|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

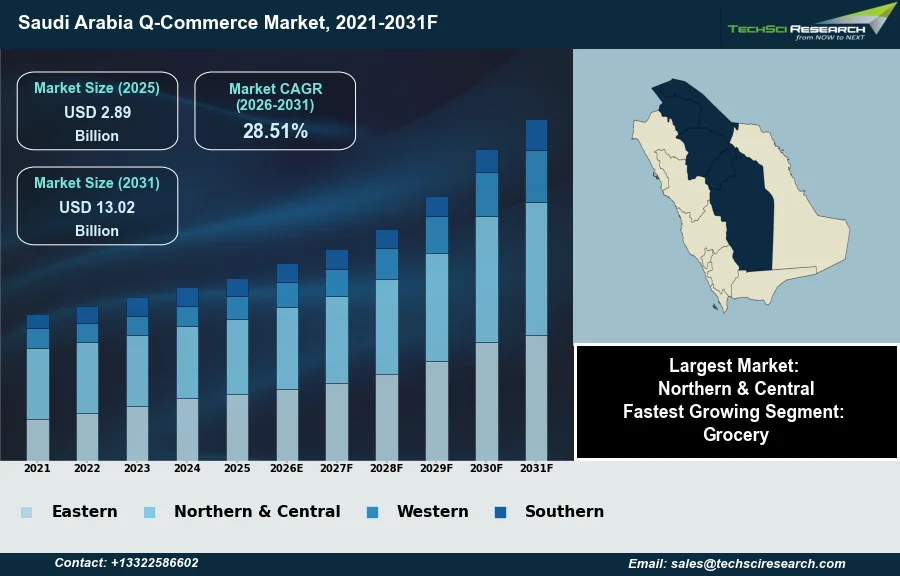

Market Size (2025)

|

USD 2.89 Billion

|

|

CAGR (2026-2031)

|

28.51%

|

|

Fastest Growing Segment

|

Grocery

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 13.02 Billion

|

Market Overview

The Q-Commerce Market in Saudi Arabia will grow from USD 2.89 Billion in 2025 to USD 13.02 Billion by 2031 at a 28.51% CAGR. Quick commerce, or Q-commerce, refers to a specialized e-commerce model focusing on ultra-fast delivery of small-basket orders, typically within minutes, from strategically positioned micro-fulfillment centers. Market growth in Saudi Arabia is significantly driven by evolving consumer expectations for immediate gratification and convenience, coupled with high smartphone penetration and digital literacy among the young population. Furthermore, government initiatives under Vision 2030, emphasizing digital transformation and a cashless economy, provide substantial foundational support. According to the Saudi Central Bank, e-commerce sales via Mada cards in the first quarter of 2025 reached over SAR 69.3 billion, highlighting the robust digital payment infrastructure underpinning the market's expansion.

A considerable challenge impeding market expansion is the inherent high operational and logistics costs. This includes expenses related to maintaining extensive dark store networks and large delivery fleets, further complicated by the geographic spread of Saudi Arabia and the need to serve diverse population densities efficiently.

Key Market Drivers

Government Support and Infrastructure Investment

Supportive government initiatives under Vision 2030 are a primary catalyst for the expansion of the Saudi Arabia Q-Commerce Market, fostering an environment conducive to digital business growth and advanced logistics. The national transformation blueprint actively promotes economic diversification and digital transformation across various sectors. These efforts include significant investments aimed at enhancing infrastructure, which directly benefits the rapid delivery model of Q-commerce. For instance, according to Logistix SA in 2025, over SAR 1 trillion (USD 266+ billion) has been allocated for transport and logistics infrastructure development, providing a robust foundation for efficient last-mile delivery and the establishment of sophisticated micro-fulfillment centers. This strategic government backing ensures regulatory flexibility, promotes innovation, and establishes a strong digital framework essential for quick commerce operations.

Demographic Momentum and Digital Readiness

Concurrently, the presence of a large young and tech-savvy population significantly drives demand within the Saudi Arabia Q-Commerce Market. This demographic exhibits a high propensity for digital adoption and a strong preference for on-demand services, aligning perfectly with the instant gratification model of quick commerce. The widespread digital literacy and extensive smartphone penetration among this consumer base facilitate seamless access to Q-commerce platforms. According to the General Authority for Statistics (GASTAT), in January 2026, 99.0% of individuals aged 15–74 reported using the internet across Saudi Arabia. This high level of digital engagement translates into a substantial user base ready to adopt and frequently utilize quick commerce applications for various purchases. According to Bloomberg News, in 2025, a Q-commerce player, Ninja, secured USD 250 million in Series C funding at a USD 1.5 billion valuation.

Download Free Sample Report

Key Market Challenges

Operational costs and geography impede expansion

The inherent high operational and logistics costs represent a significant challenging factor impeding the expansion of the Saudi Arabia Q-Commerce market. These expenses are predominantly driven by the necessity to establish and maintain extensive dark store networks and large delivery fleets. The geographical spread of Saudi Arabia, coupled with the need to efficiently serve diverse population densities, adds considerable complexity and cost to last-mile delivery operations. This directly impacts the profitability and scalability of Q-commerce providers, limiting their ability to expand services across all regions.

Capital-intensive infrastructure and margin compression

Maintaining the specialized infrastructure required for ultra-fast delivery demands substantial capital investment in warehousing and transportation assets. For example, according to ANB Capital, SAL Saudi Logistics Services, a key industrial player, in April 2025 indicated a lease rate of approximately SAR 16.0 per square meter for its logistics zone in Riyadh, with an expected annual increase. Such significant operational expenditures, alongside the continuous investment in advanced technology and a large workforce, compress profit margins for Q-commerce companies. This financial pressure can constrain their ability to introduce competitive pricing or extend their service footprint, thereby directly hampering broader market penetration and overall growth.

Key Market Trends

Sustainable and Automated Delivery Transforming Saudi Q-Commerce

The Saudi Arabia Q-Commerce market is undergoing a notable transformation with the increasing adoption of sustainable and automated delivery systems. This trend directly addresses the high operational and logistics costs inherent in rapid delivery by enhancing efficiency and reducing reliance on traditional labor-intensive models. Such advancements also align with broader environmental goals, contributing to reduced carbon emissions within urban environments. For instance, Jahez, in partnership with ROSHN Group, launched Saudi Arabia's first commercial autonomous food delivery service in July 2025, deploying five self-driving robots in Riyadh's ROSHN Front Business Area. This initiative demonstrates a strategic shift towards leveraging technology to optimize last-mile delivery and improve service reliability.

AI-Driven Logistics and Inventory Optimization

Concurrently, advancements in AI-powered logistics and inventory optimization are proving critical for market players. This trend enables Q-commerce providers to manage complex supply chains more effectively by improving demand forecasting, reducing waste, and ensuring product availability. AI tools allow for real-time, data-driven decision-making, which is vital in a market characterized by volatile consumer demand and diverse population densities. For example, according to Blue Yonder, May 2026, in an Arab News article, some platforms now process over 25 billion AI predictions a day, demonstrating the immense scale at which data-driven insights are being utilized to enhance sensing, prediction, and action across supply chain operations. These intelligent systems contribute significantly to optimizing operational expenditure and strengthening resilience against supply chain disruptions.

Segmental Insights

Grocery as the Fastest-Growing Segment in Saudi Arabia's Q-Commerce Market

The key segmental insight for Saudi Arabia's Q-Commerce Market reveals grocery as the fastest-growing segment. This rapid expansion is primarily driven by evolving consumer lifestyles, particularly among the urban and tech-savvy population, who increasingly prioritize convenience and time-saving solutions for daily essentials. The high frequency of grocery purchases, coupled with a strong preference for ultra-fast home delivery of fresh produce and household staples, fuels this trend. Furthermore, strategic investments in expansive dark store networks and advancements in last-mile logistics across metropolitan areas enable quick commerce platforms to meet stringent delivery expectations within minutes. The Kingdom's ongoing digital transformation initiatives, supported by Vision 2030, further foster an environment conducive to the sustained growth of online grocery services.

Regional Insights

Urban Density and Digital Readiness Drive Northern & Central Q-Commerce Leadership

The Northern & Central region demonstrably leads the Saudi Arabia Q-Commerce Market, primarily driven by the significant concentration of population within its urban centers, particularly Riyadh. This dominance stems from a combination of factors, including the region's high disposable incomes and the prevailing fast-paced lifestyle, which collectively fuel substantial demand for instant delivery services. Furthermore, Northern & Central benefits from superior digital infrastructure development and a technologically adept consumer base, providing a robust foundation for quick commerce operations. Major platforms have strategically established their headquarters and primary distribution centers, such as dark stores, in Riyadh, enhancing operational efficiencies and optimizing logistics networks for rapid fulfillment. Government initiatives under Vision 2030 further support the expansion of the digital economy, including smart city developments, which contribute to the region's strong Q-Commerce ecosystem.

Recent Developments

-

In October 2025, noon and Jahez, two prominent Saudi-based on-demand platforms, announced a strategic collaboration designed to enhance quick commerce services across the Kingdom. This partnership integrated noon's quick-commerce infrastructure with Jahez's extensive food-delivery network. Through this alliance, users of the Jahez application gained direct access to noon's rapid "noon Minutes" service, providing a broader selection of retail and grocery categories fulfilled via noon's dark store network. Simultaneously, the noon application incorporated Jahez's food-delivery offerings, connecting its users with over 50,000 restaurants operating across more than 100 Saudi Arabian cities.

-

In August 2025, Jahez, in partnership with ROSHN Group, launched Saudi Arabia's first commercial autonomous food delivery service within the ROSHN Front Business District in Riyadh. This innovative service deployed five self-driving robots, each equipped with over 20 sensors and six cameras, to navigate the area safely and deliver food orders from nearby restaurants during operational hours. The initiative aimed to reduce delivery times and carbon emissions, marking a significant advancement in smart logistics and automation within the Saudi Arabia Q-Commerce Market.

-

In April 2025, the Egyptian quick-commerce startup Rabbit expanded its operations into the Saudi Arabian market by establishing its regional headquarters in Riyadh. The company launched its services through a network of strategically located "dark stores" or fulfillment centers across key neighborhoods in the city. Rabbit planned to deliver 20 million items across major Saudi cities by 2026, leveraging its technology-driven hyperlocal e-commerce model that focuses on rapid delivery of groceries and other essentials, thereby contributing to the growing e-grocery segment in the Kingdom.

-

In September 2024, Jahez Group introduced its "Ubayyah" electric-vehicle (EV) fleet, marking a new product launch aimed at sustainable logistics within the Saudi Arabia Q-Commerce Market. The Transport General Authority endorsed this initiative, which supports the national goal of reducing carbon emissions from transportation. These new EVs, tailored for Jahez, operate on solar power and emit zero carbon. The initial deployment comprised 30 vehicles capable of traveling up to 200 km on a single charge, representing a forward-thinking approach to environmentally impactful delivery concepts.

Key Market Players

- Noon Q-Commerce

- Jahez

- Talabat KSA

- HungerStation

- Mrsool

- Glovo KSA

- Amazon.sa Fresh

- Carrefour Now KSA

- Al Othaim Express

- Alshaya Express

|

By Product Type

|

By Platform

|

By Region

|

|

|

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Q-Commerce Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Q-Commerce Market, By Product Type:

-

Saudi Arabia Q-Commerce Market, By Platform:

-

Saudi Arabia Q-Commerce Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Q-Commerce Market.

Available Customizations:

Saudi Arabia Q-Commerce Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Q-Commerce Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com