|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 4.58 Billion

|

|

CAGR (2026-2031)

|

5.82%

|

|

Fastest Growing Segment

|

Processed

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 6.43 Billion

|

Market Overview

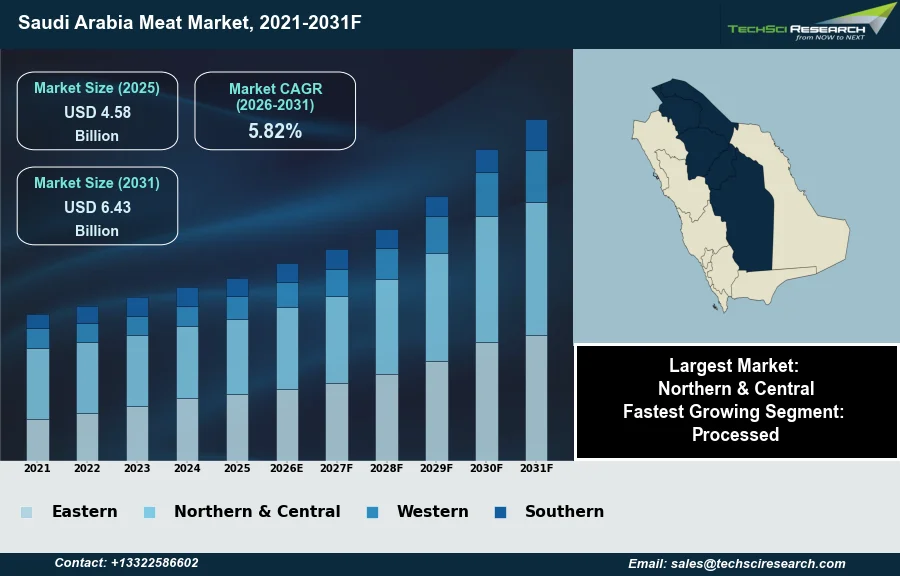

The Meat Market in Saudi Arabia will grow from USD 4.58 Billion in 2025 to USD 6.43 Billion by 2031 at a 5.82% CAGR. The Saudi Arabia meat market primarily encompasses products derived from animal flesh, including poultry, beef, and mutton, which are available in fresh, chilled, and processed forms, maintaining strict adherence to Halal standards. Market expansion is substantially driven by a growing population and increasing urbanization, factors that consistently fuel demand for protein-rich diets. Concurrently, rising disposable incomes empower consumers to purchase higher-value meat products. According to the General Authority for Statistics, annual per capita poultry consumption in Saudi Arabia reached 46.9 kg in 2024. Government initiatives aimed at bolstering food security and local livestock production further contribute to market development.

The domestic poultry sector demonstrates considerable capacity, with Saudi Arabia's broiler chicken production reaching 1.3 million tons in 2024, according to the General Authority for Statistics. However, a significant challenge impeding market expansion is the Kingdom's substantial reliance on meat imports, particularly for red meat, which renders the market vulnerable to global price fluctuations and potential supply chain disruptions. Additionally, inherent resource constraints, notably water scarcity and animal feed availability, present ongoing limitations for extensive local livestock development efforts.

Key Market Drivers

Vision 2030-driven investment to boost domestic meat self-sufficiency

Government initiatives for food security and local production, notably under Vision 2030, represent a pivotal driving factor in the Saudi Arabia meat market by strategically addressing the Kingdom's reliance on imports and fostering domestic capabilities. These comprehensive strategies include significant investments aimed at increasing self-sufficiency in key meat categories. For example, Saudi Arabia plans an SR17 billion ($5 billion) investment to boost poultry production, aiming for an 80 percent self-sufficiency rate by 2025. This targeted approach not only bolsters local supply chains but also encourages advanced farming techniques and infrastructure development within the livestock sector. Such governmental support is instrumental in diversifying the economy and reducing vulnerability to global supply chain disruptions and price volatility.

Halal integrity driving production standards and investment

The strong cultural and religious preference for Halal meat also profoundly shapes the market, influencing all aspects from production to consumption. Consumers in Saudi Arabia strictly adhere to Islamic dietary laws, ensuring that all meat products are Halal-certified. This deeply embedded cultural requirement mandates specific slaughtering practices and processing standards, thereby impacting both domestic producers and international suppliers. The emphasis on Halal integrity drives investments in compliant facilities; in April 2025, BRF's board approved the development of a new processed food plant in Jeddah, which is projected to provide Saudi Arabia with over 40,000 tonnes of halal-certified poultry and beef products annually upon completion. Overall, Saudi Arabia's imports of meat and edible meat offal totaled US$2.85 billion during 2024.

Download Free Sample Report

Key Market Challenges

Import Dependence and Resource Constraints Limit Local Livestock Growth

The Saudi Arabia meat market faces a significant challenge in its substantial reliance on meat imports, particularly for red meat. This dependency directly impedes stable market expansion by exposing the Kingdom to considerable global price volatility and potential supply chain disruptions. Inherent resource constraints, notably water scarcity and animal feed availability, continuously limit extensive local livestock development efforts.

Import Dependency Elevates Prices and Threatens Food Security

This reliance on external sources means that any shifts in international commodity prices or unforeseen interruptions in global trade routes can rapidly inflate the cost of imported meat products. According to the USDA Foreign Agricultural Service, in July 2025, Saudi Arabia relied on imports to meet up to 80 percent of its overall food consumption needs. This high degree of import dependency, especially for red meat, subjects the market to external economic pressures. Consequently, higher import costs can translate into increased retail prices, affecting consumer purchasing power and potentially curbing demand. Moreover, disruptions in the supply chain, such as those caused by geopolitical events or logistical challenges, can lead to shortages, impacting market stability and food security within the Kingdom.

Key Market Trends

Rising Demand for Premium, Healthier Meat and Ethical Sourcing

Consumers in the Saudi Arabia meat market are increasingly shifting towards premium and health-conscious meat options. This trend reflects a growing consumer awareness regarding product quality, sourcing, and health benefits, moving beyond basic commodity choices. Consumers are demonstrating a greater willingness to invest in meat products perceived as healthier, such as organic, antibiotic-free, or specific cuts associated with better nutrition. This rising preference is prompting meat producers and retailers to diversify their offerings to cater to discerning buyers seeking superior quality and ethical sourcing. For instance, according to Matrix BCG, April 2026, in 'What is Growth Strategy and Future Prospects of Almarai Company?', Almarai aims for a 10% share of the premium red meat market by 2026, highlighting the strategic importance companies place on this segment.

Expansion of Online Meat Retail and Delivery

Another significant trend influencing the Saudi Arabia meat market is the expansion of online meat retail and delivery services. The increasing digitalization of consumer purchasing habits, coupled with advancements in logistics infrastructure, is driving the growth of e-commerce platforms for fresh and processed meat products. Consumers benefit from the convenience of doorstep delivery, wider product selections, and often competitive pricing, which appeals particularly to busy urban populations. This channel expansion also enables smaller, specialized meat providers to reach a broader customer base without extensive physical retail presence. According to Gulfood, in 'Grocery Trade Trends 2025', Saudi Arabia's online grocery market was valued at USD 1.54 billion in 2024, indicating a substantial and growing digital sales environment that includes meat products.

Segmental Insights

Processed Meat: Fastest-Growing Segment Fueled by Convenience, Urbanization, and Halal Certification

The key segmental insight for the Saudi Arabia Meat Market reveals the Processed segment as the fastest growing. This significant expansion is primarily driven by rapid urbanization and evolving consumer lifestyles, which have led to increased demand for convenient, ready-to-eat food options among busy individuals and households. Rising disposable incomes further enable consumers to purchase these value-added products. Furthermore, the expanding modern retail infrastructure and the adherence to strict halal certification standards, as regulated by the Saudi Food and Drug Authority (SFDA), enhance consumer trust and accessibility to a diverse range of processed meat offerings.

Regional Insights

Drivers Behind Northern and Central Meat Market Leadership

The Northern and Central regions lead the Saudi Arabia Meat Market due to a confluence of robust demographic and economic factors. This dominance is primarily driven by substantial urban populations, particularly in Riyadh and Jeddah, coupled with higher disposable incomes that fuel increased demand for diverse meat products. These regions benefit from a high concentration of modern retail infrastructure, including numerous supermarkets, hypermarkets, and a thriving foodservice sector, which are crucial hubs for efficient meat distribution. Furthermore, ongoing urbanization and strategic logistical advantages ensure superior supply chain connectivity, facilitating product movement and supporting elevated per capita meat consumption reflecting contemporary urban dietary patterns.

Recent Developments

-

In December 2025, Tanmiah Food Company introduced a new selection of frozen breaded chicken products tailored for both retail and foodservice sectors in Saudi Arabia. This innovative product line was exclusively manufactured using 100% fresh Saudi chicken, thereby establishing a new standard for quality and added value within the processed meats category. The launch underscored Tanmiah's commitment to prioritizing locally sourced ingredients, a significant shift from the previous reliance on imported frozen chicken breast. This initiative was aligned with Saudi Arabia's food security objectives, reinforcing domestic production and enhancing self-sufficiency within the Saudi Arabia Meat Market.

-

In July 2025, Brazilian meat processor BRF launched its inaugural line of chilled chicken products, which were produced within Saudi Arabia. The company set an objective to capture a 10% share of the Saudi Arabian chilled chicken market within eighteen months. This strategic introduction aimed to bolster BRF's market presence in Saudi Arabia and decrease its dependency on imported goods by enhancing local supply capabilities. The launch directly responded to the substantial consumer demand for chilled chicken, underscoring a commitment to local production and market penetration within the Saudi Arabia Meat Market.

-

In May 2025, Tanmiah Food Company, a prominent Saudi poultry and food producer, signed a Memorandum of Understanding with Poulta Inc., an agri-tech startup from the U.S. This strategic collaboration focused on the comprehensive digitization of Tanmiah's poultry operations across Saudi Arabia. The initiative incorporated advanced technologies such as artificial intelligence, cloud computing, big data analytics, and the Internet of Things to optimize production processes. The partnership also encompassed the formation of a joint venture to deliver digital transformation services for regional livestock businesses and the establishment of a new Agriculture Technology Research Center in Saudi Arabia, advancing breakthrough research for the Saudi Arabia Meat Market.

-

In March 2025, Hilton Foods entered the Saudi Arabian market through a long-term joint venture with The National Agricultural Development Company (NADEC). The UK-based meat processing company acquired a 49% stake in the partnership and committed an initial investment of US$8.3 million (SAR 31 million) towards the project's total funding of US$16.6 million (SAR 60 million). This collaboration aimed to establish modern meat processing facilities in Saudi Arabia, with NADEC supplying red meat to the operation and integrating products into its distribution network, expanding red meat offerings as the market shifted towards pre-packaged options in the Saudi Arabia Meat Market.

Key Market Players

- Almarai

- SADAFCO

- NADEC

- Al Rabie

- National Food Industries

- Al Othaim

- Lulu Group

- HyperPanda

- Carrefour

- Bin Dawood

|

By Product

|

By Type

|

By Distribution Channel

|

By Region

|

- Chicken

- Beef

- Mutton

- Pork

- Others

|

|

- Hypermarket/Supermarket

- Specialty Stores

- Online

- Others

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Meat Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Meat Market, By Product:

-

Chicken

-

Beef

-

Mutton

-

Pork

-

Others

-

Saudi Arabia Meat Market, By Type:

-

Saudi Arabia Meat Market, By Distribution Channel:

-

Hypermarket/Supermarket

-

Specialty Stores

-

Online

-

Others

-

Saudi Arabia Meat Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Meat Market.

Available Customizations:

Saudi Arabia Meat Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Meat Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com