|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 2.67 Billion

|

|

CAGR (2026-2031)

|

6.88%

|

|

Fastest Growing Segment

|

Generic Drugs

|

|

Largest Market

|

Dubai

|

|

Market Size (2031)

|

USD 3.98 Billion

|

Market Overview

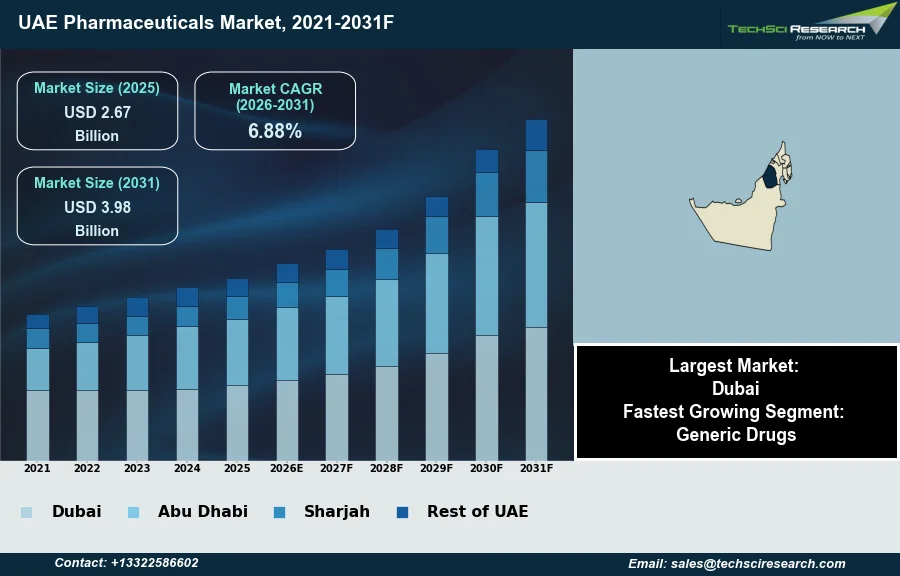

The UAE Pharmaceuticals Market will grow from USD 2.67 Billion in 2025 to USD 3.98 Billion by 2031 at a 6.88% CAGR. Pharmaceuticals are substances employed in the diagnosis, treatment, or prevention of disease and for restoring, correcting, or modifying organic functions. The UAE Pharmaceuticals Market is propelled by several fundamental drivers including increasing healthcare expenditure, a rising prevalence of chronic diseases such as diabetes and cardiovascular conditions, and robust government initiatives focused on developing healthcare infrastructure and local manufacturing capabilities. For example, according to the Dubai Health Authority, in 2025, the number of licensed healthcare facilities in Dubai reached approximately 5,800, and the private healthcare workforce exceeded 69,400 professionals, underscoring significant sector investment and growing demand.

Nonetheless, a substantial challenge hindering market expansion is the pronounced reliance on imported pharmaceutical products, with the UAE importing approximately 90% of its drugs. This dependence exposes the market to potential global supply chain vulnerabilities and contributes to elevated product costs for end-users.

Key Market Drivers

Chronic Disease Burden Drives Pharmaceutical Demand

The rising prevalence of chronic diseases significantly propels the UAE Pharmaceuticals Market, creating a sustained demand for various medications. Lifestyle changes and an aging population contribute to the increasing incidence of conditions such as diabetes, cardiovascular diseases, and obesity. These long-term illnesses necessitate continuous pharmacological interventions for management and treatment, forming a core demand segment for pharmaceutical products. For instance, according to Zavis, in April 2026, chronic conditions in the UAE, including diabetes, cardiovascular disease, and obesity, are driving an estimated AED 17 billion in annual treatment costs. This substantial expenditure reflects the ongoing need for pharmaceutical solutions to manage the health burden of these pervasive diseases.

Public Investment and Policy Support Accelerates Market Growth

Concurrently, significant government healthcare investments and initiatives are fundamentally reshaping the pharmaceutical landscape by enhancing infrastructure, promoting local manufacturing, and improving access to care. The UAE government's strategic focus on developing a robust healthcare ecosystem directly fosters an environment conducive to pharmaceutical market expansion. For example, according to ADEPTs, in its 2026 Federal Budget Yearbook, AED 5.7 billion has been allocated to healthcare within the UAE's federal budget for 2026, underscoring a strong financial commitment. This investment supports advanced medical facilities and services, which in turn increases the consumption of pharmaceutical products. Overall, according to Pharma Solutions, in May 2025, the UAE pharmaceutical market is projected to reach $4.7 billion in revenue by 2025, demonstrating the sector's robust growth.

Download Free Sample Report

Key Market Challenges

Import Dependence Drives Supply Risks and Cost Implications

The pronounced reliance on imported pharmaceutical products presents a significant challenge to the UAE Pharmaceuticals Market. This dependency directly impedes market expansion by exposing it to global supply chain vulnerabilities, which can lead to potential shortages of essential medicines. Furthermore, the necessity of importing a substantial volume of drugs contributes to elevated product costs for end-users due to logistics, tariffs, and other associated expenses. According to the Pharmaceutical Landscape in the GCC, in 2024, the UAE's import dependency for pharmaceuticals was approximately 80%.

External Dependence Impedes Domestic Manufacturing Growth and Pricing Competitiveness

This high level of external reliance can hinder the robust growth of domestic manufacturing capabilities, despite governmental efforts to foster local production. Consequently, it limits the market's ability to achieve greater self-sufficiency and establish more competitive pricing structures within the local healthcare sector, thereby impacting overall market dynamics and long-term development.

Key Market Trends

Digital Transformation in UAE Pharmaceuticals: AI, Analytics, and Telemedicine

Digital transformation in pharmaceutical operations is reshaping the UAE market by enhancing efficiency and innovation across the value chain. This trend encompasses artificial intelligence for drug discovery, advanced data analytics for supply chain optimization, and telemedicine platforms that improve patient access. The adoption of digital tools streamlines research and development, reduces operational costs, and facilitates responsive manufacturing and distribution networks. Enhanced data management systems, for instance, allow for better tracking of drug efficacy and adverse events, contributing to improved patient safety. According to Spectronix Consultancy, June 2026, a report by the Ministry of Health and Prevention (MOHAP) reveals a 35% year-on-year increase in investment within the healthcare technology sector.

Expansion of Biologics and Biosimilars and Related Investment

The expansion of the biologics and biosimilars market is another pivotal trend influencing the UAE pharmaceuticals sector. Biologics, derived from living organisms, offer targeted therapies for complex diseases, while biosimilars provide more affordable alternatives, increasing patient access to advanced treatments. This growth fosters investment in specialized manufacturing capabilities and research infrastructure within the UAE, moving beyond traditional small-molecule production. The increasing availability of biosimilars also alleviates healthcare expenditure pressures, creating a more sustainable pharmaceutical landscape. According to The Middle East Insider, January 2026, Julphar (Gulf Pharmaceutical Industries) announced an investment of AED 1 billion to modernize facilities and expand vaccine and biologic production lines.

Segmental Insights

Regulatory Support and Cost Advantages Drive Generics Growth in UAE

In the UAE Pharmaceuticals Market, generic drugs represent the fastest-growing segment, primarily driven by the increasing demand for cost-effective healthcare solutions. This rapid expansion is a direct result of government strategies aimed at enhancing healthcare affordability and accessibility for the populace. Regulatory bodies, such as the Ministry of Health and Prevention (MOHAP), have played a pivotal role by implementing policies that promote the prescription and dispensing of generic medications, while simultaneously ensuring their stringent quality and safety standards. This supportive regulatory environment, coupled with the inherent cost advantages of generics over branded counterparts, significantly contributes to their widespread adoption among patients and healthcare providers, addressing the growing need for sustainable treatment options, particularly for chronic conditions.

Regional Insights

Dubai's Strategic Position and Ecosystem Drive UAE Pharmaceutical Leadership.

Dubai leads the UAE Pharmaceuticals Market due to a confluence of strategic advantages and a supportive ecosystem. Its pivotal geographic position serves as a gateway for pharmaceutical companies accessing broader regional markets across the Middle East, Africa, and Asia. The emirate boasts advanced healthcare infrastructure, including modern hospitals, research centers, and pharmaceutical manufacturing facilities. Furthermore, Dubai's favorable regulatory environment, championed by the Dubai Health Authority (DHA), along with well-developed logistics infrastructure, including free zones like Jebel Ali, attracts multinational corporations for regional distribution and operations. These elements collectively reinforce Dubai's dominance in the pharmaceutical landscape.

Recent Developments

-

In May 2025, Tabuk Pharmaceuticals and Globalpharma announced a strategic cooperation agreement aimed at advancing local pharmaceutical manufacturing within the UAE. This partnership was established to enable Globalpharma to undertake the local production of several key pharmaceutical products developed by Tabuk Pharmaceuticals within the United Arab Emirates. The collaboration between these leading pharmaceutical companies from the Middle East and North Africa highlighted a mutual commitment to strengthening regional production capacities. This initiative was structured to increase the availability of essential medicines in the UAE and contribute to the broader objective of national pharmaceutical self-sufficiency.

-

In January 2025, Globalpharma, a Dubai-based pharmaceutical manufacturer and a wholly owned subsidiary of Dubai Investments, unveiled plans to introduce 25 new pharmaceutical products in the UAE market throughout 2025. These forthcoming launches were designated to cover key therapeutic areas, including diabetes, cardiovascular conditions, gastroenterology, and orthopaedics. This strategic initiative underscored Globalpharma's commitment to innovation and accessibility, aiming to address the evolving healthcare demands within the region. The expansion represented a pivotal component of the company's broader growth strategy, focusing on strengthening its regional impact and diversifying its portfolio of branded and specialty medicines.

-

In January 2024, Globalpharma, a prominent pharmaceutical manufacturer in the UAE, introduced two new medicines at DUPHAT 2024, thereby expanding the country's pharmaceutical offerings. These introductions included a distinct herbal medicine, conceptualized with inspiration from UAE heritage, and an advanced combination medicine specifically designed for the management of dyslipidaemia, incorporating Rosuvastatin and Ezetimibe. These additions enhanced Globalpharma's portfolios in both its herbal and nutraceutical as well as its cardio-metabolic franchises. The company underscored its robust local manufacturing capabilities located within Dubai Investments Park, ensuring in-house production of these new treatments for the UAE market.

-

In 2024, STADA Arzneimittel partnered with ADCAN Pharma in a significant collaboration intended to enhance access to crucial medicines across the UAE. This alliance strategically leveraged ADCAN Pharma's established local production capabilities and STADA Arzneimittel's extensive global marketing network. The primary objective of this partnership was to facilitate the efficient distribution of a diverse range of high-quality pharmaceutical products within the UAE market. Such strategic collaborations are considered instrumental in advancing the nation's pharmaceutical sector, fostering local manufacturing growth, and ensuring a consistent supply of innovative and accessible treatments for patients in the region.

Key Market Players

- Julphar

- Neopharma

- Gulf Pharmaceutical Industries

- Hikma Pharmaceuticals UAE

- Pfizer UAE

- Novartis UAE

- Sanofi UAE

- GSK UAE

- Merck UAE

- AstraZeneca UAE

|

By Drug Type

|

By Product Type

|

By Application

|

By Distribution Channel

|

By Region

|

- Generic Drugs

- Branded Drugs

|

- Over-The-Counter Drugs

- Prescription Drugs

|

- Cardiovascular

- Oncology

- Metabolic Disorder

- Musculoskeletal

- Anti-infective

- Others

|

- Retail Pharmacy

- Hospital Pharmacy

- E-Pharmacy

|

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

|

Report Scope:

In this report, the UAE Pharmaceuticals Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

UAE Pharmaceuticals Market, By Drug Type:

-

Generic Drugs

-

Branded Drugs

-

UAE Pharmaceuticals Market, By Product Type:

-

Over-The-Counter Drugs

-

Prescription Drugs

-

UAE Pharmaceuticals Market, By Application:

-

Cardiovascular

-

Oncology

-

Metabolic Disorder

-

Musculoskeletal

-

Anti-infective

-

Others

-

UAE Pharmaceuticals Market, By Distribution Channel:

-

Retail Pharmacy

-

Hospital Pharmacy

-

E-Pharmacy

-

UAE Pharmaceuticals Market, By Region:

-

Dubai

-

Abu Dhabi

-

Sharjah

-

Rest of UAE

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the UAE Pharmaceuticals Market.

Available Customizations:

UAE Pharmaceuticals Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).