|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 5.78 Billion

|

|

CAGR (2026-2031)

|

6.24%

|

|

Fastest Growing Segment

|

Passenger Cars

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 8.31 Billion

|

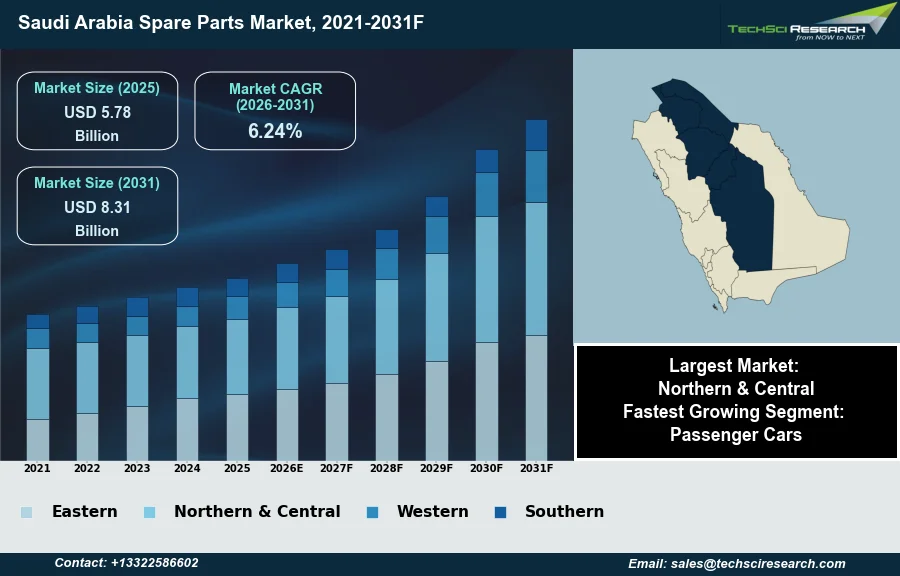

Market Overview

The Saudi Arabia Spare Parts Market will grow from USD 5.78 Billion in 2025 to USD 8.31 Billion by 2031 at a 6.24% CAGR. Spare parts encompass individual components or sub-assemblies designed for the repair, maintenance, or replacement of existing parts within machinery, equipment, or vehicles, ensuring operational continuity and extending asset lifespans. The Saudi Arabia spare parts market is primarily driven by a steadily expanding national vehicle parc and concerted government initiatives under Vision 2030, which strategically foster industrial diversification and promote local manufacturing capabilities. Additionally, the kingdom's harsh climatic conditions accelerate component wear and tear, necessitating more frequent replacements.

According to Saudi Arabia import data on TradeInt, imports of vehicles and auto parts (HS 87) were valued at USD 15.60 billion in 2025, underscoring significant market activity. However, a substantial challenge impeding market expansion is the heavy dependence on imported components, reflecting an underdeveloped domestic manufacturing ecosystem that, despite ongoing localization efforts, exposes the market to international supply chain vulnerabilities.

Key Market Drivers

Growth in vehicle fleet drives spare parts demand

The expanding vehicle fleet and ownership in Saudi Arabia represent a primary driver for the spare parts market. As the number of vehicles on the roads continues to grow, so does the demand for maintenance, repair, and replacement components to ensure operational longevity. According to an Al-Arabiya.net report, citing Zakat, Tax and Customs Authority data, vehicle imports to Saudi Arabia reached approximately 959,403 units by 2025, directly contributing to the increasing national vehicle parc and, consequently, the sustained need for spare parts across various categories.

Vision 2030 localization boosts domestic automotive manufacturing

Another significant driver is Saudi Vision 2030 and its localization initiatives, aiming to diversify the economy and build domestic manufacturing capabilities within the automotive sector. These strategic efforts foster local production of spare parts, reducing reliance on imports and strengthening the in-country value chain. For instance, according to Sharikat Mubasher, during the PIF Private Sector Forum 2026, CEER concluded 16 agreements worth over SAR 3.7 billion to fuel the local automotive industry in the Kingdom. Furthermore, the broader automotive sector continues to attract substantial investment, with companies under the Public Investment Fund having attracted approximately SAR 57 billion in direct foreign investment across emerging and new sectors, including automotive, through Q3 2025, according to Gulf Daily News.

Download Free Sample Report

Key Market Challenges

Import dependence and underdeveloped manufacturing hinder market expansion and pricing stability.

A significant challenge impeding the Saudi Arabia spare parts market is its heavy reliance on imported components, which reflects an underdeveloped domestic manufacturing ecosystem. This dependence directly hampers market expansion by exposing it to international supply chain vulnerabilities. Such reliance can lead to increased costs due to fluctuating foreign exchange rates, higher transportation expenses, and potential delays in product availability, all of which impact market efficiency and pricing stability.

Near-total import reliance on automotive spare parts constrains domestic industry growth and supply resilience.

According to WifiTalents, in February 2026, Saudi Arabia imported approximately 95% of its automotive spare parts, highlighting the minimal local production contribution. This substantial import dependency restricts the growth of a robust domestic industry, limiting opportunities for technology transfer, local job creation, and the development of a resilient in-country value chain. The absence of a mature local supplier network means the market remains susceptible to external economic pressures and geopolitical uncertainties, thereby hindering the consistent and predictable supply of essential spare parts.

Key Market Trends

Digitalization of Aftermarket Channels Reshapes Saudi Arabia Spare Parts Market

The digitalization of aftermarket sales channels is profoundly reshaping the Saudi Arabia spare parts market by enhancing accessibility and streamlining procurement for consumers and businesses alike. This trend involves a significant shift towards online platforms, e-commerce websites, and digital marketplaces that offer broader product ranges, transparent pricing, and convenient delivery options, thereby reducing reliance on traditional physical outlets. Such digital advancements foster greater market efficiency and allow for more informed purchasing decisions. According to E-Commerce Saudi Arabia 2025: Market Size and Growth, updated May 6, 2026, the transaction value for broader digital commerce channels in Saudi Arabia reached an estimated SAR 90-100 billion in 2024. This robust growth in the overall digital economy directly facilitates the expansion and maturity of online spare parts distribution.

Electric-Vehicle Growth Drives High-Tech Spare Parts Demand

Concurrently, the rise in electric vehicle and high-tech component demand presents a transformative shift within the spare parts landscape, necessitating specialized inventory and technical expertise. As the kingdom advances its sustainability goals under Vision 2030, the composition of the national vehicle fleet is evolving, moving towards electric and hybrid models that require distinct powertrain, battery, and electronic control unit components for maintenance and repair. This shift mandates significant adjustments in supply chains and aftermarket services. According to Arab News, May 30, 2026, citing the International Energy Agency, EV sales in the Middle East reached approximately 75,000 units in 2025, with Saudi Arabia and Qatar jointly accounting for about 45 percent of this regional demand. This indicates a growing segment requiring specific high-tech spare parts.

Segmental Insights

Growth Drivers for Passenger Cars: Ownership Rise, Aging Fleet, and MVPI Regulation

The Passenger Cars segment stands out as the fastest-growing category within the Saudi Arabia Spare Parts Market. This rapid expansion is fundamentally driven by a significant increase in vehicle ownership, fueled by a growing population, rising disposable incomes, and the impactful reforms allowing women to drive. Concurrently, an aging vehicle fleet necessitates more frequent maintenance and component replacements. Furthermore, stringent regulatory mandates, particularly the Motor Vehicle Periodic Inspection (MVPI) program, overseen by the Saudi Standards, Metrology and Quality Organization (SASO), compel vehicle owners to undertake regular part purchases to ensure safety and compliance, thereby sustaining robust aftermarket demand.

Regional Insights

Drivers of the Northern & Central Region’s Spare Parts Market Leadership

The Northern & Central region is the leading area within the Saudi Arabia Spare Parts Market due to a convergence of critical factors. This dominance is primarily driven by its high concentration of vehicles, stemming from dense urban populations and significant urbanization across its major cities, including the capital. The region benefits from extensive transportation infrastructure, which supports both private and commercial vehicle usage, thereby stimulating consistent demand for maintenance and replacement components. Furthermore, as a key economic, business, and administrative hub, the Northern & Central region hosts a substantial corporate fleet and a high density of dealerships, service centers, and distribution networks, ensuring efficient access to a wide array of spare parts. This robust ecosystem, combined with a considerable aging vehicle fleet, underpins the region's prominent position in the market.

Recent Developments

-

In July 2025, Partfinder UAE announced its expansion into the Saudi Arabian market with the launch of its digital platform for spare part sourcing. This new service aimed to provide workshops and individual consumers across the Kingdom with a more efficient and transparent method for acquiring automotive spare parts. The platform connects users with verified sellers, offering features like real-time availability and compatibility checks. This technological introduction was poised to enhance accessibility and optimize the procurement process within the Saudi Arabian spare parts market.

-

In May 2025, SOUEAST Motor Co. Ltd. inaugurated its first dedicated spare parts center in Saudi Arabia, a key development realized through its partnership with Starlinks. This new 10,000-square-meter facility in Jeddah was designed to significantly enhance after-sales support and streamline the distribution of essential automotive components across the Kingdom. The establishment of this center aimed to improve product availability and service efficiency, directly supporting SOUEAST vehicle owners throughout the Saudi Arabian spare parts market.

-

In December 2024, Al-Kadi Commerce & Industry and FORVIA HELLA, a global leader in automotive technology, formalized a "Sharaka" (partnership) agreement. This collaboration designated Al-Kadi Commerce & Industry as the sole distributor for FORVIA HELLA's automotive aftermarket products in Saudi Arabia. The agreement also focused on initiatives for local manufacturing and knowledge transfer, aligning with national economic diversification goals. This partnership was intended to bolster domestic production capabilities and enhance the supply chain within the Saudi Arabian spare parts market.

-

In July 2024, the National Additive Manufacturing & Innovation Company (NAMI), a joint venture, partnered with the Saudi Electricity Company (SEC) to implement an advanced digital spare parts inventory system. This collaboration focused on leveraging 3D printing technologies to enable faster, on-demand production of replacement components for the energy sector within Saudi Arabia. The initiative explored "NoSupports" printing techniques, anticipating a reduction in physical storage requirements and operational costs, thereby enhancing the efficiency of the Saudi Arabian spare parts market.

Key Market Players

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Panasonic Corporation

- Magna International Inc

- Lear Corporation

- Faurecia S.A.

- Visteon Corporation

- Yanfeng Spare Partss

- Faurecia SE

|

By Vehicle Type

|

By Component Type

|

By Distribution Channel

|

By Region

|

- Passenger Cars

- Commercial Vehicles

|

- Tires

- Batteries

- Air Filter

- Brake Shoe

- Spark Plugs

- Brake Pad

- Brake Caliper

- Other

|

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Spare Parts Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Spare Parts Market, By Vehicle Type:

-

Passenger Cars

-

Commercial Vehicles

-

Saudi Arabia Spare Parts Market, By Component Type:

-

Tires

-

Batteries

-

Air Filter

-

Brake Shoe

-

Spark Plugs

-

Brake Pad

-

Brake Caliper

-

Other

-

Saudi Arabia Spare Parts Market, By Distribution Channel:

-

Saudi Arabia Spare Parts Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Spare Parts Market.

Available Customizations:

Saudi Arabia Spare Parts Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Spare Parts Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com