Market Overview

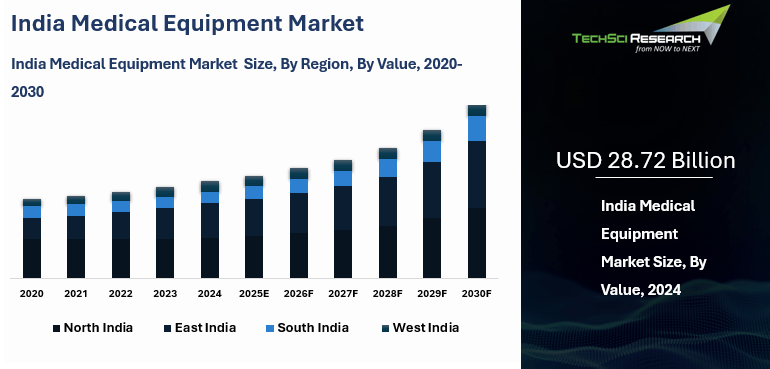

India Medical Equipment Market was valued at USD 28.72 billion in 2024 and is expected to reach USD 46.87 billion by 2030 with a CAGR of 8.65% during the forecast period.

|

Forecast

Period

|

2026-2030

|

|

Market

Size (2024)

|

USD

28.72 Billion

|

|

Market

Size (2030)

|

USD

46.87 Billion

|

|

CAGR

(2025-2030)

|

8.65%

|

|

Fastest

Growing Segment

|

Hospitals

& Clinics

|

|

Largest

Market

|

West India

|

Medical equipment, also known as medical devices, includes any instrument, appliance, software, or material used alone or in combination for diagnostic or therapeutic purposes. These devices help identify, prevent, monitor, treat, or alleviate diseases and injuries, ranging from basic tools like thermometers to advanced systems such as MRI machines and pacemakers.

The medical equipment market is a rapidly expanding sector covering the production, sales, and distribution of a wide range of healthcare technologies. This includes diagnostic devices, surgical instruments, imaging systems, and therapeutic equipment. Growth in the market is driven by continuous technological advancements and the rising need for improved patient care and clinical outcomes.

Overall, medical equipment plays a vital role in enabling healthcare professionals to deliver efficient, accurate, and high-quality treatment, enhancing patient well-being and quality of life.

Download Free Sample Report

Key Market Drivers

Growing Geriatric Population

- India’s growing geriatric population is becoming a powerful demand engine for the India medical equipment market because longer life expectancy and a higher burden of chronic illness are increasing the need for diagnostics, implants, monitoring systems, mobility aids, rehabilitation tools, and home healthcare devices across hospitals, clinics, and residential care settings.

- The demographic shift is large enough to create long-term structural demand for elder-focused medical technologies. In 2022, India had 149 million people aged 60 and above, accounting for about 10.5 percent of the population, and this share is projected to rise to 20.8 percent with 347 million older adults by 2050, which will intensify demand for cardiac care devices, orthopedic implants, rehabilitation products, and home-use monitoring equipment.

- This demand is being reinforced by broader healthcare capacity expansion in India, as major hospital groups are building more advanced infrastructure and the system is preparing for greater treatment volumes. The United States International Trade Administration notes that imports are rising as groups such as Apollo, Fortis, Max, and Hinduja expand high-end facilities, while medical tourism contributes $9 billion to the healthcare market and India may require up to 1.75 million additional hospital beds by the end of 2025.

- Industry growth is already visible in company performance, showing that manufacturers are scaling in line with rising domestic demand. For instance, Poly Medicure reported FY2025 revenue from operations of "Rs " 1,669.8" crore" , while ICRA said Trivitron Healthcare recorded consolidated revenue of "Rs " 489.8" crore" in FY2025, indicating expansion in medical technologies relevant to aging care.

Rising Prevalence of Chronic Diseases

- The rising prevalence of chronic diseases such as cardiovascular disorders, diabetes, cancer, and chronic respiratory conditions is a major force driving the India medical equipment market because these illnesses require continuous screening, diagnosis, treatment, and long-term follow-up through hospitals, diagnostic centers, outpatient clinics, and increasingly home-care environments.

- India’s Ministry of Health and Family Welfare states that non-communicable diseases account for 63 percent of all deaths in the country, with cardiovascular diseases contributing 27 percent of overall mortality, chronic respiratory diseases 11 percent, cancers 9 percent, and diabetes 3 percent. This clearly shows how the disease burden is shifting toward conditions that depend heavily on sustained medical intervention and device-led care.

- The same government guidelines report 54.5 million cardiovascular disease cases, 65 million diabetes cases, and 13.92 lakh cancer cases in India, which is steadily increasing demand for glucose monitoring systems, insulin delivery devices, pacemakers, infusion systems, diagnostic imaging equipment, and other advanced medical technologies that support earlier detection and better disease management.

- Global medtech performance also reflects the scale of demand in chronic care device categories that align closely with India’s needs. For instance, Abbott reported $2.0 billion in fourth-quarter 2025 sales from continuous glucose monitors worldwide, underscoring how major medical technology companies are scaling around regular monitoring tools relevant to India’s growing burden of long-duration diseases.

- As India continues to face more lifestyle-linked illnesses and a larger population living with chronic conditions, the need for reliable, accessible, and innovative medical equipment is expanding. This creates stronger opportunities for manufacturers while also improving treatment access, clinical outcomes, monitoring continuity, and long-term patient quality of life across the healthcare system.

Increased Demand for High-Quality Patient Care

- The rising demand for high-quality patient care in India is becoming a strong catalyst for medical equipment adoption because hospitals and diagnostic centers are under increasing pressure to deliver faster, more precise, and more dependable treatment across imaging, critical care, oncology, surgical support, and patient monitoring applications in both public and private healthcare settings.

- This quality-driven shift is encouraging deeper investment in advanced technologies and domestic manufacturing, supported by the National Medical Devices Policy 2023, which emphasizes access, affordability, quality, innovation, streamlined regulation, skills development, and a stronger manufacturing ecosystem. These priorities are helping create a more supportive environment for higher-value medical equipment deployment in India.

- Government support is also reinforcing this trend through medical device parks and common infrastructure that improve testing, validation, and product development capabilities. The Andhra Pradesh MedTech Zone has built specialized laboratories and testing centers covering biomaterial testing, EMI and EMC testing, electrical safety, 3D printing, lasers, and MRI superconducting magnet capabilities, strengthening India’s quality assurance and innovation base.

- Major industry investments show that companies are aligning their expansion strategies with India’s rising expectations for advanced care delivery. For instance, Wipro GE Healthcare announced an investment of over "INR " 8,000" crores" in manufacturing output and local R&D over the next five years, including Made in India PET CT systems, CT platforms, and MR coils, reflecting strong confidence in long-term demand for dependable patient care technologies.

- As health awareness increases and care delivery becomes more technology intensive, this combination of patient expectations, industrial investment, and policy support is improving treatment quality, raising healthcare efficiency, and steadily strengthening India’s position as an emerging hub for medical device innovation, manufacturing, and advanced clinical care.

Need For Early Disease Detection and Prevention

- The growing focus on early disease detection and prevention in India is creating strong demand for advanced medical equipment because the country’s healthcare system is increasingly prioritizing timely diagnosis, screening, and early intervention to reduce long-term complications, improve outcomes, and manage the heavy burden of non-communicable diseases more efficiently.

- The National Programme for Prevention and Control of Non-Communicable Diseases states that non-communicable diseases account for 63 percent of all deaths in India, with cardiovascular diseases responsible for 27 percent, chronic respiratory diseases 11 percent, cancers 9 percent, and diabetes 3 percent. This makes early-stage diagnosis and preventive care a much more urgent national healthcare priority.

- Government data showing 54.5 million cardiovascular disease cases and 65 million diabetes cases in India is increasing the need for portable ECG systems, glucose monitoring devices, spirometers, imaging platforms, screening tools, and other technologies that support routine testing, risk detection, earlier diagnosis, and continuous monitoring across both institutional and community care settings.

- Digital integration is further strengthening this shift by bringing more intelligent diagnostic tools into the market. Philips said its AI-enabled CT 5300 system introduced in India is designed for diagnosis, interventional procedures, and screening while improving diagnostic precision and workflow efficiency, highlighting how smart imaging is supporting earlier and more accurate clinical decision-making.

- Policy backing is also accelerating adoption through the National Medical Devices Policy 2023, which prioritizes access, affordability, quality, innovation, manufacturing, and skill development to build a stronger ecosystem for advanced medical technologies. For instance, Wipro GE Healthcare announced an investment of over "INR " 8,000" crores" in manufacturing output and local R&D over five years, including Made in India PET CT systems, CT platforms, and MR coils, illustrating how major companies are expanding diagnostic capacity in line with India’s preventive care agenda.

Key Market Challenges

Strict Regulatory Policies

- Strict regulatory policies remain a major challenge for the India medical equipment market because device manufacturers must comply with the Medical Devices Rules 2017, product classification requirements, licensing procedures, audits, labeling rules, and post-market obligations before scaling products nationally. While these controls are intended to improve patient safety and product quality, they can still slow commercialization and raise execution complexity.

- The compliance burden can significantly increase operating costs and create planning uncertainty for both domestic manufacturers and foreign medical device companies seeking to launch products or expand portfolios in India. This challenge is especially difficult for smaller firms and startups, which often lack the in-house regulatory, legal, and documentation infrastructure needed to manage detailed dossiers, respond quickly to regulator queries, and navigate state-level interpretation differences.

- Bureaucratic procurement systems add another layer of challenge because public-sector adoption of newer technologies can remain slow even after regulatory approval has been secured. Lengthy review cycles, tender procedures, and administrative formalities can delay commercial uptake and weaken go-to-market momentum for innovative products. For instance, India’s medical device approval pathway allows a target review timeline of up to 9 months for import applications, and applicants generally must respond to regulator queries within 45 days or risk having the application treated as withdrawn.

Uncertainty in Reimbursement

- Uncertainty in reimbursement remains a significant obstacle for the India medical equipment market because hospitals and device suppliers continue to operate in an environment where cost control often outweighs structured value-based evaluation. Weakly defined coverage pathways, inconsistent review timelines, and limited payment clarity can reduce confidence in the commercial viability of advanced medical technologies and slow their broader adoption.

- This makes healthcare providers more hesitant to invest in newer devices, especially when payment recovery is unclear, delayed, or not aligned with the clinical outcomes and operational benefits those technologies can deliver. Manufacturers face the same difficulty because without a transparent and predictable reimbursement framework, it becomes harder to forecast product adoption, build pricing strategies, and justify investments in localization, physician training, and long-term market development.

- The problem is further amplified by fragmentation between public and private stakeholders, limited use of formal health technology assessment frameworks, and the absence of a regularly updated review mechanism that can keep pace with innovation across multiple specialties. This creates a difficult environment for market access planning and reimbursement navigation. For instance, L.E.K. Consulting noted that India’s reimbursement pathway has to deal with more than 1,000 health benefit packages across 24 specialties without a documented annual or fixed-interval review process, highlighting the complexity and fragmentation of device reimbursement in India.

Key Market Trends

Increasing Acceptance of Refurbished Medical Equipment

- The increasing acceptance of refurbished medical equipment is becoming an important demand driver in the India medical equipment market because many hospitals, diagnostic centers, and smaller healthcare providers need dependable technology but remain constrained by limited capital budgets, high equipment costs, and long replacement cycles.

- Refurbished medical systems help bridge this affordability gap by giving healthcare providers access to imaging and diagnostic equipment at a lower upfront cost while still offering acceptable clinical performance, serviceability, and operational utility. This makes them especially relevant for budget-conscious institutions trying to expand capacity without large capital expenditure.

- The trend also aligns with the practical realities of India’s healthcare system, where extending diagnostic reach and improving service availability often matter more than installing the newest generation of equipment in every facility. In many settings, functional and reliable technology is more valuable than premium innovation alone.

- Buyer confidence has improved because established manufacturers now position refurbished medical equipment as certified, quality-checked, and warranty-backed offerings rather than informal second-hand purchases. This shift reduces hesitation, improves trust, and makes refurbished devices a more strategic solution for balancing affordability, access, and sustainability in Indian healthcare delivery. For instance, GE HealthCare says its refurbished equipment business has more than 20 years of experience and has sold over 18,000 systems globally, while its CT refurbishment and validation process involves more than 100 labor hours and 400 steps.

Increase Accessibility in Rural Areas

- Improving healthcare accessibility in rural India is steadily increasing demand in the India medical equipment market because the expansion of primary care infrastructure, decentralized diagnostics, and digital health services requires a broader installed base of medical devices across village-level and district-level healthcare facilities.

- As healthcare delivery moves closer to communities, demand is rising not only for basic diagnostic and monitoring devices but also for telemedicine-linked tools that support screening, consultation, referral, and follow-up beyond traditional urban hospitals. This is expanding the practical use case for portable, connected, and entry-level clinical equipment.

- This shift is especially important in India because rural patients often face major barriers related to travel distance, treatment delays, limited specialist availability, and lower continuity of care. In such settings, the local availability of functional medical equipment becomes essential for early disease detection, timely intervention, and ongoing patient management.

- Government initiatives are reinforcing this trend by upgrading frontline health centers and linking them with remote consultation networks, which increases equipment needs across underserved geographies. For instance, the government’s eSanjeevani platform had delivered 8 crore teleconsultations by December 2022 through 109,748 Ayushman Bharat Health and Wellness Centres linked to 14,188 hubs, showing how rural care expansion is directly creating sustained demand for medical equipment and digital health support tools.

Segmental Insights

Type Insights

Based on type, in India’s medical equipment market, diagnostic

imaging equipment dominates due to rising demand for early and accurate

disease detection. The growing prevalence of chronic conditions such as

cardiovascular diseases, cancer, and respiratory disorders has intensified the

need for advanced diagnostic tools.

An aging population further drives the segment, as

early detection and monitoring of age-related diseases become essential. Technological

innovations including 3D imaging, artificial intelligence, and molecular

imaging have improved diagnostic precision, patient comfort, and efficiency.

Additionally, government initiatives and funding to

enhance early disease detection and equip healthcare facilities with modern

imaging systems have strengthened market growth. Overall, diagnostic imaging

remains the leading segment, supported by technological progress, demographic

trends, and government support.

End User Insights

Based on End User, Hospitals and clinics represent

the fastest-growing end-user segment in India’s medical equipment market. The

surge in chronic diseases, coupled with rapid urbanization and expanding

healthcare infrastructure in major cities, has increased the need for advanced

diagnostic and treatment equipment.

Government programs such as the National Health Mission and Ayushman

Bharat have improved access to modern equipment, especially in rural and

underserved regions. The rapid expansion of private healthcare, rising

disposable incomes, and growing public-private collaborations further

accelerate equipment adoption. These factors collectively position hospitals and clinics as

the key growth drivers of India’s medical equipment market.

Download Free Sample Report

Regional Insights

The West region of India, with a particular focus

on Mumbai and its surrounding areas, has emerged as a dominant force in the

Indian Medical Equipment Market. The western region of India, particularly Mumbai and its adjoining areas, has established itself as a major hub in the Indian medical equipment market. This prominence is largely driven by the region's strong healthcare infrastructure, which includes advanced hospitals, cutting-edge research centers, and a pool of skilled medical professionals. Also, the high patient density in the area has created sustained demand for modern medical technologies and equipment.

Both government and private sector investments have further accelerated growth, making the region a hotspot for healthcare innovation. Mumbai, being a financial and commercial capital, also provides strategic advantages such as connectivity, logistics, and access to capital, enhancing its appeal to domestic and global players. As a result, the western region not only supports the growing healthcare needs of the population but also plays a key role in shaping the future of India's medical technology landscape.

Recent Developments

- In August 2025, OIC International, Medi Mold, and Fives AddUp partnered to launch a 3D-printing hub for orthopaedic implants in India. Express Healthcare reported that the collaboration was designed to build India into a manufacturing base for high-performance implants using additive manufacturing, with OIC introducing implants produced in India through proprietary 3D-printing technology. The partners said the approach could reduce post-surgery recovery time, lower costs, and support large-scale local production for both domestic and global markets, making it a significant medical-equipment innovation story.

- In August 2025, Healthium Medtech and C-CAMP launched an innovation program focused on surgical and medical technologies in India. According to Express Healthcare, the initiative was intended to support deep-science startups building digitally enabled, affordable, and clinically relevant technologies, while giving them access to mentoring, validation pathways, and commercialization support. This was an important collaboration in the medical-equipment ecosystem because it connected an established medtech manufacturer with a startup and innovation platform to accelerate device development.

- In August 2025, US-based Vyome signed an MoU with Embryyo, an Indian medical-device innovation studio, to work on advancing medical technology development. BioSpectrum India identified the deal as a formal partnership between a global player and an Indian innovation-focused medtech platform, underscoring the growing role of India in device co-development and commercialization partnerships. Although the visible excerpt is brief, it clearly qualifies as a collaboration-led development in India’s medical-equipment space.

- In December 2025, BPL Medical Technologies launched a new range of critical-care devices at ISACON 2025, including the ExcelSign E12 and E17 modular patient monitors, the Relife 1000 biphasic defibrillator, and new OT charting software. The company said these products were built to strengthen preparedness across intensive care units, operating rooms, and emergency departments, combining bedside equipment with digital workflow support. This was a notable product launch for India’s medical-equipment market because it expanded locally relevant critical-care hardware and software solutions in one coordinated rollout.

Key Market Players

- Philips India Ltd.

- India

Medtronic Pvt. Ltd.

- Wipro GE

Health Care Limited

- Johnson

and Johnson Ltd

- B. Braun

India

- Baxter

Inia Pvt Ltd

- Becton

Dickinson India Pvt Ltd.

- Abbott

India Ltd

- Robert

Bosch India Limited

- 3M India

Limited

|

By

Type

|

By

End User

|

By

Region

|

- Cardiovascular Devices

- Diagnostic Imaging

equipment

- In-vitro Diagnostic Devices

- Ophthalmic Devices

- Diabetes Care Devices

- Dental Care Devices

- Surgical Equipment

- Patient Monitoring Devices

- Orthopedic Devices

- Nephrology & Urology

Devices

- Others

|

- Hospitals & Clinics

- Diagnostic Centers

- Others

|

|

Report Scope:

In this report, the India Medical Equipment Market has

been segmented into the following categories, in addition to the industry

trends which have also been detailed below:

- India Medical Equipment Market, By Type:

o Cardiovascular Devices

o Diagnostic Imaging

equipment

o In-vitro Diagnostic Devices

o Ophthalmic Devices

o Diabetes Care Devices

o Dental Care Devices

o Surgical Equipment

o Patient Monitoring Devices

o Orthopedic Devices

o Nephrology & Urology

Devices

o Others

- India Medical Equipment Market, By End User:

o Hospitals & Clinics

o Diagnostic Centers

o Others

- India Medical Equipment Market, By Region:

o North

o South

o West

o East

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the India Medical

Equipment Market.

Available Customizations:

India Medical Equipment Market report with

the given market data, TechSci Research offers customizations according to a

company's specific needs. The following customization options are available for

the report:

Company Information

- Detailed analysis and profiling of additional

market players (up to five).

India Medical Equipment Market is an upcoming

report to be released soon. If you wish an early delivery of this report or

want to confirm the date of release, please contact us at sales@techsciresearch.com