environment for testing, validating, and certifying autonomous vehicle sensor technologies.

-

In October 2025, a commercial fleet of self-driving electric trucks, developed by Evocargo, was deployed for RAK Ceramics in the Al Jazeera Al Hamra industrial zone in Ras Al Khaimah. This collaboration introduced unmanned N1 electric trucks, which are equipped with an AI-driven multi-sensor perception system. This system integrates data from LiDARs, sonars, and cameras, processed through an onboard computing unit to adapt to road and environmental conditions instantly. This deployment showcases a new product application for advanced automotive sensors in the UAE's logistics and industrial sectors.

-

In September 2025, Tensor debuted its fully autonomous Level 4 Robocar at the Dubai World Congress for Self-Driving Transport. This new product launch represents a breakthrough in personal autonomous vehicles within the UAE automotive market. The Robocar incorporates over 100 integrated sensors, featuring 37 cameras, 5 LiDAR units, and 11 radars, designed to ensure comprehensive environmental perception and safety. The introduction of such a sensor-rich vehicle highlights the rapid development and adoption of advanced sensor technologies crucial for autonomous driving capabilities in the region.

-

In 2024, Uber, in collaboration with WeRide, launched a robotaxi service in Abu Dhabi. This initiative marked a significant advancement in autonomous mobility within the UAE, directly impacting the automotive sensors market. The operation of robotaxis relies extensively on advanced sensor technologies, including LiDAR, radar, and cameras, to navigate safely and detect surroundings without human intervention. This collaboration demonstrates a practical application of complex sensor fusion systems for urban transportation, emphasizing the growing demand for sophisticated automotive sensor solutions in the region.

Key Market Players

- Bosch UAE

- Continental UAE

- Denso UAE

- Honeywell UAE

- Infineon Technologies UAE

- NXP Semiconductors UAE

- Sensata Technologies UAE

- TE Connectivity UAE

- Valeo UAE

- Delphi Technologies UAE

|

By Sensor Type

|

By Vehicle Type

|

By Application

|

By Region

|

- Temperature Sensor

- Pressure Sensor

- Oxygen Sensor

- Position Sensor

- Motion Sensor

- Torque Sensor

- Optical Sensor

- Others

|

- Passenger Car

- Commercial Vehicle

|

- ADAS

- Chassis

- Powertrain

- Others

|

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

|

Report Scope:

In this report, the UAE Automotive Sensors Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

UAE Automotive Sensors Market, By Sensor Type:

-

Temperature Sensor

-

Pressure Sensor

-

Oxygen Sensor

-

Position Sensor

-

Motion Sensor

-

Torque Sensor

-

Optical Sensor

-

Others

-

UAE Automotive Sensors Market, By Vehicle Type:

-

Passenger Car

-

Commercial Vehicle

-

UAE Automotive Sensors Market, By Application:

-

ADAS

-

Chassis

-

Powertrain

-

Others

-

UAE Automotive Sensors Market, By Region:

-

Dubai

-

Abu Dhabi

-

Sharjah

-

Rest of UAE

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the UAE Automotive Sensors Market.

Available Customizations:

UAE Automotive Sensors Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

UAE Automotive Sensors Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com