|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 974.19 Million

|

|

CAGR (2026-2031)

|

6.93%

|

|

Fastest Growing Segment

|

Humidifier & Dehumidifier

|

|

Largest Market

|

Dubai

|

|

Market Size (2031)

|

USD 1456.27 Million

|

Market Overview

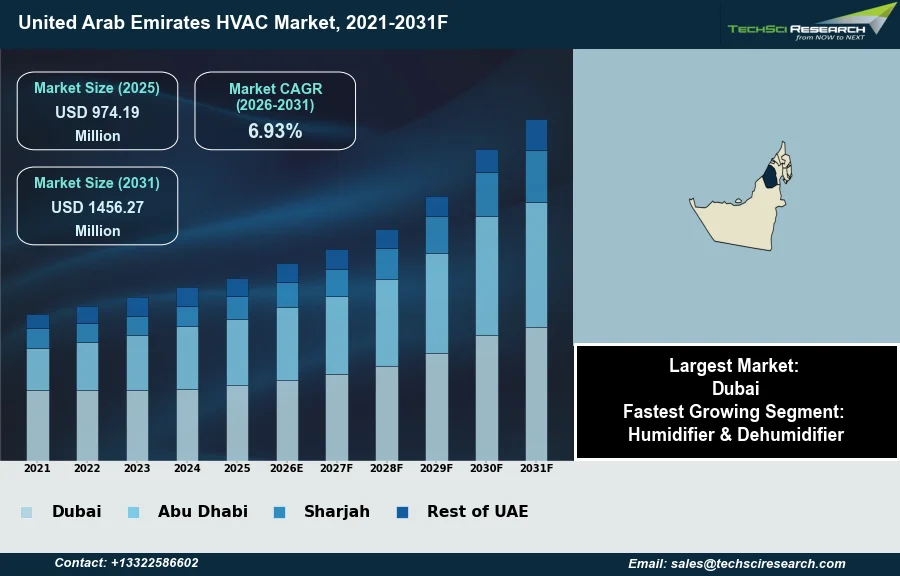

The HVAC Market in United Arab Emirates will grow from USD 974.19 Million in 2025 to USD 1456.27 Million by 2031 at a 6.93% CAGR. The United Arab Emirates Heating, Ventilation, and Air Conditioning (HVAC) market encompasses systems designed to regulate indoor air quality, temperature, and humidity across residential, commercial, and industrial environments. This market's growth is primarily driven by the nation's extreme climatic conditions, which necessitate extensive cooling solutions. Additionally, rapid urbanization and significant government investments in large-scale infrastructure and real estate projects, including smart cities and tourism facilities, consistently fuel demand for advanced HVAC systems.

According to the Gulf Organization for Research and Development, in 2024, over 70% of energy consumption in UAE buildings was attributed to cooling, underscoring the critical role of HVAC. Despite robust market expansion, a significant challenge impeding further growth is the substantial initial investment required for the procurement and installation of sophisticated HVAC technologies, which can deter adoption, particularly among smaller enterprises.

Key Market Drivers

Extreme UAE Climate Drives Ongoing HVAC Demand

The extreme climatic conditions prevalent across the United Arab Emirates represent a fundamental and enduring driver for the HVAC market. With temperatures frequently reaching severe highs, the demand for robust and efficient cooling systems is constant and critical for habitability and productivity across all sectors. The intense heat necessitates sophisticated HVAC solutions capable of enduring harsh operational demands while providing consistent indoor comfort. According to the National Centre of Meteorology (NCM), on August 1, 2025, temperatures peaked at 51.8 °C in Sweihan, Al Ain region, marking the highest recorded temperature in the UAE that year. This persistent need for powerful cooling infrastructure fuels ongoing investment in advanced air conditioning technologies.

Urbanization and Infrastructure Growth Boost HVAC Demand

Complementing the climatic demands, rapid urbanization and extensive infrastructure development significantly propel the UAE HVAC market. The nation continues to witness substantial investments in constructing new residential areas, commercial complexes, hospitality establishments, and large-scale public infrastructure projects. These developments inherently require comprehensive HVAC installations from the initial design phase through ongoing operation. As of June 2026, the Abu Dhabi Projects and Infrastructure Centre allocated approximately Dh35 billion for 11 transportation and road projects, including over 300 kilometers of new roads, bridges, tunnels, and major intersections, underscoring the scale of ongoing infrastructure expansion. This extensive construction pipeline directly translates into sustained demand for HVAC systems and related services. Further reflecting this growth, by year-end 2025, DEWA's customer base expanded to 1,327,182 accounts, reflecting a 4.48% increase.

Download Free Sample Report

Key Market Challenges

Upfront Investment Barriers Hamper UAE HVAC Growth

The substantial initial investment required for procuring and installing advanced HVAC technologies presents a significant impediment to the growth of the United Arab Emirates HVAC market. This financial barrier disproportionately affects smaller enterprises, limiting their capacity to adopt or upgrade to modern climate control systems. Such high upfront costs deter investment, particularly for businesses operating with tighter capital budgets, preventing the widespread integration of more efficient and environmentally conscious HVAC solutions.

Construction-Cost Inflation and Tender Pressures Limit HVAC Adoption

The impact of elevated expenses is notable across the construction sector, which directly influences HVAC market demand. According to Turner & Townsend's 2025 construction market intelligence, materials now constitute approximately 60 percent of construction baseline costs in the UAE, while tender price inflation for 2025 is forecast at 3.3 percent. These rising input costs translate directly into higher overall project expenses, including HVAC installations. This trend restricts the adoption of high-performance HVAC systems that offer long-term operational savings and improved indoor air quality, thereby hindering the market's expansion and technological advancement.

Key Market Trends

Smart HVAC: IoT and AI for Efficiency and Reliability

The integration of smart and connected HVAC systems represents a pivotal trend reshaping the United Arab Emirates market, driven by the imperative for enhanced operational efficiency and precise environmental control. These advanced systems, leveraging IoT sensors and artificial intelligence, enable real-time monitoring, predictive maintenance, and optimized energy consumption tailored to occupancy and external conditions. Such capabilities are crucial in a region with high cooling demands, allowing building operators to significantly reduce waste and improve system reliability. According to DEWA, in August 2025, their smart grid systems utilize artificial intelligence and the Internet of Things to analyze 15 million data points daily, underscoring the scale and sophistication of connected infrastructure aimed at optimizing energy use.

Renewable and Hybrid HVAC: Expanding Clean Energy Use

Concurrently, the adoption of renewable and hybrid energy HVAC systems is gaining substantial traction as the UAE diversifies its energy mix and pursues sustainability goals. This trend involves incorporating solar thermal, geothermal, or waste heat recovery technologies into cooling and heating infrastructure, aiming to lessen reliance on conventional fossil fuels for energy-intensive climate control. These sustainable approaches contribute to a reduced carbon footprint and offer long-term operational cost savings. Domestically, the UAE's installed renewable energy capacity has surpassed 7.7 gigawatts, as reported by TECHx Media in June 2026, indicating a robust shift towards cleaner energy sources that can power these advanced HVAC applications.

Segmental Insights

Climate-Driven Growth and Regulatory Push for Humidity Management in the UAE

The Humidifier & Dehumidifier segment is experiencing rapid growth in the United Arab Emirates HVAC Market, primarily driven by the region's extreme climate, which is characterized by high ambient humidity, particularly in coastal areas. This environmental factor necessitates effective humidity control solutions to ensure occupant comfort and mitigate challenges such as mold formation. Furthermore, stringent indoor air quality regulations, enforced by bodies like Dubai Municipality and the Health Authority Abu Dhabi, mandate the maintenance of optimal indoor humidity levels across commercial, public, and healthcare facilities. These regulatory imperatives, alongside increasing awareness of public health and the need to protect sensitive assets from moisture-related damage, are significantly accelerating the adoption of advanced humidity management systems.

Regional Insights

Dubai's HVAC Market Leadership: Urban Growth, Climate, and Regulatory Initiatives

Dubai stands as the leading region within the United Arab Emirates HVAC market, primarily driven by its extensive urbanization and continuous infrastructure development. As a prominent global business and tourism hub, the emirate consistently undertakes large-scale commercial, residential, and hospitality projects, demanding sophisticated cooling solutions. The inherently extreme arid climate necessitates robust HVAC systems for essential indoor comfort. Furthermore, stringent mandates like the Dubai Green Building Regulations actively promote the adoption of advanced, energy-efficient HVAC technologies, including the widespread implementation of district cooling systems managed by entities such as Emirates Central Cooling Systems Corporation (Empower), thereby reinforcing Dubai's market dominance.

Recent Developments

-

In November 2025, Himel strengthened its presence in the United Arab Emirates HVAC market with the introduction of its "I Love Control" series. This new flagship product line features smart industrial control and automation solutions specifically designed for the heating, ventilation, and air conditioning sector. The launch, showcased at Big 5 Global 2025 in Dubai, marked Himel's expansion into the HVAC-centric industrial automation segment. The series aims to optimize power management across ventilation, pumping, air handling units, and chillers, promoting sustainability and energy efficiency within the UAE's rapidly growing HVAC landscape.

-

In November 2025, LG Electronics Inc. entered a strategic partnership with Expo City Dubai Authority to supply advanced heating, ventilation, and air conditioning (HVAC) solutions and artificial intelligence (AI) home solutions for a smart city development in Dubai. This collaboration positions LG as a comprehensive solutions provider across business-to-consumer, business-to-business, and business-to-government segments in the Middle East. The initiative aligns with the UAE government's vision for a sustainable city that integrates AI and renewable energy, reinforcing the country's carbon neutrality goals and demand for energy-efficient infrastructure.

-

In April 2025, Foster International announced the launch of its own HVAC brand, FOSTER, in Dubai, UAE. This new brand offers a comprehensive array of energy-efficient systems, including HiWall split units, ducted split units, and advanced Variable Refrigerant Flow (VRF) systems utilizing inverter technology. For industrial applications, the product line features robust package air conditioners and chilled water fan coil units. The introduction of FOSTER reinforces the company's commitment to delivering high-performance, eco-conscious designs and smart HVAC technologies, aiming to redefine comfort and efficiency within the UAE's HVAC sector.

-

In March 2025, National Central Cooling Company (Tabreed) formed a joint venture with Dubai Holding Investments to provide district cooling services for the Palm Jebel Ali development in Dubai. Tabreed holds a 51% stake in this agreement, which entails an estimated investment of AED 1.5 billion for the district cooling network. This significant concession, representing approximately one-fifth of Tabreed's connected capacity, is set to enhance its competitive position in the dynamic Dubai market. The construction of the network was scheduled to commence in the second quarter of 2025, with initial cooling services anticipated by 2027.

Key Market Players

- Daikin Middle East and Africa FZE

- Carrier Global Corporation

- LG Electronics Gulf FZE

- Mitsubishi Electric Corporation

- Samsung Gulf Electronics Co. Ltd.

- SKM Air Conditioning LLC

- Johnson Controls International plc

- Trane Technologies plc

- Danfoss A/S

- Gree Electric Appliances Inc. of Zhuhai

|

By Equipment

|

By End User

|

By Region

|

- Heat Pump

- Air Conditioner

- Humidifier & Dehumidifier

- Others

|

- Residential

- Commercial

- Industrial

|

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

|

Report Scope:

In this report, the United Arab Emirates HVAC Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

United Arab Emirates HVAC Market, By Equipment:

-

Heat Pump

-

Air Conditioner

-

Humidifier & Dehumidifier

-

Others

-

United Arab Emirates HVAC Market, By End User:

-

Residential

-

Commercial

-

Industrial

-

United Arab Emirates HVAC Market, By Region:

-

Dubai

-

Abu Dhabi

-

Sharjah

-

Rest of UAE

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the United Arab Emirates HVAC Market.

Available Customizations:

United Arab Emirates HVAC Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

United Arab Emirates HVAC Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com