|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

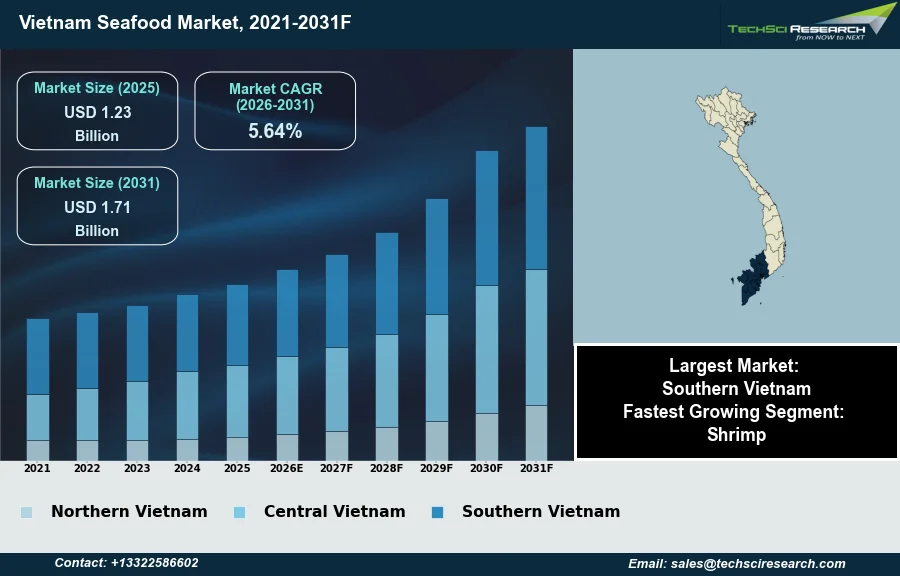

Market Size (2025)

|

USD 1.23 Billion

|

|

CAGR (2026-2031)

|

5.64%

|

|

Fastest Growing Segment

|

Shrimp

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 1.71 Billion

|

Market Overview

The Seafood Market in Vietnam will grow from USD 1.23 Billion in 2025 to USD 1.71 Billion by 2031 at a 5.64% CAGR. The Vietnam seafood market encompasses a diverse array of cultivated and wild-caught aquatic products, including prominent species such as shrimp, pangasius, and various marine fish, processed for both domestic consumption and international export. The market's growth is primarily driven by Vietnam's extensive coastline, robust government support for aquaculture development, increasing global demand for protein, and strategic utilization of free trade agreements facilitating market access. According to the Vietnam Association of Seafood Exporters and Producers (VASEP), in 2025, the country's seafood export turnover reached approximately USD 11.3 billion, marking an increase of over 12% compared to 2024.

Despite this strong performance, a significant challenge impeding sustained market expansion is the unresolved Illegal, Unreported, and Unregulated (IUU) fishing "yellow card" issued by the European Union. This regulatory impediment restricts access to a key export market and mandates adherence to stringent traceability and sustainability standards, impacting the wild-caught seafood segment and requiring substantial industry adjustments.

Key Market Drivers

Robust global demand drives Vietnam's seafood market

Robust global export demand significantly propels the Vietnam seafood market, driven by increasing international appreciation for Vietnamese aquatic products and rising protein consumption worldwide. This sustained appetite from key markets such as China, the US, and Japan provides consistent impetus for production and processing activities within Vietnam. According to Vietnam News, citing the Vietnam Association of Seafood Exporters and Producers (VASEP), seafood export turnover reached nearly $4 billion in the first four months of 2026, reflecting a robust increase of more than 14 percent year-on-year. This performance highlights the market's ability to meet diverse global needs despite various international trade complexities.

FTAs expand access and diversify Vietnam's seafood exports

Strategic free trade agreements (FTAs) further enhance Vietnam's seafood market by expanding access and offering competitive tariff advantages. Agreements like the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and the EU-Vietnam Free Trade Agreement (EVFTA) dismantle trade barriers, making Vietnamese seafood more attractive to importing nations. Seafood exports to CPTPP member countries reached $3.07 billion in 2025, up 22% compared to the previous year, according to VnEconomy, citing VASEP. Furthermore, under the EVFTA, Vietnam's shrimp export value to the EU reached 434 million USD in the first nine months of 2025, marking a 21% year-on-year increase, according to Nhan Dan Online, attributing VASEP. These agreements are instrumental in facilitating market diversification and integrating Vietnam into global seafood supply chains.

Download Free Sample Report

Key Market Challenges

EU IUU Yellow Card: Implications for Vietnam's Seafood Exports

A significant challenge impeding the sustained expansion of the Vietnam seafood market is the unresolved Illegal, Unreported, and Unregulated (IUU) fishing "yellow card" issued by the European Union. This regulatory impediment directly restricts access to a crucial export market, increasing operational costs for enterprises and diminishing the overall competitiveness of Vietnamese seafood products globally. The yellow card status necessitates rigorous adherence to stringent traceability and sustainability standards, primarily impacting the wild-caught seafood segment and requiring substantial industry adjustments.

EU IUU Measures: Non-Tariff Barrier and Reputation Risk

The EU's ongoing yellow card serves as a considerable non-tariff barrier, creating additional burdens for Vietnamese exporters. According to the Vietnam Association of Seafood Exporters and Producers (VASEP), tuna exports fell 6.5 percent to USD 924.3 million in 2025, largely attributed to significant headwinds from the EU's IUU fishing warning and raw material shortages. This regulatory constraint not only complicates export processes but also damages the international reputation and credibility of Vietnamese seafood, which can have long-term implications for market growth beyond the EU.

Key Market Trends

Tech-Driven Aquaculture Modernization and Public Investment

High-tech aquaculture adoption represents a pivotal trend for the Vietnam seafood market, driving enhanced productivity, improved disease management, and a reduced environmental footprint. This strategic shift involves integrating advanced technologies such as real-time water quality monitoring, automated feeding systems, and biofloc technology in farming operations. These innovations are crucial for sustaining growth in a sector facing increasing resource constraints and environmental scrutiny. The government is actively supporting this transformation, allocating nearly $300 million to upgrade over 50 farming zones, as reported by SGS Digicomply in May 2025 in "Vietnamese Aquaculture in 2025: Market Trends and Potential". This investment underscores a national commitment to modernizing production methods and increasing efficiency across the aquaculture value chain.

Rise of Value-Added Seafood and Premium Exports

Another significant trend is the robust development of value-added seafood products, moving beyond raw material exports to offer sophisticated processed goods that command higher prices in international markets. This shift enables Vietnamese producers to differentiate their offerings, cater to evolving consumer preferences for convenience and quality, and enhance overall profitability. This strategy is evident in the strong performance of premium segments; for instance, lobster exports surged to US$817 million in 2025, more than doubling 2024 levels, according to Vietnam Briefing in January 2026, in "Vietnam's Seafood Exports: Growth Drivers, Market Shifts, and Outlook". This focus on higher-value products is essential for increasing export revenue and strengthening Vietnam's position in competitive global seafood markets.

Segmental Insights

Policy Support, Trade Access, and Sustainability Propel Shrimp Growth in Vietnam

Shrimp is the fastest-growing segment within the Vietnam Seafood Market, largely propelled by robust global demand for high-quality and sustainably sourced products. This rapid expansion is underpinned by the Vietnamese government's strategic focus, with institutions like the Ministry of Agriculture and Rural Development actively promoting sustainable aquaculture practices and supporting the adoption of advanced farming technologies. Furthermore, Vietnam's participation in key international trade agreements, such as the EVFTA and CPTPP, significantly enhances market access and boosts competitiveness in major export destinations including the United States, EU, and Japan. This concerted effort towards quality, sustainability, and market reach collectively fuels the segment's strong growth trajectory.

Regional Insights

Southern Vietnam's geographic advantages and policy support drive its seafood leadership.

Southern Vietnam dominates the Vietnam Seafood Market primarily due to its exceptional geographical advantages, notably the Mekong Delta's extensive river systems and favorable climate that are ideal for aquaculture. This region is the hub for cultivating key export species such as pangasius and shrimp, accounting for a substantial majority of the national aquaculture output and serving as the primary source of raw materials for processing. Furthermore, Southern Vietnam benefits from developed infrastructure, a high concentration of seafood processing facilities, and the continuous adoption of advanced farming technologies. The Ministry of Agriculture and Rural Development, through bodies like the Directorate of Fisheries and the National Agro-Forestry-Fisheries Quality Assurance Department, supports adherence to international quality and sustainability standards, reinforcing the region's leading position.

Recent Developments

-

In December 2025, De Heus Company Limited and Minh Phu Seafood Group Joint Stock Company, a prominent Vietnamese shrimp processing and exporting enterprise, formalized a strategic cooperation agreement. This partnership in Vietnam's seafood market aimed to foster the sustainable development of the country's shrimp value chain. De Heus committed to supplying advanced nutritional solutions, high-quality aquafeed, and technical support services to Minh Phu. In return, Minh Phu agreed to utilize De Heus's shrimp feed products across its farming operations. The collaboration further involved pilot programs, technology transfer, and initiatives to elevate the value of Vietnamese shrimp internationally.

-

In September 2024, Vinh Hoan Corporation, based in Cao Lanh, Vietnam, received the Best New Product award at the 2024 Seafood Excellence Asia Awards for its "Lucky Bag" retail product. This innovative offering for the Vietnamese seafood market is a combination of pangasius surimi, shrimp, and various vegetables including corn, carrots, and green onions. The pangasius surimi was ingeniously used for the dumpling wrappers, while vibrant colors were achieved through natural ingredients like pumpkin, butterfly pea flower, and spirulina. The product was recognized for its delicious, nutritious, and aesthetically pleasing attributes, requiring minimal cooking time.

-

In August 2024, Minh Phu Seafood Corporation, a Vietnamese company, launched a new premium shrimp product under its "Rice Shrimp 5 in 1" brand. The "Premium HLSO" (Head Less Shell On) shrimp were cultivated using an innovative rice-shrimp farming model, which integrates rice cultivation and shrimp farming on the same land. This sustainable approach aims to maximize land use while promoting environmental responsibility. The company emphasized the product's superior quality and flavor, attributed to natural farming methods, live harvesting, and rapid processing techniques. This launch was positioned to redefine sustainable seafood expectations in the market.

-

In February 2024, Vinh Hoan Corporation, a leading Vietnamese sustainable seafood producer, expanded its strategic partnership with Entobel, an insect protein producer. This collaboration aimed to advance a more sustainable and resilient aquaculture supply chain within the Vietnamese seafood market. The partnership included an off-take agreement where Feed One, a subsidiary of Vinh Hoan, committed to purchasing a substantial volume of insect protein from Entobel’s Vung Tau factory in 2024. Over the next three years, from 2025 to 2027, Vinh Hoan will purchase a minimum of 15,000 metric tons of insect protein to integrate into pangasius production.

Key Market Players

- Saudi Fisheries Company

- National Fishing Company

- Almarai Seafood

- Al Rabie Seafood

- Al Othaim Seafood

- Lulu Seafood

- HyperPanda Seafood

- Carrefour Seafood

- Bin Dawood Seafood

- Amazon Vietnam Seafood

|

By Product Type

|

By Type

|

By Distribution Channel

|

By Region

|

- Fishes

- Shrimps

- Oysters

- Snails

- Others

|

|

- Supermarket/Hypermarket

- Traditional Retails

- Online

- Others

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam Seafood Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam Seafood Market, By Product Type:

-

Fishes

-

Shrimps

-

Oysters

-

Snails

-

Others

-

Vietnam Seafood Market, By Type:

-

Vietnam Seafood Market, By Distribution Channel:

-

Supermarket/Hypermarket

-

Traditional Retails

-

Online

-

Others

-

Vietnam Seafood Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam Seafood Market.

Available Customizations:

Vietnam Seafood Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam Seafood Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com