|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 10.89 Billion

|

|

CAGR (2026-2031)

|

4.61%

|

|

Fastest Growing Segment

|

Outsource Warehousing

|

|

Largest Market

|

Eastern

|

|

Market Size (2031)

|

USD 14.27 Billion

|

Market Overview

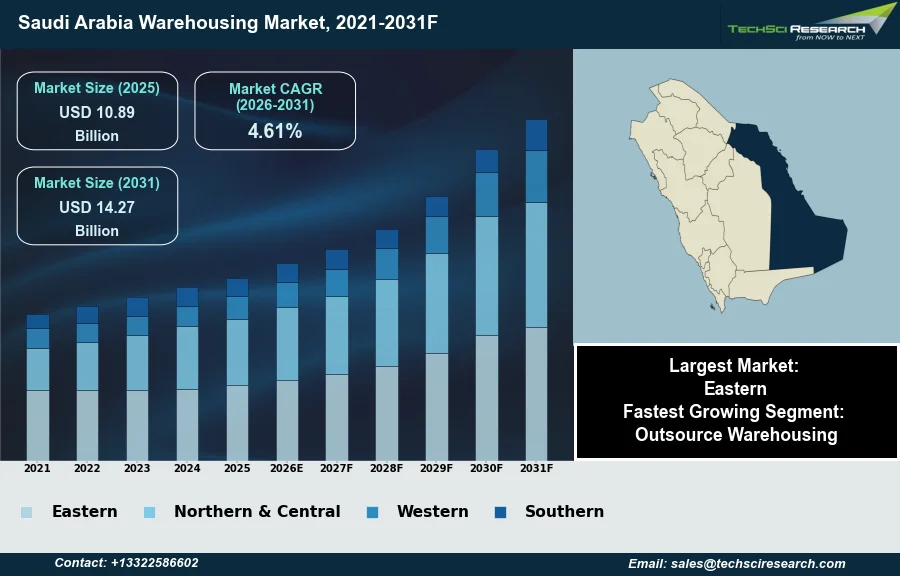

The Saudi Arabia Warehousing Market will grow from USD 10.89 Billion in 2025 to USD 14.27 Billion by 2031 at a 4.61% CAGR. Warehousing constitutes the systematic storage and management of physical goods and materials within specialized facilities, serving as an essential element of modern logistics and supply chain frameworks. The Saudi Arabia Warehousing Market is primarily propelled by the Kingdom's ambitious economic diversification agenda under Vision 2030, which channels substantial investments into developing a robust logistics infrastructure. Concurrently, the burgeoning e-commerce sector and shifts in consumer purchasing patterns are significantly escalating the need for efficient storage and distribution capabilities throughout the nation. The expansion of the domestic manufacturing base further contributes to the demand for enhanced warehousing solutions.

According to SAL Saudi Logistics Services Co., revenue from its Logistics division reached SAR 86 million in the fourth quarter of 2025, demonstrating a 16% year-on-year increase. Nevertheless, a notable impediment to continued market expansion is the scarcity of modern, high-specification Grade A warehousing facilities, which creates a persistent supply-demand imbalance, particularly for advanced and automated storage solutions across key logistical hubs.

Key Market Drivers

E-commerce Growth Drives Warehousing Demand

The expansion of the e-commerce sector and increasing digitalization represent a primary driver for the Saudi Arabia Warehousing Market. The shift in consumer behavior towards online shopping necessitates a sophisticated network of storage, fulfillment, and distribution centers across the Kingdom. This growing digital commerce significantly impacts the demand for warehousing space, particularly for facilities capable of handling a diverse range of products, rapid inventory turnover, and efficient last-mile delivery operations. According to the Saudi Central Bank, December 2025, in "Saudi e-commerce sales surge 68% to over SR30 billion in October 2025", e-commerce sales via Mada cards in Saudi Arabia exceeded SAR 30.7 billion in October 2025, demonstrating a 68% year-on-year increase. This substantial growth underscores the escalating need for modern warehousing solutions to support the burgeoning online retail environment.

Vision 2030 and National Logistics Strategy Stimulate Warehousing Development

Furthermore, the government's ambitious Vision 2030 and the National Logistics Strategy are instrumental in shaping the warehousing landscape through significant infrastructure investments. These initiatives aim to transform Saudi Arabia into a global logistics hub, fostering the development of advanced transport networks, special economic zones, and integrated logistics parks. Such strategic governmental impetus directly fuels demand for large-scale, technologically equipped warehousing facilities. For instance, according to the Saudi Ports Authority, January 2026, in "Saudi Ports Authority reports over 8 million TEUs handled in 2025", container throughput in its ports rose by 10.58% year-on-year in 2025, reaching over 8.3 million TEUs, indicating increased trade volumes requiring storage. Overall, this concerted effort contributes to the Kingdom's economic diversification, with Saudi Arabia's real GDP expanding by 4.5% in 2025, according to the General Authority for Statistics, February 2026.

Download Free Sample Report

Key Market Challenges

Scarcity of Grade A Warehousing Hampers Growth

The scarcity of modern, high-specification Grade A warehousing facilities presents a significant impediment to the growth of the Saudi Arabia Warehousing Market. This shortage creates a persistent supply-demand imbalance, particularly for advanced and automated storage solutions across key logistical hubs. Businesses, especially those in the burgeoning e-commerce and manufacturing sectors, face limitations in scaling operations efficiently due to the unavailability of suitable infrastructure. The lack of these high-quality facilities hinders the adoption of advanced logistics technologies and automation, leading to operational inefficiencies and increased costs throughout the supply chain.

Grade A Gap Limits Saudi Logistics Ambitions

Despite efforts to expand overall logistics infrastructure, the qualitative gap remains. According to the General Authority for Statistics (GASTAT), in 2024, the number of activated logistics centers in Saudi Arabia increased to 23, covering a total area of 34.6 million square meters. However, much of this existing and new capacity does not meet the Grade A specifications required for modern, efficient warehousing operations. This structural deficiency directly impacts the market's ability to support the Kingdom's economic diversification goals and its ambition to become a global logistics hub, as businesses struggle to find facilities that can accommodate sophisticated inventory management and rapid distribution needs.

Key Market Trends

Automation and Technology Transforming the Saudi Arabia Warehousing Market

Increased automation and technology adoption is significantly reshaping the Saudi Arabia Warehousing Market by enhancing operational efficiencies and throughput. Businesses are increasingly investing in advanced warehouse management systems, robotics, and artificial intelligence to optimize inventory management and accelerate order fulfillment. This strategic integration of technology is crucial for meeting escalating consumer demands and overcoming operational challenges. According to Supply Chain Digital, December 2025, in "Five trends shaping the future of warehousing in Middle East", autonomous robots are expected to process up to 50% of e-commerce orders by 2025, indicating a rapid shift towards automated solutions in fulfillment centers.

3PL Outsourcing Driving Growth in Saudi Arabia Warehousing

The growing trend of outsourcing to Third-Party Logistics (3PL) Providers is also fundamentally transforming the warehousing sector. Companies are leveraging 3PL expertise to manage complex logistics operations, access modern infrastructure, and scale supply chain capabilities without substantial capital expenditure. This enables businesses to focus on core competencies while benefiting from specialized logistics services. The expansion by 3PLs helps address the deficit of modern, high-specification warehousing facilities. This trend is further underscored by significant investments from global players; for instance, according to DC Velocity, November 2025, DHL Supply Chain announced plans to develop a $150 million facility in Saudi Arabia.

Segmental Insights

Outsource Warehousing: Growth Fueled by Vision 2030, E-commerce, and Government Support.

In the Saudi Arabia Warehousing Market, Outsource Warehousing is identified as the fastest growing segment, driven by several strategic factors. This rapid expansion is primarily fueled by the Kingdom's Vision 2030, which aims to diversify the economy and establish Saudi Arabia as a global logistics hub through significant infrastructure investment and regulatory reforms. Concurrently, the booming e-commerce sector demands highly efficient and agile supply chains, compelling businesses to seek specialized third-party logistics providers for advanced fulfillment and distribution capabilities. Outsourcing enables companies to leverage modern warehousing solutions, including automation and integrated technology, without the substantial initial capital investment. Furthermore, supportive government initiatives, such as the National Transport and Logistics Strategy and regulations overseen by the Ministry of Commerce, foster a structured and investment-friendly environment for outsourced logistics services.

Regional Insights

Eastern Province: Leading Logistics Hub Driven by Industrial Assets and Port Connectivity

The Eastern Province leads the Saudi Arabia Warehousing Market primarily due to its strategic industrial significance and robust logistical infrastructure. This region hosts major industrial cities such as Dammam and Jubail, which are key centers for petrochemicals, mining, and manufacturing, generating substantial demand for warehousing and distribution services. Furthermore, its access to vital maritime trade routes via major ports like King Abdulaziz Port and Jubail Commercial Port, along with continuous government investment in enhancing road and rail networks, solidifies its position as a dominant logistics hub facilitating efficient movement of goods for both domestic consumption and international trade.

Recent Developments

-

In November 2025, DHL Supply Chain announced a significant investment of EUR 130 million (approximately $150 million) to establish a new regional logistics and distribution hub within Saudi Arabia's Special Integrated Logistics Zone (SILZ) in Riyadh. This strategic initiative involves a 26-year land lease agreement and will culminate in a 53,000 square meter multi-user warehouse. The facility is designed to serve various sectors, including technology, retail, consumer goods, automotive, energy, and e-commerce, directly contributing to the expansion of warehousing capabilities in the Saudi Arabia Warehousing Market.

-

In August 2025, Starlinks launched its new Polaris warehouse in Riyadh, which integrated advanced AI automation and featured a capacity for 44,000 multi-temperature pallets. This facility was designed to enhance efficiency specifically for pharmaceutical and food cold chain operations. The introduction of this technologically advanced warehouse underscored a significant step in deploying innovative solutions within the specialized segment of the Saudi Arabia Warehousing Market, catering to stringent temperature-controlled storage requirements.

-

In April 2025, it was reported that during the preceding year, Saudi property developer Kaden collaborated with global logistics provider DB Schenker to enhance logistics capabilities within the Kingdom. This partnership aimed at expanding warehousing and distribution networks, addressing the increasing demand for advanced logistics infrastructure in the Saudi Arabia Warehousing Market. Such strategic alliances underscore the growing trend of international and local companies joining forces to develop sophisticated storage and distribution solutions across the region.

-

In January 2025, Aramex introduced an advanced automated robotic sortation system at Jeddah Islamic Port. This technological enhancement was capable of processing up to 96,000 parcels on a daily basis, significantly boosting efficiency and speed in parcel handling operations. The implementation of this automated solution reflected a commitment to integrating breakthrough research in robotics and automation into operational processes, directly impacting the capabilities and technological sophistication of the Saudi Arabia Warehousing Market.

Key Market Players

- Aramex KSA

- DHL KSA

- Kuehne+Nagel KSA

- DB Schenker KSA

- Maersk KSA

- DP World KSA

- Agility KSA

- CEVA Logistics KSA

- Gulf Logistics KSA

- Al Futtaim Logistics

|

By Type

|

By Ownership

|

By Size

|

By Region

|

- Insource Warehousing

- Outsource Warehousing

|

- Public Warehouses

- Private Warehouses

- Bonded Warehouses

- Consolidated Warehouse

|

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Warehousing Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Warehousing Market, By Type:

-

Insource Warehousing

-

Outsource Warehousing

-

Saudi Arabia Warehousing Market, By Ownership:

-

Public Warehouses

-

Private Warehouses

-

Bonded Warehouses

-

Consolidated Warehouse

-

Saudi Arabia Warehousing Market, By Size:

-

Saudi Arabia Warehousing Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Warehousing Market.

Available Customizations:

Saudi Arabia Warehousing Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Warehousing Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com