Forecast Period | 2026-2030 |

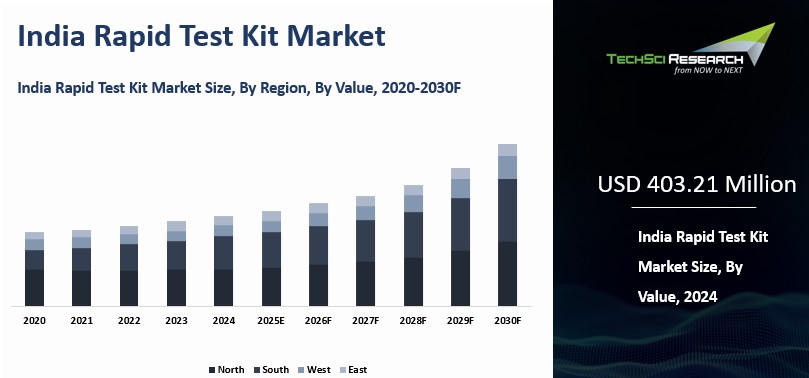

Market Size (2024) | USD 403.21 Million |

Market Size (2030) | USD 604.78 Million |

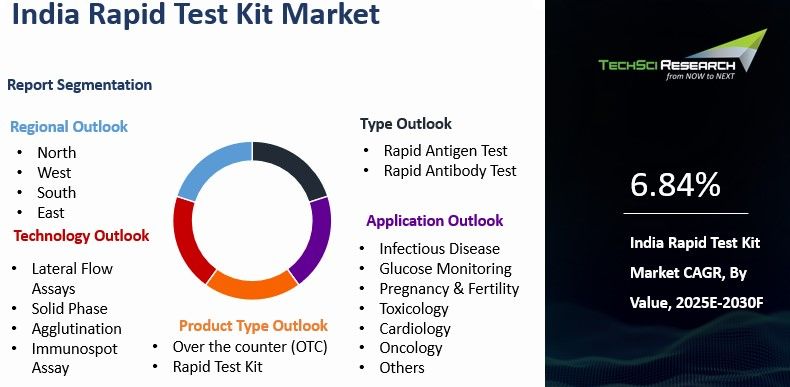

CAGR (2025-2030) | 6.84% |

Fastest Growing Segment | Over the Counter (OTC) |

Largest Market | South India |

Market Overview

India Rapid Test Kit Market was valued

at USD 403.21 Million in 2024 and is expected to

reach USD 604.78 Million by 2030 with a CAGR of 6.84% during the forecast

period.

The India rapid test kit market has grown significantly in recent years, supported by rising demand for quick and accurate diagnostic solutions, particularly following the COVID-19 pandemic. As per the Indian Council of Medical Research (ICMR) report dated May 18, 2023, a total of 169 antigen-based rapid test kits have been validated, including 34 revalidations demonstrating satisfactory performance. These kits, used for detecting infectious diseases, diabetes, and cardiovascular conditions, are widely applied in both clinical and home settings. The market includes antigen, antibody, and molecular diagnostic kits serving diverse healthcare needs.

Growth is supported by increasing disease prevalence, higher health awareness, and government initiatives to improve healthcare access. Regulatory oversight and quality control measures have further strengthened the market framework. However, challenges such as limited awareness in rural areas, regulatory complexities, and counterfeit products persist. Despite these constraints, ongoing research and development efforts aimed at improving accuracy and expanding diagnostic capabilities continue to support the market’s progression within India’s evolving healthcare system.

Download Free Sample Report

Key Market Drivers

Increasing

Demand for Quick Diagnostics

The growing need for fast and reliable diagnostic solutions remains a key driver of the India rapid test kit market, because the country continues to manage a large infectious disease burden while also expanding point-of-care testing across hospitals, clinics, community health centers, and home settings. Rapid test kits are especially valuable in India because they shorten the time between suspicion and confirmation, allowing faster treatment decisions, earlier isolation where needed, and better disease management in locations where full laboratory infrastructure may be limited.

Their relevance became highly visible during the COVID period, but the same advantages continue to apply for malaria and other public health priorities, particularly in remote and underserved areas where decentralized testing can improve access and reduce delays. The market is also supported by stronger awareness of screening and by the need for simple, reliable formats that non-specialist users can adopt more easily than conventional diagnostics. For Instance, WHO reported that India reduced malaria cases by 69 percent and malaria deaths by 68 percent between 2017 and 2023, while Abbott said it had shipped 300 million Panbio rapid antigen tests globally and Mylab’s CoviSelf delivers results in 15 minutes, underscoring how rapid diagnostics support both mass-scale response and timely clinical action.

Technological

Advancements

Technological innovation is another major factor driving growth in the India rapid test kit market, as manufacturers continue to improve the accuracy, speed, usability, and affordability of diagnostic products. Ongoing research and development has enabled faster turnaround times, enhanced sensitivity and specificity, and more user-friendly formats, making rapid test kits more effective in both professional and consumer settings.

Among the notable advancements, microfluidic technology has enabled multiple diagnostic functions to be integrated into compact devices that require smaller sample volumes and deliver quicker results. This not only improves efficiency but also lowers testing costs and expands usability in decentralized and remote healthcare settings. Similarly, nanotechnology has strengthened test performance by enhancing signal detection, particularly in lateral flow assays where materials such as gold nanoparticles are used to improve sensitivity even at low analyte concentrations.

India has also seen notable innovation in disease-specific rapid testing. In addition, advancements in ELISA-based methods, lateral flow immunoassays, and digital health integration are helping improve real-time interpretation and ease of use. The increasing convergence of diagnostics with smartphone platforms and AI-enabled systems is expected to further strengthen the rapid testing landscape in India over the coming years.

Growing

Health Awareness

Rising health awareness among the Indian population is playing an important role in boosting demand for rapid test kits, as consumers are increasingly taking a proactive approach toward prevention, screening, and early diagnosis rather than waiting for advanced symptoms to appear. This shift has been supported by stronger health literacy, urbanization, and easier access to information through public campaigns, hospitals, digital platforms, and community outreach efforts that explain symptoms, risk factors, and the value of timely testing.

Government-led diagnostic expansion has also made testing more visible and acceptable, helping rapid kits gain wider relevance not only for infectious diseases but also for routine screening and decentralized care. The COVID period accelerated this behavior by familiarizing people with self-testing and fast point-of-care diagnostics, which has had a lasting effect on consumer willingness to use convenient rapid kits at home, work, or clinics. For Instance, under the National Programme for NCD prevention and control, India had 707 District NCD Clinics, 268 District Day Care Centres, and 5,541 Community Health Centre NCD Clinics as of December 2022, while Abbott’s Panbio self-test gives results in 15 minutes and is available in packs of 1, 4, 10, and 20 tests, reflecting how awareness and access are jointly expanding rapid test adoption.

Key Market Challenges

Complex

Regulatory Environment

A complex and evolving regulatory framework remains a major challenge for the India rapid test kit market. The approval process for diagnostic products can often be lengthy and resource-intensive, which may delay the launch of new and innovative solutions. Regulatory oversight is primarily managed by the Central Drugs Standard Control Organization (CDSCO), but varying interpretations and limited clarity in some guidelines can create uncertainty for manufacturers operating in this space.

Companies are required to comply with different regulatory standards depending on the test type, intended use, and risk classification of the product. This often involves extensive documentation, validation studies, and quality assurance requirements, all of which can increase time-to-market and overall compliance costs. In a sector where innovation moves quickly, such delays may limit responsiveness to emerging healthcare needs.

These regulatory complexities can also discourage smaller players and new entrants, thereby restricting the diversity of products available in the market. Addressing this challenge will require greater regulatory clarity, more streamlined approval pathways, and stronger alignment between policymakers and industry stakeholders. A more predictable and efficient regulatory environment would help accelerate innovation while ensuring quality and patient safety.

Market

Competition

The India rapid test kit market is highly competitive, with a mix of established diagnostic companies and new entrants competing for market share. This intense competition often leads to aggressive pricing strategies, which can make test kits more affordable but may also place pressure on manufacturers’ margins and product differentiation efforts. In a market where accuracy and reliability are essential, excessive pricing pressure can raise concerns about maintaining consistent quality standards.

Another major concern is the presence of counterfeit and substandard products in circulation. As demand for rapid diagnostics increases, low-quality kits may enter the market, potentially resulting in inaccurate outcomes and increased health risks for users. This not only affects patient trust but can also weaken the credibility of the broader market.

To remain competitive, manufacturers are increasingly focusing on innovation, product design, and advanced technology integration as key differentiators. At the same time, strong quality assurance systems, effective brand positioning, and greater consumer awareness about sourcing genuine products from trusted channels are becoming essential for maintaining long-term confidence in the market.

Key Market Trends

Growing

Adoption in Home Testing

The increasing adoption of home testing is one of the most prominent trends shaping the India rapid test kit market. This shift reflects the broader transition toward personalized, decentralized, and convenience-led healthcare, where consumers prefer diagnostic solutions that are accessible, private, and easy to use. Home-based testing has become especially relevant for conditions such as pregnancy, diabetes, infectious diseases, and general wellness monitoring.

Government support has also contributed to the expansion of decentralized diagnostics. India’s diagnostic infrastructure has strengthened steadily through public health initiatives aimed at improving access to essential tests across primary healthcare settings. As of July 2025, more than 1.78 lakh Ayushman Arogya Mandirs were operational across the country, reflecting the government’s continued emphasis on broader healthcare and diagnostic access.

The COVID-19 pandemic significantly accelerated the uptake of self-testing by familiarizing consumers with the concept of rapid, home-based diagnostics. Since then, home testing has gained wider acceptance due to its convenience, privacy benefits, and ability to reduce dependence on in-person clinical visits. This trend is expected to remain strong as consumers continue to prioritize preventive care and self-monitoring solutions.

Emergence

of E-commerce Platforms

The rise of e-commerce platforms is reshaping the distribution landscape for rapid test kits in India by improving accessibility and purchase convenience. Online channels became especially important during the pandemic, when consumers increasingly relied on digital platforms to buy healthcare essentials without visiting physical stores. This behavior has continued, supported by growing internet penetration and increasing comfort with digital purchasing.

E-commerce platforms now offer a broad range of rapid test kits for various conditions, enabling users to compare products, read specifications, assess reviews, and make informed buying decisions from home. This has expanded access not only in major urban centers but also in semi-urban and underserved areas where physical healthcare retail outlets may be limited. As a result, online distribution is helping bridge gaps in healthcare product availability across regions.

Competitive pricing is another key advantage of online channels, as consumers can compare multiple sellers and benefit from promotional offers and discounts. Customer ratings and reviews further contribute to purchase confidence by offering insights into product usability and reliability. Together, these factors are making e-commerce an increasingly influential channel in the India rapid test kit market.

Segmental Insights

Type Insights

The Rapid Antigen Test segment dominated the India rapid test kit market, primarily due to its ability to deliver results within a short time frame of around 15 to 30 minutes. This fast turnaround makes rapid antigen tests highly suitable for both healthcare providers and consumers, particularly in time-sensitive settings such as hospitals, clinics, emergency screening programs, and public health surveillance initiatives. Their importance became especially evident during the COVID-19 pandemic, when immediate diagnosis was essential for outbreak containment and infection control.

Rapid antigen tests are also generally more affordable than several alternative rapid diagnostic formats, which enhances their accessibility across diverse patient groups and resource-constrained settings. Their cost-effectiveness, ease of use, and scalability have supported widespread deployment in both urban and rural healthcare environments.

In addition, government backing played a critical role in strengthening the segment’s leadership position, particularly through the validation and use of rapid antigen tests in public health programs. This strong alignment between affordability, speed, and policy support has positioned the rapid antigen test segment as a leading component of India’s rapid diagnostics landscape.

Product Type Insights

Based on product type, the Over the Counter (OTC) segment dominated the India rapid test kit market due to its strong consumer accessibility and growing alignment with self-care trends. OTC rapid test kits can be purchased without a prescription, allowing individuals to conduct self-testing for a variety of conditions, including pregnancy, blood glucose monitoring, and certain infectious diseases, from the convenience of their homes. This ease of access has significantly contributed to the segment’s market strength.

Another important factor supporting OTC segment growth is the increasing preference for privacy and convenience. For sensitive conditions, such as sexually transmitted infections, the ability to test discreetly in a personal setting can encourage higher adoption and improve early diagnosis rates. This has made OTC kits particularly relevant in a healthcare environment that increasingly values patient autonomy and preventive action.

The segment also benefits from a broad and expanding product portfolio, which gives consumers access to testing solutions tailored to different health needs. The momentum of home testing, reinforced during the pandemic and sustained by ongoing health awareness, continues to support the dominance of OTC rapid test kits in the Indian market.

Download Free Sample Report

Regional Insights

The southern region of India, particularly states such as Tamil Nadu, Karnataka, and Andhra Pradesh, represents the most dominant regional market for rapid test kits in the country. One of the key reasons for this leadership is the region’s relatively advanced healthcare infrastructure, which includes established hospitals, diagnostic laboratories, medical colleges, and research institutions. This ecosystem has enabled faster adoption and integration of rapid diagnostic technologies across both public and private healthcare settings.

The region has also historically faced a notable burden of infectious diseases, including dengue, tuberculosis, and malaria, which has strengthened demand for quick and efficient diagnostic solutions. In addition, proactive healthcare initiatives and state-level government efforts aimed at improving disease detection and outbreak response have supported wider deployment of rapid test kits, including in underserved areas.

Growing public awareness around early diagnosis and preventive healthcare has further contributed to regional demand. As consumers in southern India become more informed and proactive about health monitoring, the region is likely to maintain its strong position in the India rapid test kit market over the forecast period.

Recent Developments

- In April 2025, India launched two indigenously developed HPV test kits for cervical cancer screening Truenat HPV-HR Plus from Molbio Diagnostics and Patho Detect from Mylab Discovery Solutions after successful evaluation by AIIMS Delhi doctors and other institutions. This was a significant product-launch development because the kits were designed to improve access to affordable, locally made screening tools for cervical cancer, one of the most common cancers affecting Indian women.

- In March 2026, the Technology Development Board under the Department of Science and Technology backed BabyCue Private Limited in Cuttack for the development and commercialization of DiaCue, an indigenous rapid diagnostic platform for childhood diarrhea. The platform was presented as a rapid, non-invasive, and cost-effective point-of-care solution capable of differentiating bacterial from non-bacterial diarrhea, making it a meaningful innovation for primary care and rural health settings where quick treatment decisions are critical.

- In March 2026, TDB-DST supported Chennai-based Acrannolife Genomics for indigenous manufacturing of advanced IVD diagnostic kits at scale. This was an important manufacturing-led development for India’s rapid and point-of-care diagnostics ecosystem because the facility was intended to strengthen domestic capacity for products such as tuberculosis diagnostics and reduce dependence on imported technologies.

- In January 2025, SD BIOSENSOR’s Ultra Covi-Catch COVID-19 rapid antigen self-test became available on a leading Indian e-commerce pharmacy platform, indicating sustained retail channel access for self-testing kits in early 2025.

- In February 2025, the Indian Council of Medical Research (ICMR) and Central Drugs Standard Control Organisation (CDSCO) closed the public consultation period for national draft standard performance evaluation protocols for dengue and chikungunya rapid diagnostic tests (RDTs), marking a key step toward standardized performance benchmarks for India’s RDT sector.

Key Market Players

- SD Biosensor Healthcare Pvt. Ltd

- J. Mitra & Co. Pvt. Ltd.

- Meril Life Sciences Pvt. Ltd

- Tulip Diagnostics (P) Ltd

- Oscar Medicare Pvt. Ltd.

- Angstrom Biotech Pvt. Ltd.

- Ubio Biotechnology Systems Pvt Ltd

- Mylab Discovery Solutions Pvt. Ltd.

- Alpine Biomedicals Pvt. Ltd.

- Abbott India Limited

|

By Type

|

By Product Type

|

By Technology

|

By Application

|

By Region

|

- Rapid Antigen Test

- Rapid Antibody Test

|

- Over the counter (OTC)

- Rapid Test Kit

|

- Lateral Flow Assays

- Solid Phase

- Agglutination

- Immunospot Assay

|

- Infectious Disease

- Glucose Monitoring

- Pregnancy & Fertility

- Toxicology

- Cardiology

- Oncology

- Others

|

|

Report Scope:

In

this report, the India Rapid Test Kit Market has been segmented into the following

categories, in addition to the industry trends which have also been detailed

below:

- India Rapid Test Kit Market, By

Type:

o

Rapid Antigen Test

o

Rapid Antibody Test

- India Rapid Test Kit Market, By

Product Type:

o

Over the counter (OTC)

o

Rapid Test Kit

- India Rapid Test Kit Market, By

Technology:

o

Lateral Flow Assays

o

Solid Phase

o

Agglutination

o

Immunospot Assay

- India Rapid Test Kit Market, By

Application:

o

Infectious Disease

o

Glucose Monitoring

o

Pregnancy & Fertility

o

Toxicology

o

Cardiology

o

Oncology

o

Others

- India Rapid Test Kit Market, By

Region:

o

North

o

South

o

West

o

East

Competitive

Landscape

Company

Profiles: Detailed analysis of the major companies present

in the India Rapid Test Kit Market.

Available

Customizations:

India

Rapid Test Kit Market report with the given market data, TechSci

Research offers customizations according to a company's specific needs. The

following customization options are available for the report:

Company

Information

- Detailed

analysis and profiling of additional market players (up to five).

India

Rapid Test Kit Market is an upcoming report to be released soon. If you wish an

early delivery of this report or want to confirm the date of release, please

contact us at sales@techsciresearch.com