|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

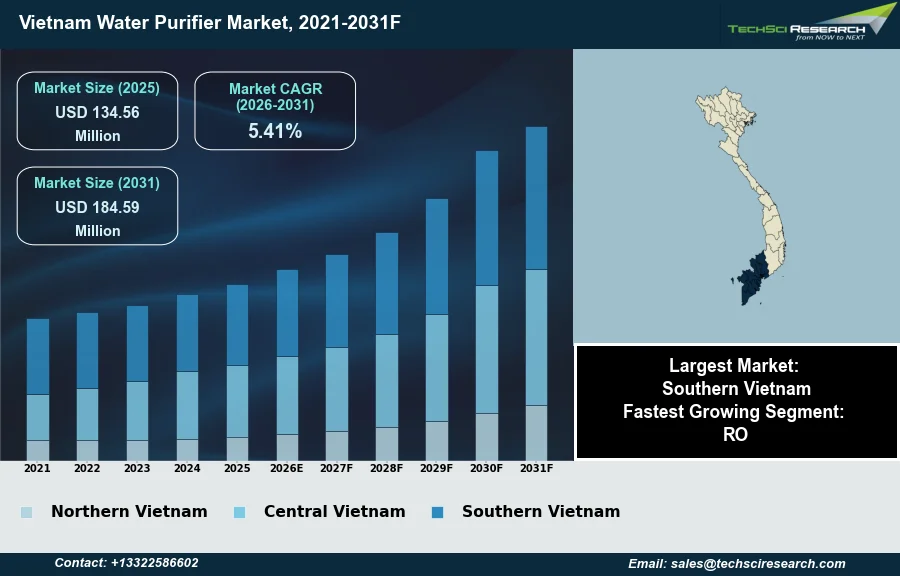

Market Size (2025)

|

USD 134.56 Million

|

|

CAGR (2026-2031)

|

5.41%

|

|

Fastest Growing Segment

|

RO

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 184.59 Million

|

Market Overview

The Water Purifier Market in Vietnam will grow from USD 134.56 Million in 2025 to USD 184.59 Million by 2031 at a 5.41% CAGR. A water purifier is an appliance engineered to remove undesirable chemicals, biological contaminants, suspended solids, and other impurities from water, rendering it safe for consumption and other applications through technologies such as reverse osmosis and ultraviolet treatment. The Vietnam Water Purifier Market is primarily driven by heightened public awareness concerning water quality and health implications, with studies indicating over 60% of Vietnamese households express concerns regarding tap water safety. Rapid urbanization and industrialization contribute significantly to water pollution, necessitating reliable purification solutions as municipal supplies face contamination challenges. Additionally, increasing disposable incomes empower consumers to invest in advanced purification systems.

However, a notable impediment to market expansion is the substantial initial capital outlay required for sophisticated water purification systems, which presents an affordability barrier, particularly for households outside affluent urban centers.

Key Market Drivers

Pollution Escalation and Stricter Regulations Drive Market Growth

Escalating water pollution and contamination stands as a primary catalyst for the Vietnam Water Purifier Market. Industrialization and rapid urbanization significantly strain existing water infrastructure, leading to widespread contamination of water sources. According to RTI International, in March 2026, a report revealed that 20% of household drinking water samples collected near Hanoi's industrial zones exceeded the American Academy of Pediatrics' recommended lead level, directly impacting consumer health and trust in tap water quality. Furthermore, insufficient wastewater treatment exacerbates the problem, with stricter regulations like QCVN 40:2025/BTNMT, effective September 1, 2025, now expanding controlled pollution parameters to 61, underscoring the severity and breadth of contaminants present in water sources across the country.

Health Awareness and Untreated Wastewater Drive In-Home Purification Demand

Concurrently, increasing health awareness and concerns regarding waterborne diseases are significantly propelling market expansion. Consumers are becoming more cognizant of the detrimental effects of contaminated water on health, driving demand for in-home purification systems. According to MDPI, in June 2025, a study highlighted that Arsenic concentrations frequently exceeded the World Health Organization guideline of 0.01 mg/L in surface water in the Mekong Delta, indicating chronic exposure hazards and fueling public demand for safe drinking solutions. This heightened awareness, coupled with the systemic challenges in water management, creates a compelling need for advanced purification technologies. The market's potential is further underscored by the fact that, according to the Vietnam Water Supply and Sewerage Association (VWSA), in December 2024, approximately 12 million cubic meters of wastewater are generated across the country daily, with up to 87% released untreated into the environment, emphasizing the critical role of water purifiers in mitigating widespread contamination.

Download Free Sample Report

Key Market Challenges

Upfront Costs Impede Market Expansion

A notable impediment to the expansion of the Vietnam Water Purifier Market is the significant initial capital outlay associated with advanced water purification systems. This financial requirement presents a substantial affordability barrier, particularly for households situated outside affluent urban centers. While consumer awareness regarding water quality and health implications is high, the upfront investment needed for effective purification solutions remains a key deterrent.

Income Levels Limit Market Penetration

This directly hampers market growth as a considerable segment of the population is unable to allocate funds for these purchases. According to the National Statistics Office, the average per capita income in Vietnam was estimated at VND 5.9 million (approximately $225) per month in 2025. This income level indicates that for a large portion of Vietnamese households, the cost of a modern water purifier represents a significant financial commitment, thereby limiting market penetration. The consequence is a restricted customer base, as the market struggles to reach households that prioritize immediate necessities over higher-priced home appliances, despite acknowledging the benefits of purified water.

Key Market Trends

Smart Technology Adoption Expands the Vietnam Water Purifier Market

The integration of smart technologies is increasingly influencing the Vietnam Water Purifier Market. These systems offer consumers enhanced convenience through features such as real-time water quality monitoring, automated filter replacement reminders, and remote control via mobile applications. This technological shift addresses consumer desire for ease of maintenance and assurance of water purity without constant manual checks. For instance, smart purifiers can provide alerts when water quality deviates from set parameters, prompting timely intervention. According to Vietnam Today, in February 2026, the household penetration of smart home devices in Vietnam was forecast to rise from approximately 15% in 2025 to roughly 25% within the next few years. This indicates a growing consumer readiness for connected appliances, including advanced water purification solutions.

Local Vietnamese Brands Drive Innovation and Market Leadership

Concurrently, local brands are demonstrating significant product innovation and establishing market leadership. These domestic manufacturers possess a deep understanding of local water conditions and consumer preferences, enabling them to tailor purification solutions effectively. Their agility in responding to specific market demands and investing in localized research and development has fostered strong consumer trust and brand loyalty. According to the Asia Pacific Enterprise Awards, SUNHOUSE Group, a prominent Vietnamese home appliance corporation, sells more than 30 million products domestically and exports over 13 million units each year, driven by its commitment to high-tech production lines and dedicated R&D. This highlights the considerable influence and production scale achieved by local players in shaping the market landscape.

Segmental Insights

RO Systems: Fastest-Growing Segment in Vietnam's Water Purifier Market

In the Vietnam Water Purifier Market, Reverse Osmosis (RO) systems represent a key segmental insight, emerging as the fastest-growing technology. This accelerated expansion is primarily driven by escalating concerns regarding water contamination stemming from rapid industrialization and urbanization, which have led to increased pollutants in water sources. Consumers are increasingly prioritizing health and seeking advanced purification solutions capable of effectively removing a broad spectrum of contaminants, including heavy metals, bacteria, and dissolved solids, capabilities for which RO technology is highly regarded. Furthermore, rising public awareness about waterborne diseases, coupled with government initiatives promoting improved water quality standards, significantly propels the adoption of RO purifiers across the nation.

Regional Insights

Southern Vietnam: Market Leader Fueled by Urbanization, Industrial Concentration, and Rising Affluence

Southern Vietnam emerges as the leading region in the Vietnam Water Purifier Market, primarily driven by rapid urbanization and significant industrial concentration in major cities such as Ho Chi Minh City. This concentration contributes to heightened water quality concerns from industrial discharge and agricultural runoff, prompting robust demand for purification solutions. Furthermore, the region benefits from higher disposable incomes and a growing middle class, enabling greater investment in advanced purification systems. Enhanced consumer awareness regarding waterborne diseases and health risks, further supported by the government's focus on public health, also fuels market expansion.

Recent Developments

-

In August 2025, Kangaroo continued its pioneering efforts in the Vietnamese water purifier market by advancing its Hydrogen Water technology. The company was noted for being the first in Vietnam to introduce active hydrogen alkaline water through its patented Reverse Osmosis Water Electrolysis Technology. Additionally, Kangaroo introduced water purifiers featuring magnet technology to produce hydrogen water with smaller molecular compounds, alongside advanced 10-stage filtration systems designed to deliver active hydrogen alkaline water and water-saving RO Vortex Purifier Technology.

-

In November 2024, A.O. Smith Corporation completed the acquisition of Pureit, a prominent water purification brand, from Hindustan Unilever Limited (HUL) for $72 million. This strategic acquisition significantly expanded A.O. Smith's presence in key emerging markets, including Vietnam. The transaction aimed to broaden A.O. Smith’s product portfolio and leverage Pureit’s established market position to cater to the growing consumer demand for safe and affordable water purification solutions in the Vietnamese market. This move consolidated capabilities in direct-to-consumer and e-commerce channels in the region.

-

In April 2024, Karofi, a leading water purifier brand in Vietnam, was recognized as one of the "TOP 10 ASEAN STRONG BRANDS 2024". This acknowledgment highlighted the company's continuous advancements and its leading position in applying modern 4.0 technology to water purifiers in the Vietnamese market. Such innovations included features like voice-activated water dispensing, remote water quality control via mobile applications, touchscreen interfaces, and advanced heating and cooling technologies, enhancing user convenience and product functionality.

-

In 2024, ITL Corporation, an integrated logistics solutions provider, demonstrated its commitment to social responsibility within Vietnam by donating water filtration systems to schools in Tien Giang. This initiative was part of the company’s broader efforts to contribute to community well-being and support educational institutions. By providing access to clean drinking water, ITL Corporation directly addressed a critical need, reflecting corporate engagement in the public health aspect related to water quality in the Vietnam Water Purifier Market.

Key Market Players

- Kent

- Eureka Forbes

- Pureit

- AO Smith

- Coway

- Blue Star

- Havells

- Local Purifier Brands

- Al Futtaim Water

- Amazon Vietnam Water

|

By Type

|

By Technology

|

By Sales Channel

|

By Region

|

- Floor Standing

- Under Sink

- Counter Top

- Faucet Mount

- Others

|

- RO

- UF

- UV

- Media

- Others (Nanofiltration, etc.)

|

- Retail

- Distributor

- Direct

- Online

- Others (Plumber, Contractor, etc.)

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam Water Purifier Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam Water Purifier Market, By Type:

-

Floor Standing

-

Under Sink

-

Counter Top

-

Faucet Mount

-

Others

-

Vietnam Water Purifier Market, By Technology:

-

RO

-

UF

-

UV

-

Media

-

Others (Nanofiltration, etc.)

-

Vietnam Water Purifier Market, By Sales Channel:

-

Retail

-

Distributor

-

Direct

-

Online

-

Others (Plumber, Contractor, etc.)

-

Vietnam Water Purifier Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam Water Purifier Market.

Available Customizations:

Vietnam Water Purifier Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam Water Purifier Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com