|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

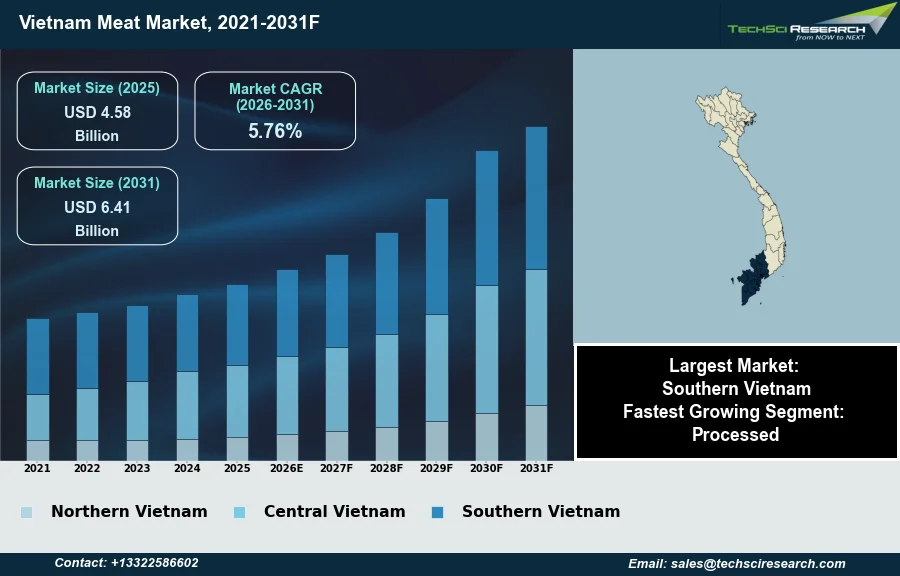

Market Size (2025)

|

USD 4.58 Billion

|

|

CAGR (2026-2031)

|

5.76%

|

|

Fastest Growing Segment

|

Processed

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 6.41 Billion

|

Market Overview

The Meat Market in Vietnam will grow from USD 4.58 Billion in 2025 to USD 6.41 Billion by 2031 at a 5.76% CAGR. The Vietnam Meat Market encompasses the production, processing, distribution, and consumption of animal flesh for human food, primarily including pork, poultry, and beef. This market's robust expansion is primarily driven by escalating disposable incomes, rapid urbanization, evolving dietary preferences favoring increased protein consumption, and strategic government initiatives supporting domestic livestock production. The development of modern retail channels and the growth of the foodservice industry further underpin this sustained market momentum.

According to the Ministry of Agriculture and Environment, in 2025, Vietnam's livestock industry achieved a total meat output of 8.6 million tonnes, including 5.4 million tonnes of pork. A significant challenge impeding market expansion is the persistent threat of animal disease outbreaks, such as African Swine Fever, which can disrupt supply chains and elevate production costs.

Key Market Drivers

Affluence Drives Demand for Quality Meats

The growing affluence of Vietnamese consumers significantly propels the meat market. As incomes increase, households allocate a larger portion of their budgets towards higher-quality food items, including various meat products. This economic upward mobility allows consumers to move beyond basic necessities and seek greater variety and premium options in their diets. According to Sunbytes, in a February 2026 report based on National Statistics Office of Vietnam / GSO data, the average monthly salary in Vietnam for 2026 planning sits around 8.4–8.7 million VND, approximately $323–335 USD. This enhanced purchasing power directly translates into higher demand for fresh, processed, and convenience meat products.

Dietary Shifts Increase Poultry and Beef Share

Evolving dietary preferences, particularly a heightened focus on protein-rich diets, are reshaping consumption patterns within the Vietnam Meat Market. Consumers are increasingly diversifying their meat intake beyond traditional pork, incorporating more poultry and beef into their meals. This shift is driven by a greater awareness of nutritional benefits and a desire for diverse culinary experiences. According to a March 2026 report by eFeedLink citing the Department of Livestock Production and Animal Health, poultry meat consumption has increased, ranking second to pork, rising from 21.9 kg to 25.8 kg per person annually. This diversification is also reflected in the broader market, where total meat imports reached 313,070 tonnes valued at $928.83 million in the first four months of 2026.

Download Free Sample Report

Key Market Challenges

ASF Outbreaks Curtail Pork Supply

The persistent threat of animal disease outbreaks, particularly African Swine Fever, significantly impedes the growth of the Vietnam Meat Market. These outbreaks directly result in substantial livestock losses, causing severe disruptions across production and supply chains. For instance, according to the World Organisation for Animal Health, a total of 2,782 African Swine Fever outbreaks were confirmed nationwide in 2025, leading to the culling of over 1.27 million pigs. This massive culling directly reduces the available supply of pork, a primary component of Vietnam's meat consumption, thereby limiting market volume.

Rising Costs and Uncertainty Reduce Domestic Meat Output

Such widespread disease incidence elevates production costs for farmers due to increased biosecurity investments, veterinary care, and the necessity of restocking herds. The uncertainty introduced by frequent outbreaks also affects farmer confidence and investment, particularly among smaller operations less equipped to implement stringent preventative measures. This dynamic ultimately contributes to reduced overall domestic meat output, potentially increasing reliance on imported meat to meet consumer demand and constraining the market's organic expansion.

Key Market Trends

Shift to Modern Retail and Packaged Meats Drives Branded, Traceable Offerings

A significant trend reshaping the Vietnam Meat Market is the accelerating shift towards modern retail channels and packaged meat products. Consumers are increasingly moving away from traditional wet markets to supermarkets, hypermarkets, and convenience stores, driven by enhanced hygiene, quality assurance, and convenience. This transition facilitates the adoption of chilled and frozen packaged meats, offering longer shelf lives and ease of preparation. The expansion of these modern retail formats demonstrates this trend; according to the USDA Foreign Agricultural Service, April 2026, in the 'Food Processing Ingredients Annual' report, WinMart expanded its network to 4,592 outlets in 2025. This channel shift fosters greater demand for branded and traceable products, as consumers seek reliability.

Rising Demand for Wholesome, Sustainable, and Organic Meat

Parallel to the retail shift, a burgeoning consumer preference exists for wholesome, sustainable, and organic meat offerings in Vietnam. This trend is fueled by heightened health consciousness and increasing food safety awareness, prompting consumers to seek products with transparent origins and ethical production methods. The emphasis is on attributes such as antibiotic-free, hormone-free, and environmentally friendly sourcing. This demand for higher standards is evident in purchasing behavior; according to the article 'Vietnam's Meat Industry on the Path to Modernization Amid New Consumer Trends', September 2025, 72% of Vietnamese consumers are willing to pay more for products certified under VietGAP or Organic standards. This signals a fundamental change in consumer values.

Segmental Insights

Processed meat growth driven by convenience, rising incomes, and safety standards.

The Processed segment is emerging as the fastest-growing within the Vietnam Meat Market, primarily driven by evolving consumer lifestyles and heightened preferences for convenience. Rapid urbanization and increasingly busy schedules have significantly boosted the demand for ready-to-eat and value-added meat products. Concurrently, rising disposable incomes among the expanding middle-class population enable greater expenditure on these convenient options. Furthermore, growing consumer awareness regarding food safety and quality, coupled with stringent national food safety standards enforced by bodies such as the Ministry of Health and the Ministry of Agriculture and Rural Development, encourages a shift towards trusted, branded processed meat products with transparent traceability. This trend is further supported by innovations in product offerings and the expansion of modern retail channels, enhancing accessibility for consumers seeking quality and ease of preparation.

Regional Insights

Drivers Behind Southern Vietnam's Meat Market Leadership

Southern Vietnam leads the national meat market due to several converging factors. The region, encompassing major urban centers like Ho Chi Minh City and the fertile Mekong Delta, benefits from advanced livestock farming infrastructure and proximity to essential processing facilities. This robust foundation is coupled with favorable climatic conditions conducive to efficient livestock production. Furthermore, high urbanization and rising disposable incomes in Southern Vietnam drive significant consumer demand for diverse meat products, contributing to elevated consumption levels. The region's strategic location also provides advantageous access to key export markets. These elements collectively foster a dynamic market environment, reinforced by established distribution networks and a strong foodservice industry presence.

Recent Developments

-

In September 2025, BAF Vietnam Agriculture JSC announced a significant collaboration with China's Muyuan Foods to establish Vietnam's first high-rise pig farming complex in Tay Ninh province. This substantial USD 454 million project was designed to house 64,000 sows and produce 1.6 million market pigs annually from 2027. The venture, which also included a 600,000-tonne capacity feed plant, was expected to generate USD 378.5 million in annual revenue, aiming to bolster domestic pork supply within the Vietnam Meat Market through advanced, biosecure farming systems.

-

In March 2025, Charoen Pokphand Foods Plc (CPF) reported substantial revenue of THB122 billion ($3.62 billion) from its Vietnam operations in 2024, marking a 5% increase year-on-year. This performance positioned Vietnam as the second-largest contributor to CPF's total global revenue. The growth was largely driven by improved meat prices, particularly for swine, within the Vietnam Meat Market. C.P. Vietnam, a subsidiary, maintained its extensive presence with 21 operational factories, including seven dedicated meat processing plants.

-

In October 2024, Masan MEATLife, a key subsidiary of Masan Group, showcased successful new product launches and an expanded focus on processed meats within the Vietnam Meat Market. The company reported a net profit for the third quarter of 2024, buoyed by a 13.6% year-on-year increase in its meat segment revenue. This growth was attributed to the successful introduction of new brands like Heo Cao Boi and Ponnie, offering products such as pork pie, sausage, pork floss, and dried chicken, which were well-received by consumers.

-

In October 2024, GreenFeed Vietnam demonstrated a strategic move to enhance its breeding capabilities within the Vietnam Meat Market. The company imported over 400 great-grandparent pigs from the US swine industry leader, Pig Improvement Company (PIC), for its newly established breeding center in Quang Tri province during August 2024. This initiative was aimed at improving the quality and productivity of its breeding stock, thereby strengthening its integrated feed-farm-food value chain and promoting more sustainable livestock farming practices across Vietnam.

Key Market Players

- Almarai

- SADAFCO

- NADEC

- Al Rabie

- National Food Industries

- Al Othaim

- Lulu Group

- HyperPanda

- Carrefour

- Bin Dawood

|

By Product

|

By Type

|

By Distribution Channel

|

By Region

|

- Chicken

- Pork

- Frog

- Duck

- Mutton

|

|

- Departmental Stores

- Specialty Stores

- Hypermarket/ Supermarket

- Online and Others (Direct Sellers, General Merchandised Retailers, etc.)

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam Meat Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam Meat Market, By Product:

-

Chicken

-

Pork

-

Frog

-

Duck

-

Mutton

-

Vietnam Meat Market, By Type:

-

Vietnam Meat Market, By Distribution Channel:

-

Departmental Stores

-

Specialty Stores

-

Hypermarket/ Supermarket

-

Online and Others (Direct Sellers, General Merchandised Retailers, etc.)

-

Vietnam Meat Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam Meat Market.

Available Customizations:

Vietnam Meat Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam Meat Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com