|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

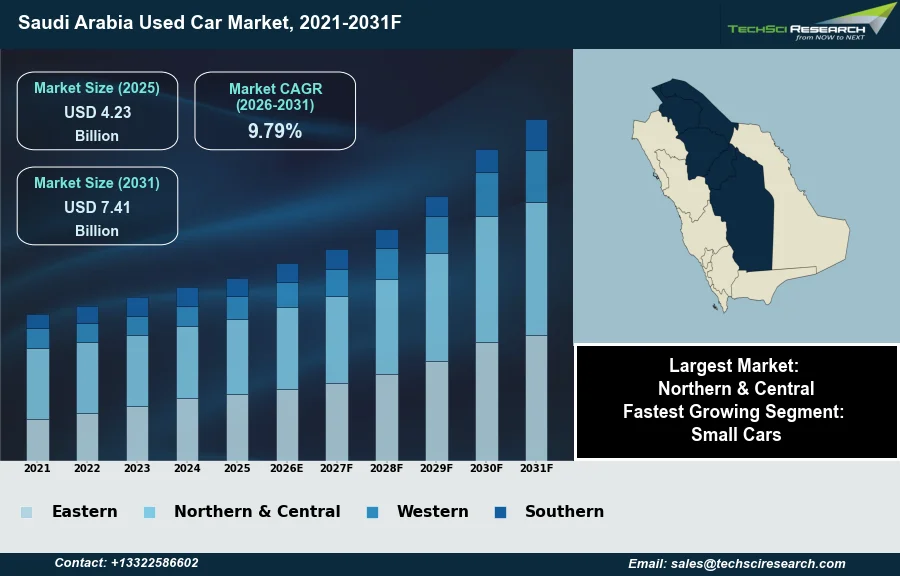

Market Size (2025)

|

USD 4.23 Billion

|

|

CAGR (2026-2031)

|

9.79%

|

|

Fastest Growing Segment

|

Small Cars

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 7.41 Billion

|

Market Overview

The Saudi Arabia Used Car Market will grow from USD 4.23 Billion in 2025 to USD 7.41 Billion by 2031 at a 9.79% CAGR. The Saudi Arabia used car market encompasses the trade of pre-owned vehicles, including passenger cars, SUVs, and commercial vehicles, which have been previously registered and operated by one or more end-users. This market's growth is predominantly driven by several fundamental factors. A significant driver is the increasing demand for affordable transportation, largely influenced by the elevated prices of new vehicles and the rising cost of living, which encourages consumers to seek more economical alternatives. The expanding population base and ongoing urbanization further contribute to a larger pool of potential vehicle owners, while the increasing participation of women in driving, following policy changes, has substantially broadened the consumer demographic. Additionally, the relatively high depreciation rate of new vehicles makes used cars a financially attractive option, with favorable auto financing solutions enhancing accessibility for a wider range of buyers.

Despite these robust growth drivers, the market faces notable impediments. A significant challenge lies in the fragmented nature of the market and the lack of comprehensive regulatory oversight, particularly within the unorganized segments. This fragmentation can lead to issues with vehicle history transparency, inconsistent pricing, and limited consumer protection mechanisms, thereby eroding buyer confidence. According to the U.S. International Trade Administration, total vehicle sales in Saudi Arabia were projected to reach 543,000 units by 2025, underscoring the broader automotive sector's scale.

Key Market Drivers

Digital marketplaces expand accessibility and transparency in the Saudi used-car market

The expansion of online sales channels and digital marketplaces significantly propels the Saudi Arabia used car market by enhancing accessibility and transparency for consumers. These platforms offer a broad selection of vehicles, enabling buyers to compare prices, features, and historical data with unprecedented ease. This digital transformation simplifies the purchasing journey, often including virtual inspections and streamlined documentation processes, which builds buyer confidence in pre-owned vehicles. According to YallaMotor, in 2024, the platform saw a 14.4% year-over-year increase in average monthly active users, reflecting the growing consumer reliance on digital avenues for used car transactions.

Expanded financing accessibility broadens the used-car market reach

Furthermore, improved used car financing accessibility plays a crucial role in expanding the market's reach by making vehicle ownership attainable for a wider demographic. Financial institutions are increasingly offering tailored loan products for used cars, including more flexible terms and competitive interest rates, which cater to varying consumer needs. This enhanced access to credit empowers individuals, particularly the middle-class and first-time buyers, to invest in personal transportation. According to the Saudi Central Bank, finance company credit reached SR96.26 billion in 2024, indicating a robust growth in lending across the financial sector that includes automotive financing. Overall, Saudi Arabia Motor Vehicles Sales recorded 805,034 units in December 2024, underscoring the substantial activity within the broader automotive sector.

Download Free Sample Report

Key Market Challenges

Market fragmentation and limited regulatory oversight erode trust and impede growth

A significant challenge within the Saudi Arabia used car market stems from its fragmented nature and the lack of comprehensive regulatory oversight, particularly within the unorganized segments. This structural issue directly impedes market growth by fostering opacity regarding vehicle history, leading to inconsistent pricing practices, and offering limited consumer protection mechanisms. Consequently, buyers face considerable difficulty in verifying the true condition, mileage, or accident history of pre-owned vehicles, which fundamentally erodes trust and discourages purchasing decisions.

Regulatory gaps and lack of redress constrain the used-car market despite broader automotive expansion

The absence of standardized regulations and clear channels for redress makes consumers wary of potential undisclosed defects or unfair valuations. This uncertainty surrounding vehicle provenance and transactional integrity restricts the market's potential, as a substantial portion of prospective buyers may opt out or delay purchases due to perceived risks. According to the General Authority for Statistics, in March 2026, the wholesale and retail trade and repair of motor vehicles activity in Saudi Arabia experienced an increase of 4.6% compared to March 2025. While reflecting broader automotive sector growth, this highlights the considerable unrealized potential within the used car segment where fragmentation continues to constrain consumer confidence and market expansion.

Key Market Trends

Rising Demand for Newer Used Models Driven by Fresh Vehicle Imports

A notable trend in the Saudi Arabia used car market is the increasing demand for newer used vehicle models. This reflects a consumer shift towards more contemporary features, improved fuel efficiency, and enhanced reliability, seeking options closer to new car technology without the full price. This trend is indirectly supported by the robust influx of new vehicles, which subsequently increases the pool of relatively newer models for resale. According to the Al-Arabiya.net report, citing data from the Saudi Zakat, Tax and Customs Authority (ZATCA), vehicle imports to Saudi Arabia reached approximately 942,118 units in 2024. This continuous replenishment of the overall fleet addresses evolving consumer expectations for up-to-date options.

Leasing and Subscription Growth Expands the Used-Car Inventory

Another significant development is the growth of car subscription and leasing return models, influencing the used car market's supply dynamics. These alternative ownership solutions offer flexibility, lower upfront costs, and predictable expenses for consumers and businesses. Upon contract conclusion, a consistent stream of well-maintained, relatively new vehicles re-enters the used car inventory, often through organized channels. This provides a reliable source of high-quality used cars, boosting confidence. According to GIB Capital's 'Saudi Car Rental Sector' report in June 2025, the aggregate leasing fleet in Saudi Arabia is projected to grow at a Compound Annual Growth Rate of 6% over 2024-2028, surpassing 105,000 vehicles. This expansion directly contributes to a structured, high-volume pipeline for the used car market.

Segmental Insights

Expansion of Small Cars in the Saudi Arabia Used Car Market

The Small Cars segment represents a key area of rapid expansion within the Saudi Arabia Used Car Market. This growth is predominantly driven by increasing demand for accessible and affordable transportation solutions, particularly from an expanding demographic of first-time buyers and the expatriate population. Enhanced urbanization and evolving consumer priorities towards value contribute significantly, as small cars offer superior fuel efficiency and improved maneuverability, making them a practical and economical choice for urban environments and diverse new owners. This trend reflects a market where cost-effectiveness and operational practicality are becoming increasingly pivotal purchase considerations.

Regional Insights

Northern & Central Region Drives Saudi Used Car Market Dominance

The Northern & Central region leads the Saudi Arabia Used Car Market primarily due to its significant economic activity and high population density. Riyadh, serving as the capital and a major urban center, acts as a crucial hub for both commercial and governmental operations, generating substantial demand for private vehicles among professionals and middle-income families. Additionally, the region's considerable expatriate workforce consistently drives the need for affordable transportation solutions. The well-developed infrastructure in cities like Riyadh, encompassing accessible vehicle inspection centers and varied financing options, cultivates an organized and active used car ecosystem. These combined factors underscore the Northern & Central region's market dominance.

Recent Developments

-

In October 2025, Cartea introduced a complimentary car selling service for users throughout the Gulf Cooperation Council, including Saudi Arabia. This new digital platform was launched to meet the increasing demand for online vehicle transactions. The service provides a secure, convenient, and reliable method for individuals to list their used cars and connect with potential buyers, integrating features such as region-based price suggestions. This initiative aimed to enhance transparency and streamline the sales process within the Saudi Arabia Used Car Market.

-

In October 2024, the Motor Vehicle Periodic Inspection (MVPI), operating under the oversight of the Saudi Standards, Metrology, and Quality Organization, launched six mobile vehicle inspection stations. This expansion of services aimed to enhance the accessibility of detailed vehicle assessments across Saudi Arabia. The introduction of these mobile stations directly benefited the Saudi Arabia Used Car Market by providing more convenient and advanced technological tools for inspecting used vehicles, offering buyers and sellers greater transparency regarding a car's condition.

-

In June 2024, TUV Rheinland, a global technical services provider, formed a strategic partnership with the Saudi Standards, Metrology and Quality Organization (SASO). This collaboration was established to ensure comprehensive quality and compliance verification for imported used cars entering the Saudi Arabian market. The initiative aimed to verify that these vehicles adhere to national and international regulations, thereby increasing consumer confidence in pre-owned vehicle purchases. This development is directly linked to the Saudi Arabia Used Car Market by reinforcing standards for vehicle quality and safety.

-

In May 2024, Dubizzle Motors completed the acquisition of Drive Arabia, a move designed to integrate advanced AI-driven valuation tools into its operations. This strategic development directly impacts the Saudi Arabia Used Car Market by aiming to significantly reduce the time required for vehicle inspections. The implementation of artificial intelligence technology is intended to improve the efficiency and accuracy of assessing pre-owned vehicles, thereby fostering greater confidence and transparency for both buyers and sellers in used car transactions.

Key Market Players

- Dubizzle Cars KSA

- Yallamotor KSA

- Cars24 KSA

- CarSwitch KSA

- Auto1 Group KSA

- Al Futtaim Used Cars

- Al Habtoor Used Cars

- Al Tayer Used Cars

- Premier Motors Used

- Emirates Motors KSA

|

By Vehicle Type

|

By Fuel Type

|

By End Use

|

By Region

|

- Small Cars

- Mid-Size Cars

- Luxury Cars

|

|

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Used Car Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Used Car Market, By Vehicle Type:

-

Small Cars

-

Mid-Size Cars

-

Luxury Cars

-

Saudi Arabia Used Car Market, By Fuel Type:

-

Saudi Arabia Used Car Market, By End Use:

-

Saudi Arabia Used Car Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Used Car Market.

Available Customizations:

Saudi Arabia Used Car Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Used Car Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com