|

Forecast Period

|

2026-2030

|

|

Market Size (2024)

|

USD 12.18 Billion

|

|

CAGR (2025-2030)

|

13.5%

|

|

Fastest Growing Segment

|

Residential

|

|

Largest Market

|

North

|

|

Market Size (2030)

|

USD 26.03 Billion

|

Market Overview

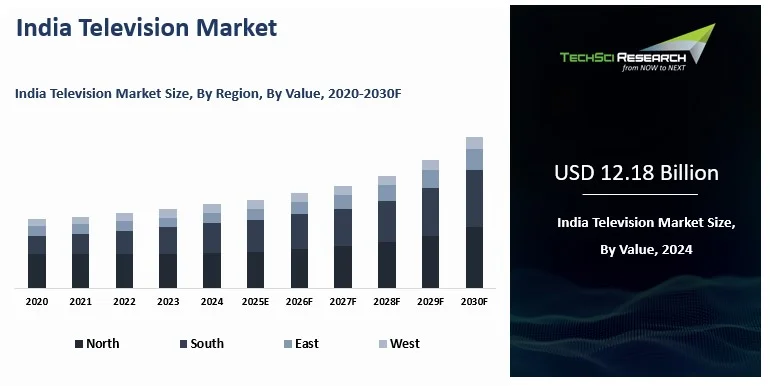

Television Market in India Size valued at USD 12.18 billion in 2024, is expected to grow to USD 26.03 billion by 2030, reflecting a robust compound annual growth rate (CAGR) of 13.5% from 2025 to 2030. The television industry has undergone a remarkable transformation, shifting from bulky CRT units to sleek, high-definition smart TVs with immersive sound and advanced connectivity. During 2025–2026, the market is entering a strong premiumization phase, driven by rising demand for advanced display technologies such as QLED, Mini-LED, and OLED. Smart TV shipments grew 8.6% year over year in 2024, reaching 12.1 million units, with Samsung leading the market at 16.1%, followed by LG at 15.1%. Although the market recorded healthy annual growth in 2024, shipment momentum moderated in early 2025 due to inflationary pressure and cautious consumer spending. At the same time, consumers in urban and upper-income segments are increasingly shifting toward premium global brands, while budget-focused manufacturers face stronger competitive pressure.

A significant shift in consumer preferences is also evident, with larger screens gaining popularity across urban households. The once-dominant 32-inch and 43-inch categories are gradually being complemented by increasing demand for larger panels, with shipments of 55-inch and above televisions rising 43% in 2024 and 65-inch models surging 75%. The growing home cinema trend has significantly increased the adoption of 4K televisions, particularly in mid-range and premium categories. Despite the continued strength of e-commerce platforms, organized offline retail, including large-format electronics stores and multi-brand retail chains, witnessed strong growth in 2024 as consumers increasingly preferred hands-on demonstrations of advanced AI-enabled televisions before purchase.

The broader Media and Entertainment sector in India, valued at approximately USD 30 billion in 2024, is expected to reach USD 100 billion by 2030, supporting television demand through rising OTT consumption, sports broadcasting, regional content expansion, and connected home entertainment adoption. While television has traditionally been the primary revenue driver within the entertainment ecosystem, digital media is expected to surpass linear television revenue by the end of 2026. This transition is reflected in evolving viewer behavior, as traditional pay-TV households gradually decline while Connected TV households continue to expand rapidly, surpassing 30 million homes. As affluent consumers increasingly shift toward OTT platforms and 5G-enabled streaming services, traditional broadcasters are becoming more dependent on regional and price-sensitive audiences, leading to pressure on premium advertising revenues despite stable overall viewing engagement.

Download Free Sample Report

Key Market Drivers

Premiumization of consumer preferences

Premiumization is becoming a defining force in the India television market as consumers increasingly move beyond entry-level sets and evaluate televisions on picture quality, design, smart features, sound performance, and overall lifestyle value. This shift is especially visible in urban households, where televisions are no longer treated as basic appliances but as central entertainment products that reflect aspiration, digital habits, and home aesthetics.

As OTT viewing, gaming, and connected entertainment become more important, buyers are showing stronger interest in QLED, OLED, AI-enabled, and feature-rich models that offer a visibly better experience than standard HD televisions. Premiumization is also being supported by wider product availability, financing options, and online comparison tools that make technology upgrades easier to understand and justify. This is gradually increasing willingness among Indian consumers to trade up within organized retail and e-commerce channels, particularly when replacement purchases are linked to better content quality and enhanced in-home viewing.

For Instance, Samsung India lists its 55-inch Neo QLED 4K Smart TV at ₹79,990 and its 55-inch QLED 4K AI Smart TV at ₹64,990, reflecting the premium price bands Indian consumers are increasingly entering for advanced televisions.

Growth in large-screen demand

Growth in large-screen demand is one of the clearest shifts in the India television market as households increasingly seek a more immersive viewing experience for streaming, live sports, gaming, and family entertainment. Larger televisions are gaining preference because they better suit urban living rooms and align with the rise of cinematic home viewing, where screen size has become a major purchase trigger alongside picture quality and smart functionality.

Consumers are also becoming more comfortable upgrading to 55-inch and above categories as financing options, festive promotions, and online-led price visibility narrow the affordability gap between mid-sized and large-screen models. This is encouraging brands to expand launches in larger form factors rather than limiting portfolios to entry-level sizes, especially in smart and 4K segments where aspirational demand is strongest. As viewing increasingly shifts toward long-form digital content and event-led entertainment, bigger screens are being seen as worthwhile household upgrades rather than occasional luxury purchases.

For Instance, Xiaomi launched its X Pro QLED 2025 television series in India in 43-inch, 55-inch, and 65-inch variants, with the 55-inch model priced at ₹44,999 and the 65-inch model at ₹64,999, underscoring the brand focus on larger screen categories.

4K resolution becoming the standard

4K resolution is becoming the preferred benchmark across mid-range and premium television segments in the India television market as declining price points and broader product availability make higher picture quality accessible to a wider consumer base. What was once considered a premium specification is increasingly moving toward mainstream adoption, particularly among consumers purchasing televisions for OTT streaming, live sports, and gaming applications where image clarity, color depth, and viewing performance are more noticeable. Manufacturers are accelerating this transition by introducing multiple 4K models across different price bands, allowing consumers to upgrade from HD and Full HD televisions without necessarily entering ultra-premium categories. The growing visibility of 4K televisions across online marketplaces and organized retail outlets is also normalizing Ultra HD as an expected feature within mid-range and premium segments rather than an aspirational upgrade.

For Instance, Xiaomi launched its 55-inch 4K TV FX in India at ₹36,999 and its 55-inch QLED FX Pro at ₹39,999, showing how 4K resolution is now being offered at increasingly reachable price points in the mainstream market.

Technological advancements in connectivity

Technological advancements in connectivity are strengthening product appeal in the India television market as consumers increasingly expect televisions to function as integrated digital hubs rather than passive display devices. Smart operating systems, voice support, app ecosystems, screen mirroring, casting features, and seamless smartphone compatibility are making televisions more relevant to everyday digital behavior inside the home.

This is especially important in India, where OTT consumption, mobile-first internet habits, and multi-device usage are pushing buyers toward televisions that connect easily with streaming services, gaming hardware, and connected home environments. As a result, replacement demand is being shaped not only by screen size and picture quality but also by how smoothly a television fits into a broader entertainment ecosystem. Brands that offer intuitive interfaces and stronger interoperability are therefore gaining an advantage because consumers increasingly value convenience, personalization, and low-friction access to content.

For Instance, the FICCI-EY report noted that connected TV homes in India increased to 30 million from 23 million in December 2023, highlighting how rapidly internet-enabled television usage is expanding across the country.

Media and entertainment growth

Growth in India’s media and entertainment ecosystem continues to support television demand by reinforcing the television set as a central screen for premium, shared, and event-led viewing experiences. Even as digital platforms expand, televisions remain highly relevant because they aggregate regional programming, OTT content, live sports, film premieres, and family entertainment in a format that is more immersive than mobile viewing.

The rise of regional language content is especially important, as viewers increasingly seek programming that reflects local identities and keeps television consumption deeply tied to India’s multilingual audience base. This strengthens the role of television in households that want access to both traditional broadcast channels and app-based entertainment through a single screen. Sports broadcasting adds another layer of demand because marquee events still drive collective viewing behavior and encourage upgrades to better screens, stronger audio, and smarter connected devices.

For Instance, the FICCI-EY report stated that the 2024 Indian Premier League reached 525 million viewers on television and 550 million to 600 million viewers on streaming, underscoring the scale of content-led engagement that sustains television relevance in India.

Key Market Challenges

Price sensitivity and affordability

Price sensitivity and affordability remain core challenges in the India television market because a large share of households, especially outside major urban centers, continues to prioritize upfront cost over advanced display quality, premium audio systems, or high-end smart features. Even when consumers show interest in upgraded televisions, final purchasing decisions are often influenced by discounts, festive offers, financing schemes, and overall screen-size value rather than by premium branding alone.

While premiumization is accelerating among affluent urban consumers and replacement buyers, affordability remains the primary purchase driver across price-sensitive and first-time buyer segments. This creates a challenging environment for manufacturers attempting to expand premium offerings, as demand can shift quickly toward lower-priced models during periods of inflationary pressure or weaker consumer sentiment. As a result, brands must carefully balance aspirational product positioning with competitive pricing and mass-market accessibility to strengthen their presence across India’s highly value-conscious television market.

Diverse consumer preferences and regional variances

Diverse consumer preferences and regional variances make the

India television market especially complex because purchase behavior differs

sharply by language, geography, household income, content habits, and digital

maturity. A television buyer in a metro city may prioritize screen size, OTT

access, and premium smart features, while a household in a smaller town may

focus more on affordability, regional channel compatibility, and reliable

everyday use.

This fragmentation makes it difficult for manufacturers to

rely on a single national strategy, since the same product proposition may

resonate differently across Hindi-speaking markets, southern states, and

fast-growing non-metro segments. Regional language consumption is particularly

important because television in India remains deeply tied to local

entertainment preferences, which means brands and content ecosystems must

reflect multilingual demand rather than assume uniform national viewing

behavior.

These regional variations influence not only content

preferences but also marketing, pricing, and channel strategy, raising

execution complexity for television brands competing across India’s broad and

highly segmented consumer landscape.

Intense competition and market saturation

Intense competition and growing saturation in urban smart TV categories continue to pressure the India television market as domestic and international brands compete aggressively for visibility and market share. Product differentiation is becoming increasingly difficult because many brands now offer similar baseline features such as smart interfaces, OTT app access, voice functionality, and larger screen sizes. This competitive environment is particularly intense across online and organized retail channels, where consumers can easily compare features and pricing across multiple brands. As a result, manufacturers are under constant pressure to refresh portfolios rapidly, increase promotional spending, and rely on discounts and channel incentives to protect market share. While significant growth opportunities still exist in Tier-2, Tier-3, and rural markets, urban categories are gradually approaching maturity, increasing the cost and complexity of acquiring incremental consumers profitably.

Infrastructure and connectivity issues

Infrastructure and connectivity issues remain a meaningful

barrier in the India television market because the value proposition of smart

and connected televisions depends heavily on reliable broadband, stable

electricity, and adequate last-mile digital access. In regions where internet

quality is inconsistent or power supply remains uneven, consumers may not

experience the full benefits of streaming, voice search, app-based viewing,

software updates, or connected home integration, reducing the practical appeal

of advanced televisions.

This challenge is

particularly relevant beyond major cities, where television demand exists but

infrastructure gaps can slow the transition from basic viewing devices to fully

connected entertainment screens. Although India’s digital ecosystem is

expanding rapidly, the market still reflects uneven readiness, which means

television brands cannot assume that smart feature adoption will progress

uniformly across all states and consumer segments. These connectivity constraints

also affect replacement demand because buyers in lower-infrastructure areas may

delay upgrading if they cannot use premium digital features consistently after

purchase.

For Instance, the government stated that under BharatNet

Phase I and Phase II, 2,14,904 Gram Panchayats were service ready out of

2,22,341 undertaken, showing progress but also indicating that connectivity

rollout is still uneven across rural India.

Technological obsolescence and rapid advancements

Technological obsolescence and rapid advancements pose a

persistent challenge in the India television market because display technology,

smart operating systems, connectivity features, and screen-size preferences are

evolving faster than many consumers and retailers can comfortably absorb.

Manufacturers must regularly update portfolios to keep pace with shifting

demand for QLED, larger screens, AI-driven interfaces, and more advanced

connected experiences, which increases product development pressure and raises

the risk of inventory aging quickly.

For consumers, this pace of innovation can create

hesitation, since many buyers may postpone purchases in expectation of better

specifications, lower prices, or newer models arriving within a short period.

The result is a market where brands must innovate continuously while also

managing pricing, forecasting, and channel inventory carefully to avoid being

overtaken by the next feature cycle. This challenge is particularly sharp in

smart televisions, where hardware and software expectations now evolve together,

making product lifecycles feel shorter than in earlier television replacement

periods.

Key Market Trends

Premiumization and Advanced Display Technologies

Premiumization and advanced display technologies are becoming central to the India television market as consumers increasingly treat televisions as lifestyle-driven entertainment products rather than simple household appliances. This shift is visible in stronger interest toward QLED, Mini LED, and OLED models that offer better contrast, color depth, brightness control, and slimmer industrial design compared with conventional LED televisions. Buyers in urban and upper-middle-income segments are also showing greater willingness to pay for advanced picture performance because OTT viewing, sports streaming, and console gaming have made screen quality far more noticeable in daily use.

At the same time, manufacturers are widening premium portfolios and pushing more feature-rich televisions into broader price bands, which is helping premium technologies move beyond niche luxury positioning. As replacement cycles increasingly revolve around experience upgrades rather than basic ownership, the premium end of the market is likely to remain an important growth engine for brands competing in India. For Instance, Samsung said its television sales in India crossed ₹10,000 crore in 2024 and that category growth is being led by the premium segment, especially 55 inch and above screen sizes.

Larger Screens and Smart Connectivity

Larger screens and smart connectivity are advancing together in the India television market as households increasingly want immersive displays that can support streaming, live sports, gaming, and family co-viewing on a single device. The demand for bigger televisions is rising because screen upgrades now feel more meaningful when consumers spend longer hours watching OTT content, connected TV apps, and event-led programming at home. This trend is being reinforced by falling prices in 43-inch and 55-inch categories, which are making large-format televisions more attainable across upper-middle and aspirational urban households.

Smart connectivity adds another layer of appeal because consumers increasingly expect televisions to support app ecosystems, casting, voice features, and seamless integration with their internet-driven viewing behavior. As a result, screen-size expansion is no longer separate from connectivity adoption, since many buyers now evaluate televisions on both visual immersion and digital convenience at the same time.\

Rise of Regional Language Content

Rise of regional language content remains one of the strongest structural themes in the India television market because viewership patterns continue to reflect the country’s multilingual culture far more than a single-language national model. Regional programming has deep influence across both traditional broadcasting and OTT services, with viewers increasingly favoring content that reflects local identity, storytelling style, and cultural familiarity. This dynamic is especially important in southern markets, where Telugu, Tamil, and Kannada content holds substantial audience loyalty, while Marathi and Bangla channels also continue to build strong engagement.

Streaming platforms are responding by investing more heavily in localized originals and regional catalog expansion, which in turn supports television demand because smart TVs remain a preferred screen for long-form entertainment consumption at home. For television brands, this means product positioning cannot rely only on hardware features, since content relevance and language affinity continue to shape how households derive value from the screen itself. For Instance, BARC based data cited in the FICCI media report showed that Hindi accounted for 44% of television viewership in 2024, while Telugu held 12%, Tamil 11 %, Kannada 7%, Marathi 5%, and Bangla 4%.

OTT Coexistence and Shifting Viewership Habits

OTT coexistence and shifting viewership habits are redefining the India television market, but they are not eliminating the relevance of linear television as quickly as simple substitution narratives often suggest. Viewers are clearly adopting connected and app-based consumption for convenience, flexibility, and on-demand access, yet traditional television still retains strength in habitual entertainment, live sports, family viewing, and familiar long-running formats. This means the market is moving toward a coexistence model in which pay TV, free TV, and connected television serve different audience needs rather than a winner-takes-all format transition.

The continued growth of free TV and connected TV is cushioning the decline in traditional pay subscriptions, while television sets themselves remain the central screen through which many households experience both broadcast and streaming ecosystems.

Emerging Technologies: D2M and Gaming

Emerging technologies such as direct to mobile broadcasting and gaming-focused display features are adding a new innovation layer to the India television market by expanding how screens are used and what consumers expect from them. D2M is being explored as a broadcast-led distribution model that could deliver video content to mobile devices without requiring active internet access, which gives it potential relevance for rural connectivity, public service communication, and network offload. At the same time, television makers are increasingly building gaming-oriented features such as higher refresh rates, lower latency, motion enhancement, and responsive picture modes into more affordable models, widening the appeal of TVs among younger and digitally engaged buyers.

This matters because gaming no longer sits only in the premium niche, and feature convergence is gradually turning televisions into multi-purpose entertainment devices rather than passive streaming screens. As these technologies mature, they can create fresh upgrade triggers in a market where brands need new reasons for consumers to replace functioning televisions. For Instance, the government said D2M pilot projects were planned in 19 cities, while Xiaomi’s QLED TV X Pro series in India introduced a 120Hz Game Booster feature aimed at smoother gaming performance on mainstream television models.

Segmental Insights

Screen

Size Insights

In the India Television Market, the

50 inch-59 inch screen size segment has emerged as the dominant choice among

consumers. This segment appeals to a wide range of households seeking a balance

between screen size, viewing comfort, and affordability. Consumers are increasingly opting for larger

screen sizes within this range to enjoy an immersive viewing experience for

movies, sports, and gaming. The 50 inch-59 inch category strikes a balance between

providing a cinematic feel while still being practical for most living room

sizes in urban and suburban homes across India.

Manufacturers have responded by offering

a diverse array of models in this segment, incorporating advanced technologies

such as 4K Ultra HD resolution, HDR (high dynamic range), and smart TV

capabilities. These features enhance the viewing experience by delivering

vibrant colors, sharp details, and seamless access to streaming content and

applications. Additionally, competitive pricing strategies and promotional

offers from leading brands and retailers have contributed to the popularity of

the 50 inch-59 inch segment, making it a preferred choice for consumers looking to

upgrade their home entertainment setups without compromising on quality or

budget.

Distribution

Channel Insights

Supermarkets and hypermarkets have

emerged as the dominating distribution segment in the India television market.

These retail formats offer significant advantages such as wide product

selections, competitive pricing, and convenient shopping experiences,

attracting a large number of consumers looking to purchase televisions. One of

the key factors driving growth in supermarkets and hypermarkets is their

ability to showcase a diverse range of television brands and models under a

single roof. This allows consumers to compare features, screen sizes, prices,

and customer reviews before making a purchase decision. The availability of

knowledgeable staff and interactive displays further enhances the shopping

experience, helping consumers make informed choices based on their specific

preferences and requirements.

Moreover, supermarkets and hypermarkets

often run promotional campaigns, discounts, and bundled offers on televisions,

attracting price-sensitive consumers seeking value for money. These retail

formats also benefit from their strategic locations in urban and semi-urban

areas, catering to a wide demographic of consumers who prefer the convenience

of one-stop shopping for electronics. As consumer preferences evolve and demand

for televisions continues to grow, supermarkets and hypermarkets are poised to

play a pivotal role in shaping the distribution landscape of the Indian

television market, offering both accessibility and competitive pricing to meet

the diverse needs of consumers across the country.

Download Free Sample Report

Regional Insights

In the India Television Market, the

North region has emerged as the dominant and fastest-growing segment.

Comprising states such as Delhi, Uttar Pradesh, Rajasthan, Haryana, and Punjab, among others, the North region has seen robust growth in television sales, driven by

several factors.

One of the primary reasons for the North's dominance is its high population density and urbanization

rate. Metropolitan cities like Delhi and the NCR (National Capital Region) have a large concentration of affluent consumers with disposable income who are strongly inclined to purchase consumer electronics, including

televisions. The presence of a burgeoning middle class also significantly increases demand for televisions in urban and semi-urban areas

across the region. Furthermore, the North region benefits from extensive retail

infrastructure, including modern retail chains, electronics stores, and

hypermarkets that cater to diverse consumer preferences. These retail

outlets offer a wide range of television brands, sizes, and features, along with competitive pricing and promotional offers, attracting consumers

seeking value and quality.

Additionally, the North region

experiences a high demand for smart TVs and advanced technologies due to

increasing digital literacy and connectivity. Consumers in urban centers are

keen to access streaming services, online content, and interactive features on smart televisions, further driving growth in this segment in the

North Indian market. Overall, the North region's dominance in the India television market is underscored by its economic vibrancy, consumer preference for premium home entertainment, and robust retail infrastructure,

making it a pivotal growth driver in the national television industry.

Recent Developments

- In April 2025, Dish TV and C21Media advanced their collaboration through the inaugural Content India Summit 2025 in Mumbai, positioning it as a platform to connect India’s television and entertainment ecosystem with international content markets. The summit was designed to drive cross-border partnerships, expand market access, and encourage new approaches to content creation and distribution, which made it a notable collaboration-led development for India’s television industry rather than just a conference event. Its significance lay in giving Indian broadcasters, producers, and platform players a structured forum to build global relationships and prepare for a larger Content India 2026 rollout.

- In June 2025, Netflix entered a new creative partnership with Balaji Telefilms, one of India’s most influential television production houses, to develop content across multiple formats for streaming audiences. Variety reported that at least one series was already in advanced development, and the collaboration was to be executed through Balaji Telefilms and its subsidiaries, extending a relationship already tested through earlier joint projects. This was an important television-sector collaboration because it linked India’s legacy TV content engine with a global streaming platform, reflecting how television storytelling talent in India is being repurposed for hybrid broadcast-digital growth.

- In May 2025, Samsung launched its 2025 premium smart TV lineup in India, introducing Neo QLED 8K, Neo QLED 4K, OLED, QLED, and The Frame models with its new Vision AI platform. The company said the new televisions would offer AI-enhanced picture and sound, gesture control, a built-in SmartThings hub, and seven years of operating system upgrades, positioning the launch as both a product refresh and a technology upgrade. This counted as a breakthrough product development in India’s television market because it pushed AI from a marketing feature into the core viewing, personalization, and device-longevity proposition of premium TVs.

- In May 2026, Samsung rolled out its full 2026 Vision AI TV lineup in India, with 72 models across six categories and the debut of Micro RGB as a new premium television tier. According to Times of India, the Micro RGB range uses individually controlled red, green, and blue micro LEDs for finer light control, while the broader lineup spans OLED, Neo QLED, The Frame, Mini LED, and UHD sets sold through Samsung’s retail and partner channels in India. This stood out as a breakthrough innovation for the Indian television market because it marked the commercial introduction of a new display architecture alongside a wider AI-led portfolio expansion.

Key Market Players

- Samsung India Electronics Pvt Ltd.

- LG Electronics India Private Limited

- Xiaomi Technology India Private Limited

- Oneplus Technology India Private Limited

- Sony India Private Limited

- Hisense India Private Limited

- TCL-India Holdings Private Limited

- Intex Technologies (India) Limited

- Panasonic Life Solutions India Private

Limited

- Haier Appliances India Pvt Ltd

|

By Screen Size

|

By Display Type

|

By Distribution

Channel

|

By Region

|

- 39'' and Below

- 40''-49''

- 50''-59''

- Above 59''

|

|

- Multi-Branded Stores

- Supermarkets & Hypermarkets

- Online

- Exclusive Stores

- Others

|

|

Report Scope:

In this report, the India Television Market has

been segmented into the following categories, in addition to the industry

trends which have also been detailed below:

- India Television Market, By Screen

Size:

o 39'' and Below

o 40''-49''

o 50''-59''

o Above 59''

- India Television Market, By Display

Type:

o LED

o OLED

o Others

- India Television Market, By Distribution

Channel:

o Multi-Branded Stores

o Supermarkets & Hypermarkets

o Online

o Exclusive Stores

o Others

- India Television Market, By

Region:

o North

o South

o East

o West

Competitive Landscape

Company Profiles: Detailed analysis of the major companies presents

in the India Television Market.

Available Customizations:

India Television Market report with the given

market data, TechSci Research offers customizations according to a company's

specific needs. The following customization options are available for the

report:

Company Information

- Detailed analysis and

profiling of additional market players (up to five).

India Television

Market is an upcoming report to be released soon. If you wish an early delivery

of this report or want to confirm the date of release, please contact us at Distribution@techsciresearch.com