|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

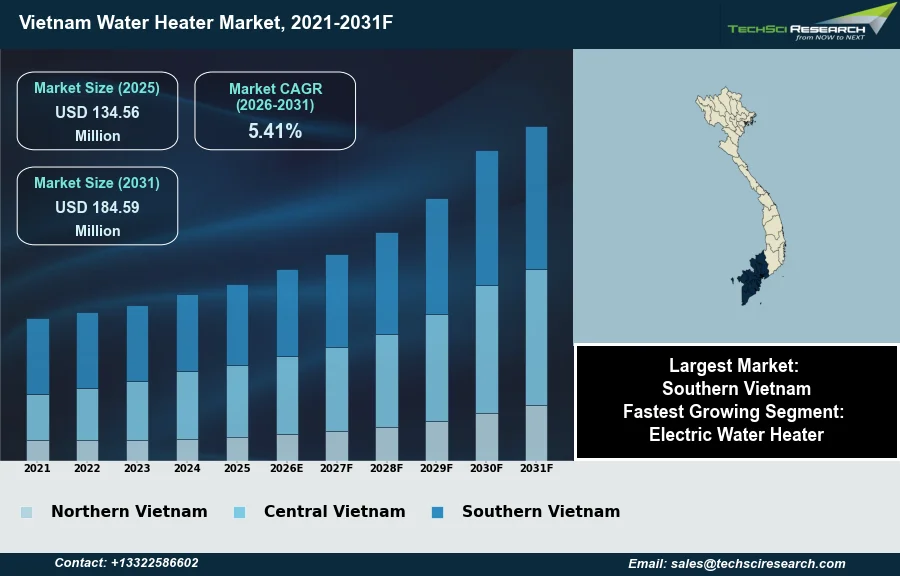

Market Size (2025)

|

USD 134.56 Million

|

|

CAGR (2026-2031)

|

5.41%

|

|

Fastest Growing Segment

|

Electric Water Heater

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 184.59 Million

|

Market Overview

The Water Heater Market in Vietnam will grow from USD 134.56 Million in 2025 to USD 184.59 Million by 2031 at a 5.41% CAGR. A water heater is an appliance designed to heat water beyond its ambient temperature for various domestic, commercial, or industrial applications. The Vietnam Water Heater Market is significantly driven by several key factors. These include sustained urbanization, leading to an expansion of modern housing units requiring hot water facilities, and consistent growth in disposable incomes among the populace, enabling higher investment in household comfort appliances. Furthermore, increasing awareness regarding improved hygiene standards and the government's initiatives for electrification contribute to market demand.

Despite these supportive drivers, the market faces challenges that could impede expansion. One significant impediment is the intense price competition within the sector, which can constrain profit margins for manufacturers and suppliers. This competitive landscape necessitates continuous innovation and efficiency improvements to maintain market positioning. While specific statistical data from industrial associations for the Vietnam water heater market for the last year, excluding market research reports, could not be identified through public search, the underlying economic conditions continue to shape market dynamics.

Key Market Drivers

Urbanization Drives Water Heater Demand

Rapid urbanization significantly drives the Vietnam Water Heater Market by increasing the number of households requiring modern conveniences. As populations migrate to urban centers, the demand for equipped residential units, including water heating systems, rises substantially. According to the General Statistics Office, in 2025, Vietnam's urban population was estimated to reach 39.4 million people, reflecting continuous demographic shifts. This concentrated growth fuels a consistent need for new infrastructure and household appliances, directly impacting water heater installations in both new and existing urban dwellings.

Construction Boom and Economic Growth Drive the Water Heater Market

Complementing urbanization, the booming real estate and construction sector serves as a direct catalyst for the water heater market. The development of new residential, commercial, and hospitality projects necessitates the integration of water heating solutions. According to the Ministry of Construction, in 2025, over 102,000 social housing units were completed nationwide, indicating a robust expansion in available living spaces. This construction activity creates immediate demand for a variety of water heater types. Furthermore, the strong economic environment, evidenced by Vietnam's GDP expanding by 7.83% year-on-year in the first quarter of 2026, according to the General Statistics Office, underpins consumer purchasing power and investor confidence in these development projects, thereby sustaining market growth.

Download Free Sample Report

Key Market Challenges

Affordability Constraints Hindering Adoption

A significant challenge for the Vietnam Water Heater Market is the prevailing price sensitivity among a substantial portion of the population, particularly in non-urban areas. This affordability constraint directly hampers market growth as consumers in lower-income segments often prioritize essential expenditures over high-cost home appliances. The initial investment required for a water heater, alongside potential installation and operational costs, presents a considerable barrier to adoption for many households.

Data Gaps Limiting Price-Sensitivity Metrics

Despite extensive efforts to locate specific statistical numerical data from a Vietnamese industrial association regarding the water heater market's valuation or sales directly linked to affordability for 2024 or 2025, such information is not publicly available through verified industrial association reports or official government statistics. Market data on the broader household appliance sector often originates from market research firms, which are explicitly excluded by the prompt's sourcing requirements. Therefore, the precise numerical impact of price sensitivity on water heater sales from an industrial association cannot be presented.

Key Market Trends

Policy incentives driving solar water heater adoption

The Vietnam Water Heater Market is significantly influenced by the growing adoption of renewable energy water heaters, particularly solar solutions. This trend is propelled by increasing environmental consciousness and governmental efforts to promote sustainable energy use in residential settings. For instance, according to PV Magazine, October 2025, in the 'Vietnam proposes financial support for residential solar, storage systems' article, the Ministry of Industry and Trade has proposed that households could receive up to VND 3 million in investment capital for home solar-plus-storage systems, demonstrating clear policy support for sustainable heating alternatives. This financial incentive encourages consumers to transition from traditional heating methods to more ecologically friendly options, directly impacting the demand for solar water heaters.

IoT-enabled water heaters aligned with digital transformation

Another pivotal trend is the accelerating integration of smart technology and IoT features into water heating solutions. Consumers increasingly seek convenience, remote control, and enhanced energy management capabilities in their home appliances. This push aligns with broader national digital transformation initiatives. According to the Ministry of Industry and Trade, December 2025, at the 'Digital Transformation Forum 2025', the year 2026 is planned for the nationwide rollout of smart energy measurement and management, reflecting a strategic emphasis on intelligent utility systems that complement smart home appliances, including advanced water heaters. This focus on connected ecosystems drives innovation in water heater functionalities, offering users greater control and efficiency.

Segmental Insights

Electric Water Heaters: Fastest-Growing Segment in Vietnam

The Vietnam Water Heater Market is experiencing significant growth, with the Electric Water Heater segment emerging as the fastest-growing. This rapid expansion is primarily driven by increasing urbanization and rising disposable incomes, enabling Vietnamese consumers to invest in modern home appliances. Electric water heaters are highly favored due to their affordability, ease of installation, and seamless compatibility with the nation's developing electricity infrastructure. Furthermore, the booming real estate sector, particularly new residential and commercial constructions, consistently integrates these efficient and convenient heating solutions, aligning with consumer preferences for comfort and contemporary living standards.

Regional Insights

Southern Vietnam: Market Leader Driven by Urbanization and Solar Potential

Southern Vietnam emerges as a pivotal region within the Vietnam Water Heater Market, largely attributed to its status as the country's most vibrant economic hub, encompassing major urban centers such as Ho Chi Minh City. This region experiences significant urbanization and a steady increase in disposable incomes, fostering a higher consumer acceptance rate for modern water heating solutions in both residential and commercial applications. The substantial development in infrastructure, coupled with a burgeoning hospitality sector and numerous residential complexes, consistently drives demand for efficient water heating systems. Furthermore, Southern Vietnam's abundant sunshine makes it particularly conducive for the adoption of solar water heaters, contributing to its market leadership.

Recent Developments

-

In July 2024, Ariston, a major water heater manufacturer, highlighted Vietnam's significance as a key production hub. The company's leadership discussed their strategic commitment to launching new water heater products in the country, incorporating pioneering, energy-efficient, and environmentally friendly technologies. Furthermore, Ariston expressed intentions to pursue extensive projects and establish collaborations with various construction and development partners across Vietnam, aiming to provide a comprehensive array of heating solutions for diverse sectors.

-

In February 2024, Ariston, a prominent thermal comfort brand, reiterated its commitment to sustained investment in Vietnam. The company emphasized its ongoing plans to expand its workforce and strengthen its production facilities within the nation. This strategic focus was driven by a rising demand for sustainable products, indicating a notable shift towards green consumption trends among Vietnamese consumers and industry partners. Ariston affirmed its dedication to elevating local consumers' comfort through eco-friendly products, aligning with its mission for sustainable comfort.

-

In 2025, Ariston was recognized at the "Energy Efficiency Awards," receiving an accolade for its "Smart Energy-Saving Hot Water Solutions." This honor underscored the company's leadership in Vietnam's heating sector. During this period, Ariston also introduced its latest generation of indirect water heaters, the Slim3 series. These new products featured advanced smart technologies and an Italian-inspired design, developed to deliver enhanced efficiency and cater to evolving user demands within the Vietnamese market.

-

In 2025, Bosch Vietnam achieved stable business growth across its key operational areas, including home appliances. The company concurrently increased its investments in local manufacturing and research and development initiatives. This strategic expansion aimed to strengthen Vietnam's role within Bosch's global service network, fostering the country's emergence as a regional service hub for logistics, supply chain operations, and comprehensive after-sales support. The focus on R&D and manufacturing capacity is expected to impact product offerings, including water heaters.

Key Market Players

- Ariston Thermo Vietnam

- Rheem Manufacturing

- Ferroli Vietnam

- Panasonic Vietnam

- Electrolux Vietnam

- Midea Vietnam

- Centon Vietnam

- Kangaroo Group

- Sunhouse Group

- Picenza Vietnam

|

By Product Type

|

By Application

|

By Region

|

- Electric Water Heater

- Gas Water Heater

- Solar Water Heater

- Heat Pump Water Heater

|

- Residential

- Commercial/Industrial

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam Water Heater Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam Water Heater Market, By Product Type:

-

Electric Water Heater

-

Gas Water Heater

-

Solar Water Heater

-

Heat Pump Water Heater

-

Vietnam Water Heater Market, By Application:

-

Residential

-

Commercial/Industrial

-

Vietnam Water Heater Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam Water Heater Market.

Available Customizations:

Vietnam Water Heater Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam Water Heater Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com