|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

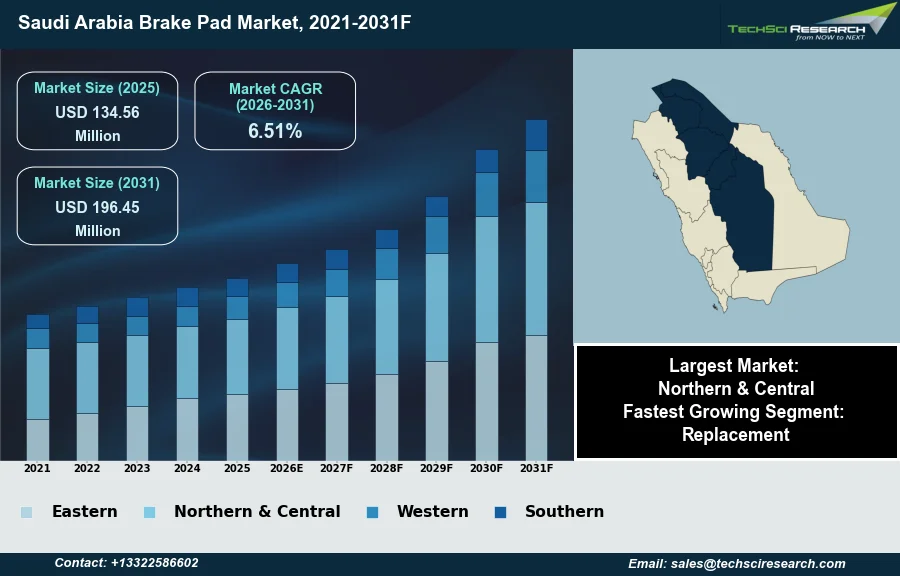

Market Size (2025)

|

USD 134.56 Million

|

|

CAGR (2026-2031)

|

6.51%

|

|

Fastest Growing Segment

|

Replacement

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 196.45 Million

|

Market Overview

The Saudi Arabia Brake Pad Market will grow from USD 134.56 Million in 2025 to USD 196.45 Million by 2031 at a 6.51% CAGR. Brake pads are critical friction components within a vehicle's braking system, engineered to convert kinetic energy into thermal energy to decelerate or stop a vehicle through controlled friction with brake rotors. The Saudi Arabia brake pad market is significantly supported by the nation's expanding vehicle fleet and consistent new vehicle sales, which directly drive aftermarket demand for replacement parts. According to the International Organization of Motor Vehicle Manufacturers (OICA), new vehicle sales in Saudi Arabia reached 705,527 units in 2024, projected to increase to 827,544 units in 2025. Key growth drivers also include population expansion, rising disposable incomes, and governmental initiatives like Vision 2030 that foster economic diversification and infrastructure development.

Moreover, the increasing participation of female drivers in the automotive sector and the demanding local climatic conditions contribute to a higher frequency of maintenance and replacement cycles for wear-and-tear components such as brake pads. Nevertheless, a notable impediment to market expansion remains the widespread availability of counterfeit and substandard automotive parts, which poses significant safety risks and diminishes consumer confidence in legitimate products.

Key Market Drivers

Growing Vehicle Fleet and Ownership Drive Brake Pad Demand

The expanding vehicle parc and continued growth in ownership are primary drivers for the Saudi Arabia brake pad market. As more individuals acquire vehicles, the overall demand for both original equipment and aftermarket brake pads naturally increases, reflecting a larger base for replacements over time. This trend is significantly bolstered by evolving societal dynamics; for instance, according to WifiTalents, in February 2026, over 2 million women have obtained driving licenses since the lifting of the driving ban in 2018. This demographic shift expands the overall number of active drivers and, consequently, the vehicle fleet, necessitating more frequent maintenance and replacement of wear-and-tear components such as brake pads.

Aging Fleet and Production Targets Sustain Brake Pad Demand

Concurrently, the aging vehicle fleet within Saudi Arabia contributes substantially to heightened aftermarket demand for brake pads. Older vehicles typically require more frequent maintenance and component replacements compared to newer models. This is evident as, according to WifiTalents, in February 2026, the average age of vehicles on Saudi roads is 8.5 years. Such an aging fleet directly translates into a sustained and growing need for replacement brake pads. The government's strategic initiatives further support the automotive sector, with the Ministry of Investment indicating in November 2025 that Saudi Arabia aims to produce 300,000 to 350,000 vehicles annually by 2030, which will also impact the demand for brake pads in both OEM and aftermarket channels.

Download Free Sample Report

Key Market Challenges

Counterfeit Brake Pads: Impact on Saudi Market Growth and Consumer Confidence

The widespread availability of counterfeit and substandard automotive parts poses a notable impediment to the growth of the Saudi Arabia brake pad market. These illicit products, frequently offered at lower prices, divert consumer demand away from legitimate manufacturers and distributors. This directly curtails revenue generation for authentic brake pad suppliers and undermines market stability. Furthermore, the inferior quality of counterfeit brake pads compromises vehicle safety and often leads to premature failure, requiring frequent and unexpected replacements. This erodes consumer confidence in the reliability and safety of aftermarket brake components within the Kingdom. According to Saudi authorities, over 3.6 million counterfeit goods were seized in a coordinated campaign in December 2025, highlighting the significant presence of illicit products across various consumer sectors, including automotive parts. This pervasive issue reduces the incentive for reputable companies to invest in quality manufacturing and innovation, thereby stagnating overall market development for genuine brake pads.

Key Market Trends

Sustainable Brake Pads and Circular-Economy Goals

The increasing demand for environmentally sustainable brake pads represents a significant trend in the Saudi Arabian market. This shift is primarily driven by the Kingdom's ambitious environmental goals under Vision 2030 and initiatives like the Saudi Green Initiative, which advocate for reduced emissions and a circular economy. Consumers and regulators alike are increasingly favoring brake pads that are free from harmful materials such as copper and asbestos, opting instead for formulations that minimize environmental impact throughout their lifecycle. This preference is fostering innovation in material science, pushing manufacturers to develop advanced friction materials that offer comparable or superior performance with a smaller ecological footprint. According to MDPI, April 2025, in 'A Comparative Analysis of Circular Economy Practices in Saudi Arabia', the Saudi Investment Recycling Company (SIRC) targets an 81% recycling rate by 2035, underscoring the growing emphasis on sustainable material usage in the automotive sector.

EV Brake Pad Needs and Domestic Localization Push

Concurrently, the specialized brake pad requirements for electric vehicles (EVs) are emerging as another pivotal trend shaping the market. As Saudi Arabia actively invests in developing its domestic EV manufacturing capabilities and promoting EV adoption, the demand for brake pads uniquely suited to these vehicles is set to grow. EVs typically require quieter brake pads due to the absence of engine noise, as well as formulations that complement regenerative braking systems, leading to different wear patterns and longevity expectations compared to conventional internal combustion engine vehicles. This necessitates specialized research and development in friction materials. According to the Saudi Ministry of Investment, January 2026, the National Industrial Strategy aims to localize the automotive industry by 2035 with a production capacity of up to 600,000 vehicles annually, a significant portion of which will be electric, thereby driving specific demand for EV brake pad technologies.

Segmental Insights

Replacement Segment: Key Growth Driver Fueled by Fleet Dynamics, Harsh Environment, and Regulatory Compliance

The Replacement segment is a primary growth driver in the Saudi Arabia Brake Pad Market, experiencing rapid expansion due to several interconnected factors. A consistently increasing vehicle parc, coupled with an aging vehicle fleet and extended ownership periods, inherently escalates the demand for periodic maintenance and component replacements. Furthermore, Saudi Arabia's challenging environmental conditions, characterized by high temperatures and dusty environments, along with prevalent stop-and-go city traffic, accelerate brake pad wear, thereby necessitating more frequent replacements. This demand is further propelled by rising consumer awareness regarding vehicle safety and the importance of timely maintenance, alongside stringent safety regulations for automotive parts, including brake pads, enforced by entities such as the Saudi Standards, Metrology and Quality Organization (SASO).

Regional Insights

Northern and Central Saudi Arabia: Demand Leader for Brake Pads

Northern & Central Saudi Arabia leads the brake pad market, primarily driven by its significant economic activity, high population density, and concentrated vehicle registrations. Riyadh, as the Kingdom's commercial and administrative hub, centralizes these factors, fostering substantial vehicle ownership and frequent usage, which directly increases brake pad wear and replacement demand. The region's extensive transportation infrastructure further supports heightened vehicle utilization and its role as a key distribution hub for automotive components. Government initiatives, including Vision 2030, coupled with stringent safety standards enforced by the Saudi Standards, Metrology and Quality Organization (SASO), bolster the demand for certified, high-quality braking components across this dominant region.

Recent Developments

-

In April 2025, Brembo S.p.A. unveiled its innovative GREENTELL brake disc and pad set, which featured advanced coating technology engineered to reduce brake dust emissions by up to 90 percent. This product development aligned with the increasingly stringent environmental regulations, such as forthcoming Euro 7 standards. While globally introduced at Auto Shanghai, the availability of such high-performance and environmentally conscious braking solutions is relevant to the Saudi Arabia brake pad market, which is experiencing a growing demand for advanced and sustainable automotive components.

-

In March 2025, Tenneco Inc. launched its Ferodo Eco-Cycle brake pad line, developed with over 60 percent reclaimed friction material from end-of-life pads. This product introduction marked a substantial step towards fostering a circular economy within the automotive aftermarket. As a significant global manufacturer supplying the Saudi market, the integration of these sustainable friction materials contributes to the ongoing technological advancements in the Saudi Arabia brake pad market. This initiative supports the increasing industry focus on environmental responsibility and resource efficiency.

-

In October 2024, FORVIA HELLA, a prominent global automotive supplier, launched its comprehensive range of brake products under the HELLA brand. This offering, encompassing various braking components including brake pads, was introduced after the company's acquisition of the HELLA PAGID joint venture. Notably, FORVIA HELLA expanded its presence by launching truck-related brake products in the Middle East, aiming to leverage its original equipment expertise. This strategic development significantly impacted the availability and diversity of braking solutions within the Saudi Arabia brake pad market.

-

In June 2024, Stellantis announced the introduction of its bproauto brand of aftermarket parts and products across the Middle East. This launch featured essential components such as brake pads, brake rotors, air filters, and oil filters, all competitively priced and offering a two-year warranty. The bproauto line was designed to fit most automotive makes and models, fulfilling the company’s strategic objective to expand its presence in the independent aftermarket segment. This initiative enhanced the range of options for vehicle maintenance and repair services in the Saudi Arabia brake pad market.

Key Market Players

- Bosch Brake KSA

- Brembo KSA

- TRW KSA

- Ferodo KSA

- Al Futtaim Brake

- Al Habtoor Brake

- Al Tayer Brake

- Local Brake Suppliers KSA

- Al Rajhi Brake

- Manlift Brake

|

By Material Type

|

By Vehicle Type

|

By Demand Category

|

By Region

|

- Semi-Metallic

- Ceramic

- Others

|

- Passenger Car

- Commercial Vehicle

- Two-Wheeler

|

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Brake Pad Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Brake Pad Market, By Material Type:

-

Semi-Metallic

-

Ceramic

-

Others

-

Saudi Arabia Brake Pad Market, By Vehicle Type:

-

Passenger Car

-

Commercial Vehicle

-

Two-Wheeler

-

Saudi Arabia Brake Pad Market, By Demand Category:

-

Saudi Arabia Brake Pad Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Brake Pad Market.

Available Customizations:

Saudi Arabia Brake Pad Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Brake Pad Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com