|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

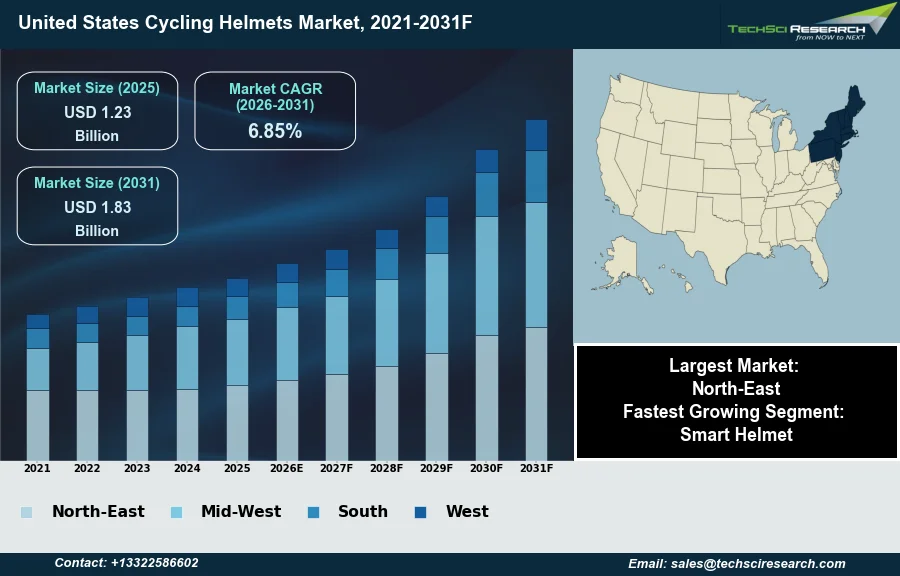

Market Size (2025)

|

USD 1.23 Billion

|

|

CAGR (2026-2031)

|

6.85%

|

|

Fastest Growing Segment

|

Smart Helmet

|

|

Largest Market

|

North-East

|

|

Market Size (2031)

|

USD 1.83 Billion

|

Market Overview

The United States Cycling Helmets Market will grow from USD 1.23 Billion in 2025 to USD 1.83 Billion by 2031 at a 6.85% CAGR. The United States cycling helmets market encompasses protective headgear designed to mitigate head injuries sustained during various cycling activities. This market's expansion is significantly propelled by several key drivers. Primarily, increasing public awareness regarding cycling safety and the importance of head protection, alongside governmental regulations mandating helmet usage in various jurisdictions, fosters consistent demand. Furthermore, a growing engagement in cycling for health, leisure, and as a sustainable mode of urban transportation directly contributes to market growth.

According to PeopleForBikes, in 2024, 112 million Americans rode a bicycle at least once, underscoring a substantial and expanding participant base requiring protective equipment. This robust participation, coupled with ongoing investments in dedicated cycling infrastructure, supports sustained market vitality. However, a significant challenge impeding market expansion is the proliferation of counterfeit products, which compromises user safety by failing to meet established protective standards and erodes consumer confidence in legitimate safety certifications.

Key Market Drivers

Rising Cycling Participation Expands Helmet Demand

Expanding cycling participation and the enthusiast base represent a primary driver for the United States cycling helmets market. As more individuals embrace cycling for recreation, fitness, and commuting, the demand for protective headgear naturally escalates. This growing engagement is evident across various segments of the population; according to Eco-Counter, in 2025, cycling traffic in the US grew by 4.7%, indicating a notable increase in overall ridership. This sustained growth introduces new cyclists requiring entry-level helmets and encourages existing enthusiasts to upgrade their equipment for enhanced performance and safety. The diversification of cycling demographics further broadens the consumer base for different helmet types.

Technological Innovation Accelerates Helmet Growth

Continuous technological innovation in helmet design also significantly propels the market. Manufacturers are consistently introducing advanced features that improve protection, comfort, and aerodynamics. Innovations such as multi-directional impact protection systems (MIPS) and other rotational impact technologies are increasingly standard in premium offerings. For instance, manufacturers have incorporated advanced safety systems into 45.3% of premium helmet SKUs by 2026, showcasing the industry's commitment to enhanced safety. These advancements attract tech-savvy buyers and incentivize existing cyclists to replace older models. The broader cycling market’s vitality further supports this trend; according to the National Bicycle Dealers Association's 2026 Market Outlook, published in January 2026, U.S. bicycle retail sales are projected to reach USD 4.1 billion in 2026, reflecting robust consumer spending within the sector. This environment sustains investment in helmet design and safety technologies.

Download Free Sample Report

Key Market Challenges

Counterfeit Helmets Undermine Safety Standards and Market Growth

The proliferation of counterfeit products presents a significant impediment to the growth of the United States cycling helmets market. These illicit goods frequently bypass rigorous testing and established safety certifications, directly compromising user safety by failing to provide the expected level of head injury mitigation. The presence of substandard, uncertified helmets erodes consumer confidence, not only in individual brands but also in the integrity of legitimate safety standards that are crucial for protective gear. This directly undermines the market for authentic manufacturers who invest substantially in research, development, and stringent quality control measures.

Revenue Loss and Market Dilution from Counterfeits

Such market distortion leads to a tangible loss of sales for legitimate products, as consumers may inadvertently purchase inferior alternatives or become hesitant to trust safety claims across the market. The Sports & Fitness Industry Association (SFIA) reported that the wholesale sales for the overall U.S. sporting goods industry reached $130 billion in 2025, indicating the substantial size of the legitimate market susceptible to the damaging effects of counterfeit goods. This pervasive issue ultimately hampers the sustained expansion of the market for certified cycling helmets by diverting revenue and diminishing the value of genuine, safety-compliant products.

Key Market Trends

Integrated Smart Helmets Drive Premium Segment Growth

The integration of smart helmet technology represents a pivotal trend reshaping the United States cycling helmets market. This involves incorporating advanced electronics such as integrated lighting systems, GPS navigation, and communication capabilities directly into helmets, moving beyond traditional passive protection. These features offer cyclists enhanced situational awareness and connectivity, appealing to urban commuters and tech-savvy recreational riders seeking comprehensive safety solutions and a seamless riding experience. This focus on integrated technology differentiates these products significantly from conventional helmets, driving a new segment of premium offerings. For instance, the Lumos Sonorus smart helmet successfully raised over £350,000 (approximately $440,000 USD) on Kickstarter with more than 1,600 backers, demonstrating strong consumer interest in these advanced functionalities, according to Road.cc, May 23, 2026, in 'Lumos adds talking to do-it-all helmet + loads more tech'.

E-Bike-Specific Helmets for Higher Speeds and Comfort

Another significant trend influencing the market is the specialized development of helmets for e-bike users. The growing popularity of electric bicycles, which typically reach higher average speeds and are often used for longer distances, necessitates helmets engineered with distinct safety and comfort considerations. Manufacturers are responding by designing helmets with improved ventilation to manage increased exertion, enhanced impact protection tailored to higher velocities, and sometimes integrated visors for better wind and debris protection. This trend reflects a market adaptation to the unique demands of the rapidly expanding e-bike segment, creating a dedicated category of helmets that cater specifically to the performance and safety requirements of electric cycling. According to BenitoLink, June 30, 2026, citing the Light Electric Vehicle Association, 2.2 million e-bikes were imported into the United States in 2025, marking a 29% increase over 2024.

Segmental Insights

Smart Helmets: Fastest-Growing Segment Fueled by Safety and Technology

In the United States Cycling Helmets Market, the Smart Helmet segment is emerging as the fastest-growing category. This rapid expansion is primarily driven by an increasing consumer emphasis on enhanced safety and the continuous integration of advanced technology. Smart helmets offer significant advancements over traditional models through features such as crash detection with automatic emergency alerts, integrated LED lighting for improved visibility, and seamless communication systems. These innovations address the critical demand for superior protection and connectivity, resonating with a market increasingly valuing proactive safety measures. The growing adoption is further influenced by evolving safety awareness, aligning with standards promoted by organizations like the U.S. Consumer Product Safety Commission (CPSC) for bicycle helmets.

Regional Insights

North-East Leadership Driven by Regulations, Infrastructure, and Safety Advocacy

The North-East region demonstrably leads the United States Cycling Helmets Market, driven by a combination of stringent safety regulations and a well-established cycling culture. This dominance is significantly shaped by robust state and municipal helmet mandates, particularly for minors, which consistently propel sales. Furthermore, the region's substantial investments in advanced cycling infrastructure, including extensive bike lane networks and public bike-share initiatives, encourage widespread cycling for both commuting and recreational purposes. These factors, alongside an elevated public safety awareness supported by various advocacy organizations, collectively ensure high helmet adoption rates within the North-East.

Recent Developments

-

In March 2025, POC released its new Cytal road helmet and Cularis mountain bike helmet, which achieved leading safety distinctions. Both helmet models were ranked as the safest in their respective categories by Virginia Tech's Helmet Lab, highlighting breakthrough research in impact protection. The company emphasized that these helmets integrate advanced safety performance and enhanced ventilation, utilizing technologies such as the MIPS Air Node system to mitigate rotational impact forces, thereby strengthening offerings in the United States cycling helmets market.

-

In August 2024, Trek introduced three new mountain bike helmets to the United States cycling helmets market, featuring enhanced WaveCel safety technology. The new models, including the Quantum, Rally, and Blaze WaveCel, were designed to be lighter and offer improved cooling. These helmets received a 5-star safety rating from Virginia Tech, an independent testing laboratory. The products comply with U.S. CPSC safety standards for bicycle helmets and became available to consumers through Trek retailers and online in select markets.

-

In April 2024, a strategic partnership was announced between Aleck and SMITH, focused on integrating Aleck Crash Sensor (Aleck CS) technology into SMITH's performance cycling helmets for the North American market. This collaboration introduced an intelligent impact detection system that identifies serious crashes and sends emergency notifications with GPS location to pre-selected contacts. SMITH became the first brand in North America to offer cycling helmets with this integrated safety feature across four models, including the Forefront 2, Payroll, Trace, and Triad.

-

In February 2024, Specialized launched its new Propero 4 road bike helmet within the United States market. The helmet's development prioritized advancements in both aerodynamics and ventilation, drawing on technologies from previous S-Works models. This new product achieved a 5-star safety rating from the Virginia Tech helmet testing laboratory, an internationally recognized standard for independent helmet evaluation. The introduction of the Propero 4 aimed to provide a high-performance option for a broader range of cyclists.

Key Market Players

- Bell Helmets

- Giro

- Specialized Bicycle Components

- Smith Optics

- POC Sports

- Trek Bicycle Corporation

- Cannondale

- Scott Sports

- Rudy Project

- Kask

|

By Type

|

By Distribution Channel

|

By Region

|

- Conventional Helmet

- Smart Helmet

|

- Online

- Department & discount stores

- Specialty & sports shops

|

- Northeast

- Midwest

- South

- West

|

Report Scope:

In this report, the United States Cycling Helmets Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

United States Cycling Helmets Market, By Type:

-

Conventional Helmet

-

Smart Helmet

-

United States Cycling Helmets Market, By Distribution Channel:

-

Online

-

Department & discount stores

-

Specialty & sports shops

-

United States Cycling Helmets Market, By Region:

-

Northeast

-

Midwest

-

South

-

West

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the United States Cycling Helmets Market.

Available Customizations:

United States Cycling Helmets Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

United States Cycling Helmets Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com