|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

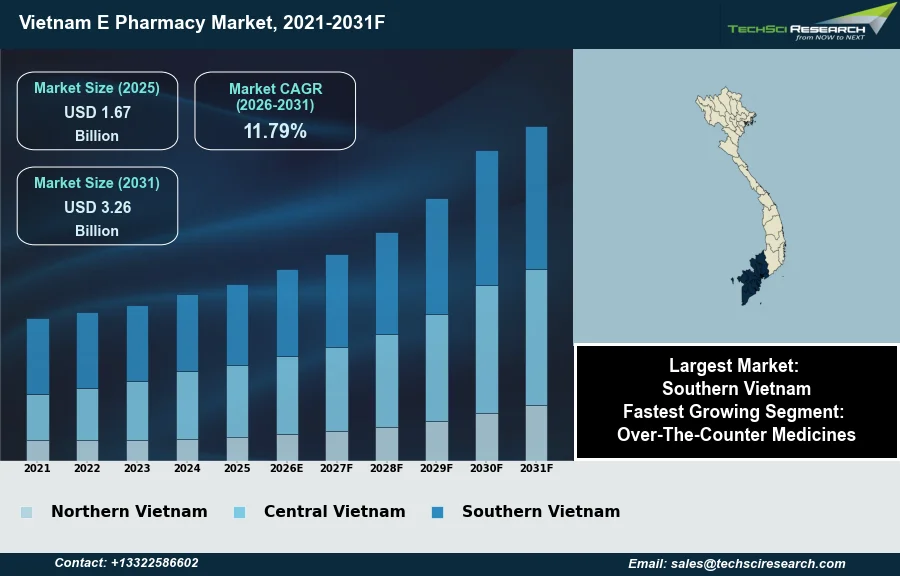

Market Size (2025)

|

USD 1.67 Billion

|

|

CAGR (2026-2031)

|

11.79%

|

|

Fastest Growing Segment

|

Over-The-Counter Medicines

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 3.26 Billion

|

Market Overview

The E-Pharmacy Market in Vietnam will grow from USD 1.67 Billion in 2025 to USD 3.26 Billion by 2031 at a 11.79% CAGR. E-pharmacy encompasses the online retail and distribution of pharmaceutical products, alongside digital healthcare services, offering consumers remote access to medications and professional consultations. The market's growth is primarily driven by escalating digital adoption rates and increasing demand for convenient healthcare solutions. According to the Drug Administration of Vietnam, in 2025, the online public service system for the pharmaceutical and cosmetic sectors processed nearly 110,000 online applications, indicating a substantial increase in digital engagement within the industry. Further impetus comes from governmental initiatives promoting healthcare digitalization and expanding internet penetration across the nation.

Despite robust growth drivers, a significant challenge impeding market expansion stems from the intricate regulatory environment governing online prescription drug sales. Current frameworks often present complexities regarding verification processes for online prescriptions and ensuring the authenticity and quality of pharmaceutical products dispensed digitally, thereby necessitating continuous adaptation by market participants.

Key Market Drivers

Digital Connectivity Fuels E-Pharmacy Growth in Vietnam

Rapid digitalization and increasing internet penetration profoundly influence the Vietnam E Pharmacy Market by expanding the addressable consumer base and enabling seamless online transactions. Widespread availability of affordable smartphones and improved network infrastructure has empowered a larger segment of the population to access digital services, including online healthcare platforms. This digital shift facilitates consumer engagement with e-pharmacy, from browsing products to placing orders and managing prescriptions. According to DataReportal's "Digital 2026: Vietnam" report, in October 2025, Vietnam recorded 85.6 million internet users, reflecting an online penetration of 84.2 percent. This extensive digital connectivity forms a foundational layer for e-pharmacy growth, making online medication procurement a viable and increasingly preferred option for a digitally-savvy populace.

Health Awareness and Digital Health Adoption Drive Online Pharmacy Expansion

Concurrently, rising health awareness and a growing demand for convenient healthcare access are pivotal drivers. Consumers are increasingly proactive about managing their health and seeking accessible solutions that integrate into their busy lifestyles, fueling online pharmacy adoption. The convenience of e-pharmacy, such as home delivery and 24/7 access to products, caters to this evolving preference. According to Vietnam News, in March 2026, electronic health records linked to the VNeID application had been deployed across 34 provinces and cities, encompassing approximately 30 million digital health records. This widespread digital health adoption underscores public readiness to engage with online health platforms. Further supporting e-pharmacy's ecosystem, according to Vietnam News, in March 2026, over 1,200 public and private hospitals nationwide had implemented electronic medical records. These interconnected developments collectively enhance operational environments, fostering market expansion.

Download Free Sample Report

Key Market Challenges

Regulatory Constraints on Online Prescription Drug Sales

The intricate regulatory environment in Vietnam directly impedes the growth of the e-pharmacy market, particularly concerning the online sale of prescription drugs. A significant development in this area is the amended Pharmacy Law, which came into effect on July 1, 2025, explicitly prohibiting the retail sale of prescription drugs through e-commerce platforms, with limited exceptions. This regulatory measure restricts e-pharmacies from offering a wide range of essential medications, thereby limiting their potential market scope and revenue generation. The inability to digitally process and dispense prescription medications fundamentally alters the business model for online pharmacies, shifting their focus primarily to over-the-counter products.

Barriers to Digital Distribution and Compliance Burden

This prohibition creates substantial barriers for market participants aiming to leverage digital channels for comprehensive pharmaceutical distribution. It forces e-pharmacy operators to continuously adapt their strategies to a more constrained operational environment. While the broader pharmaceutical market in Vietnam saw a total value of 234.8 trillion VND in 2025, a 5% increase from 2024, according to the Vietnam Pharmaceutical Corporation (Vinapharm), the e-pharmacy segment's growth potential is directly hampered by such specific legislative restrictions on product categories. The legal framework's complexity, coupled with the need for stringent verification processes for any permissible online drug sales and ensuring product authenticity, necessitates considerable compliance efforts that detract from market expansion.

Key Market Trends

Expansion of OTC and Wellness Offerings in Vietnam E Pharmacy Market

The expansion of over-the-counter and wellness product offerings represents a pivotal trend reshaping the Vietnam E Pharmacy Market, driven by evolving consumer preferences for proactive health management and strategic diversification. Faced with regulatory constraints on online prescription drug sales, e-pharmacies are increasingly focusing on non-prescription medications, dietary supplements, and personal care items. This shift enables platforms to diversify revenue streams and cater to a broader spectrum of consumer health needs. According to Theinvestor.vn, in March 2026, retail sales in Vietnam's beauty and personal care category reached VND74.4 trillion ($2.83 billion) in 2025, marking a nearly 30% year-on-year increase and becoming the largest segment in the nation's online retail market. This growth highlights the strong demand for products enhancing general well-being.

Telemedicine Integration with E-Pharmacy Platforms

Another significant trend is the increasing integration of telemedicine with e-pharmacy platforms, fostering a more holistic digital healthcare ecosystem. This convergence offers consumers convenient access to remote medical consultations alongside medication procurement, streamlining the patient journey from diagnosis to treatment. Such integration enhances patient engagement and trust by providing professional medical advice directly within the e-pharmacy framework, especially valuable where healthcare access may be uneven. This trend is bolstered by broader digital health adoption. According to the Vietnam Medical Informatics Association, as reported on June 21, 2026, 1,238 hospitals across Vietnam have commenced applying artificial intelligence and digital technologies in healthcare services, establishing a foundational infrastructure for integrated digital health offerings.

Segmental Insights

OTC Medicines: Key Growth Driver in Vietnam's E-Pharmacy Market

The Over-The-Counter (OTC) Medicines segment is a primary growth driver within the Vietnam E-Pharmacy Market, experiencing rapid expansion due to evolving consumer preferences and a conducive regulatory framework. This segment's swift growth stems from increasing health awareness and a rising inclination towards self-medication for common ailments, enabling consumers to conveniently purchase products such as vitamins, health supplements, and minor remedies without requiring a prescription. Regulatory clarity from the Ministry of Health, which permits the online sale of OTC medications, significantly reduces market entry barriers compared to prescription drugs. This policy, coupled with extensive internet penetration, facilitates seamless online transactions, cementing OTC medicines' position as a key growth catalyst in Vietnam's digital pharmaceutical landscape.

Regional Insights

Key Drivers of Southern Vietnam's E-Pharmacy Market

Southern Vietnam stands as the leading region in Vietnam's e-pharmacy market, primarily driven by its significant population density and rapid urbanization, particularly in major economic and healthcare hubs like Ho Chi Minh City. This dominance is further propelled by the region's robust digital infrastructure, characterized by high internet penetration and widespread smartphone adoption, which fosters consumer receptiveness to online health solutions. A growing middle-class population, coupled with increased health awareness and busy lifestyles, fuels the demand for convenient digital access to medicines. The presence of established pharmaceutical distributors, advanced logistics networks, and leading healthcare facilities further supports the efficient growth and operation of e-pharmacy services in Southern Vietnam. The Ministry of Health also plays a crucial role in regulating this evolving market by mandating licenses and operational standards for online pharmacies.

Recent Developments

-

In December 2025, Pharmacity, a leading drugstore chain in Vietnam, entered into a strategic partnership with Biocodex Vietnam, a French pharmaceutical group. The agreement, signed in Ho Chi Minh City, aimed to enhance the distribution of Biocodex's health products throughout Vietnam. This collaboration signified a concerted effort to expand the availability of internationally standardized, EU-standard healthcare solutions to Vietnamese consumers through Pharmacity's extensive retail network, including its digital channels. The partnership reinforced Pharmacity's commitment to offering a diverse portfolio of high-quality, scientifically-backed products within the Vietnam E Pharmacy Market.

-

In August 2025, Pharmacity established a strategic partnership with Nestlé Health Science, the specialized health and nutrition division of Nestlé Group. This collaboration focused on increasing the accessibility of internationally standardized, science-based nutrition products in Vietnam. Pharmacity became a key distribution partner for a range of imported nutritional solutions, including products for children, older adults, and individuals with digestive impairments, as well as exclusive rights for Vital Proteins Collagen Peptides. This initiative aimed to broaden consumer access to premium health products and promote proactive health management within the Vietnam E Pharmacy Market.

-

In December 2024, FPT Long Chau, a prominent pharmacy chain in Vietnam, partnered with the Centre for Research and Application of Population Data and Citizen Identification (RAR Center) under the Ministry of Public Security. This collaboration led to the introduction of an electronic verification service via the VNeID application. Commencing January 1, 2025, customers gained the ability to securely purchase medications online through the VNeID platform, thereby enhancing the trustworthiness of digital healthcare transactions within the Vietnam E Pharmacy Market. This initiative aimed to improve accessibility and ensure greater transparency and privacy for consumers engaging in online pharmaceutical purchases.

-

In November 2024, SwiftHub announced a significant investment of $5 million for Vietnam's first pharmaceutical-grade e-commerce fulfillment center in Ho Chi Minh City. This development responded to the Vietnamese government's policy, enacted in July 2024, which officially permitted the online sale of over-the-counter (OTC) medications. The 1.3-hectare facility was designed to meet stringent Good Storage Practice (GSP) standards, including temperature-controlled zones, to ensure the integrity and safety of products. This investment was poised to redefine healthcare logistics and establish new benchmarks for efficiency in the rapidly expanding Vietnam E Pharmacy Market.

Key Market Players

- Pharmacity

- FPT Long Châu

- An Khang Pharmacy

- Medigo

- Med247

- Jio Health

- Buymed (Thuocsi.vn)

- mClinica Vietnam

- MyPharma

- Vietnam DrugBank

|

By Type

|

By Operating Platform

|

By Region

|

- Prescription Medicines

- Over-The-Counter Medicines

|

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam E Pharmacy Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam E Pharmacy Market, By Type:

-

Prescription Medicines

-

Over-The-Counter Medicines

-

Vietnam E Pharmacy Market, By Operating Platform:

-

Vietnam E Pharmacy Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam E Pharmacy Market.

Available Customizations:

Vietnam E Pharmacy Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam E Pharmacy Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com