Forecast Period | 2026-2030 |

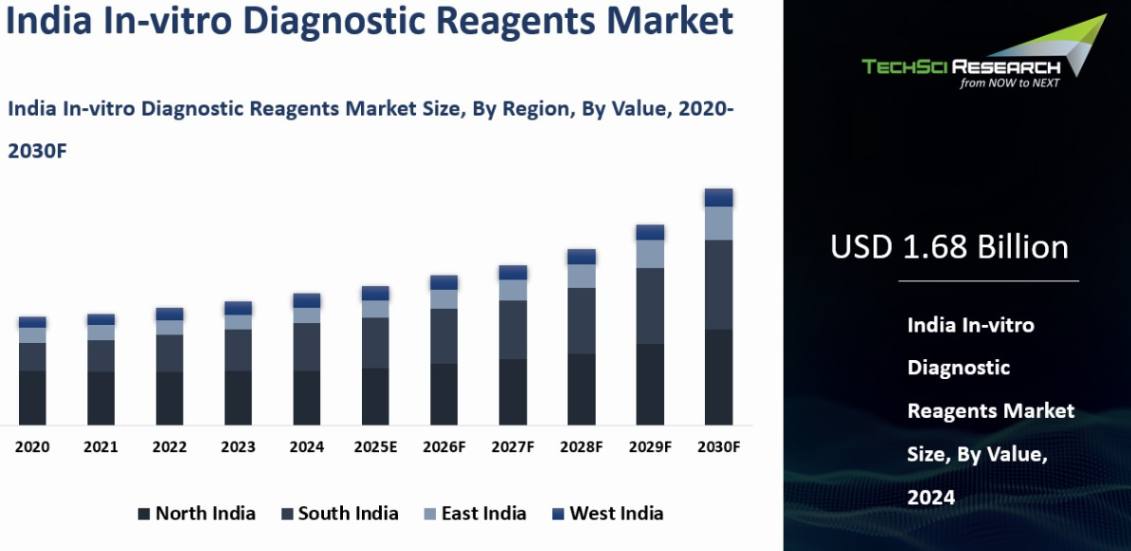

Market Size (2024) | USD 1.68 Billion |

Market Size (2030) | USD 2.30 Billion |

CAGR (2025-2030) | 6.55% |

Fastest Growing Segment | Clinical Chemistry |

Largest Market | North India |

Market Overview

India In-vitro Diagnostic Reagents Market was valued at USD 1.68 billion in 2024 and is anticipated to reach USD 2.30 Billion by 2030, with a CAGR of 6.55% during 2025-2030.

The Indian In-vitro Diagnostic (IVD) Reagents market is witnessing substantial growth and evolution, propelled by technological advancements, heightened healthcare awareness, and a surge in chronic disease cases. The market's future appears bright, with continuous innovations in diagnostic technologies and escalating healthcare investments. The increasing emphasis on personalized medicine and the emergence of novel biomarkers are poised to unlock new growth opportunities. Furthermore, the COVID-19 pandemic has underscored the critical role of diagnostics, paving the way for sustained investment and innovation in this sector.

Key Market Drivers

Technological Advancements

Technological advancements are a powerful growth driver for India’s IVD reagents market because they are making diagnostics faster, sharper, and more scalable across both high end reference laboratories and broader care networks, with Indian diagnostic chains increasingly using molecular genomics, next generation sequencing, artificial intelligence, digital pathology, and intelligent real time information systems to improve turnaround time, support clinical decision making, and strengthen the shift from basic testing toward precise and clinically differentiated detection of infectious disease, cancer, and other complex conditions.

For instance, Metropolis Healthcare stated that its Innovation Cell integrated molecular genomics, artificial intelligence, and next generation sequencing into its test portfolio and launched more than 100 advanced tests in FY 2023-24, while the company operated 199 clinical laboratories, more than 4,150 service points, and a presence in over 600 towns in India, showing that advanced testing is no longer limited to a handful of elite urban centres but is being operationalized at meaningful scale through large organized players.

This matters directly for reagent demand because every expansion in automated workflows, specialized assay menus, accredited processing, and digitally enabled reporting increases the need for dependable consumables that can support higher throughput and more sophisticated test formats, and Metropolis also reported a CAP proficiency score of over 98 percent for the past decade and more than 75 percent of reports generated by accredited labs, reinforcing how technology adoption in India is being tied to quality assurance rather than only to speed or convenience.

Rising Prevalence of Chronic Diseases

The rising prevalence of chronic diseases is a major driver of India’s IVD reagents market because the country is dealing with a large and persistent burden of diabetes, prediabetes, obesity, cardiovascular risk, and other long duration conditions that require repeated screening, diagnosis, and monitoring rather than one time intervention, with ICMR noting that its INDIAB study covered 30 states and union territories and 113,106 individuals and found diabetes prevalence at 9.6 percent, while a later national analysis published in Nature reported diabetes at 11.4 percent, prediabetes at 15.3 percent, generalized obesity at 28.6 percent, abdominal obesity at 39.5 percent, and non communicable diseases accounting for 6.3 million deaths or 68 percent of all deaths in India.

For instance, Metropolis Healthcare reported 12 million patient volumes in FY 2023-24 and said its portfolio includes more than 4,000 tests and profiles along with wellness offerings specifically curated for screening lifestyle and chronic diseases, which illustrates how organized Indian labs are increasingly built around recurring demand for glucose assessment, blood chemistry analysis, lipid risk evaluation, pathology review, and other routine or specialized monitoring needs associated with chronic illness.

As chronic disease management becomes more continuous and protocol driven, the consumption of IVD reagents rises in tandem because clinicians and patients depend on repeat testing to track progression, treatment response, and early risk signals, and this creates durable volume growth for laboratories that can combine routine panels with specialized diagnostics across wide national service networks rather than relying only on episodic testing demand.

Growing Healthcare Awareness

Growing healthcare awareness is accelerating India’s IVD reagents market because preventive testing is becoming more visible within public health delivery, primary care outreach, and population level screening efforts, with the Ministry of Health and Family Welfare framing early detection as a core part of Ayushman Bharat and the National Programme for Prevention and Control of Non Communicable Diseases, while the country has also expanded the delivery backbone through 770 District NCD Clinics, 364 District Day Care Cancer Centres, and 6,410 NCD clinics at Community Health Centres to support screening, diagnosis, referral, treatment, and health promotion.

For instance, the Government of India launched an intensified special NCD screening campaign from 20 February to 31 March 2025 to achieve 100 percent screening of all individuals aged 30 years and above for diabetes, hypertension, and three common cancers, and by 31 October 2025 the NP-NCD portal had recorded 38.79 crore hypertension screenings, 36.05 crore diabetes screenings, 31.88 crore oral cancer screenings, 14.98 crore breast cancer screenings, and 8.15 crore cervical cancer screenings at sub centres, primary health centres, and Ayushman Arogya Mandirs.

This scale of screening shows that awareness in India is no longer confined to messaging alone but is increasingly translating into actual diagnostic utilization, and when more people accept regular checkups, risk assessment, and earlier testing as part of normal healthcare behaviour, demand for IVD reagents strengthens steadily across public programs, organized diagnostic chains, and referral laboratory networks.

Download Free Sample Report

Key Market Challenges

Regulatory Hurdles and Compliance Issues

The regulatory landscape for IVD reagents in India is intricate and often perceived as cumbersome. The Central Drugs Standard Control Organization (CDSCO) is the primary regulatory body, and obtaining approvals for new diagnostic products can be a lengthy and complicated process. This complexity can delay the introduction of innovative diagnostic reagents into the market.

Regulatory standards in the IVD sector are continuously evolving to keep pace with advancements in technology and international best practices. While this is necessary for ensuring safety and efficacy, it can pose challenges for manufacturers who must constantly adapt to new regulations. Keeping up with these changes requires significant resources and can be particularly challenging for smaller companies.

Meeting stringent regulatory requirements entails substantial compliance costs. These include expenses related to clinical trials, documentation, and quality assurance. For many local manufacturers, especially small and medium-sized enterprises (SMEs), these costs can be prohibitive, limiting their ability to compete with larger, well-funded multinational companies.

High Costs of Advanced Diagnostic Technologies

Advanced diagnostic technologies, such as molecular diagnostics, next-generation sequencing, and high-throughput automated systems, involve high capital and operational expenditures. The costs associated with acquiring and maintaining sophisticated diagnostic equipment and reagents are significant barriers, particularly for healthcare providers in rural and semi-urban areas.

A large segment of the Indian population cannot afford the high costs associated with advanced diagnostic tests. Despite rising incomes and increased healthcare spending, many patients still opt for basic diagnostic services due to financial constraints. This limits the market penetration of high-cost IVD reagents.

In India, the reimbursement landscape for diagnostic tests is not as well-developed as in some Western countries. The lack of comprehensive insurance coverage for advanced diagnostic tests means that patients often have to pay out-of-pocket, further restricting the demand for expensive IVD reagents. Without sufficient reimbursement mechanisms, the uptake of advanced diagnostic technologies remains limited.

Limited Skilled Workforce and Infrastructure

The operation of advanced diagnostic equipment and the interpretation of complex test results require specialized skills. India faces a significant shortage of trained laboratory technicians, pathologists, and other healthcare professionals capable of handling sophisticated IVD technologies. This skills gap hinders the adoption and effective use of advanced diagnostic reagents.

While urban areas may have access to state-of-the-art diagnostic laboratories, rural and semi-urban regions often lack adequate infrastructure. Many laboratories in these areas are not equipped with the necessary technology to perform advanced diagnostic tests, limiting the reach and effectiveness of IVD reagents.

Ensuring consistent quality and standardization across diagnostic laboratories is a significant challenge. Variations in laboratory practices, equipment calibration, and reagent quality can lead to discrepancies in test results. This lack of standardization can undermine trust in diagnostic tests and restrict market growth.

Key Market Trends

Integration of Artificial Intelligence and Machine Learning

Artificial Intelligence (AI) and Machine Learning (ML) technologies are being increasingly integrated into diagnostic processes to enhance accuracy and efficiency. AI algorithms can analyze large datasets to identify patterns and anomalies that may be missed by human analysts. This capability is particularly useful in complex diagnostic areas such as oncology and genomics, where precision is critical.

AI and ML can also be used for predictive analytics, enabling the early detection of diseases based on patient data trends. Predictive models can help in identifying individuals at high risk of developing certain conditions, thereby facilitating early intervention and better disease management. This proactive approach to healthcare is expected to drive the demand for IVD reagents used in predictive diagnostics.

The integration of AI and ML in laboratory operations can streamline workflows, reduce turnaround times, and optimize resource utilization. Automated data analysis and reporting can free up healthcare professionals to focus on more complex tasks, improving overall efficiency and increasing the throughput of diagnostic tests. This operational efficiency can boost the demand for IVD reagents as laboratories become capable of handling higher volumes of tests.

Expansion of Point-of-Care Testing (POCT)

Point-of-care testing (POCT) offers rapid diagnostic results at or near the site of patient care, such as in clinics, homes, or remote locations. The convenience and accessibility of POCT make it a valuable tool for improving healthcare delivery, especially in rural and underserved areas. The expansion of POCT is expected to drive the demand for portable and easy-to-use IVD reagents.

POCT allows for immediate clinical decision-making, which is crucial in emergency and critical care settings. The ability to quickly diagnose conditions such as infections, cardiac events, and metabolic disorders can significantly improve patient outcomes. The growing adoption of POCT devices and reagents for such critical applications is a major driver of market growth.

Advances in POCT technology, including the development of miniaturized and multifunctional devices, are expanding the range of tests that can be performed at the point of care. Innovations such as microfluidics, biosensors, and smartphone-based diagnostics are making POCT more accurate, affordable, and user-friendly. These advancements are expected to increase the adoption of POCT and drive the demand for related IVD reagents.

Segmental Insights

Test Type Insights

Based on the category of Test Type,The clinical chemistry segment dominated India’s IVD reagents market in 2024, driven by its broad application in diagnosing and monitoring a wide range of conditions, including metabolic disorders, kidney and liver diseases, lipid levels, and glucose.

These tests are a core part of routine health check-ups and preventive care, leading to high testing volumes. The rising prevalence of chronic diseases such as diabetes, cardiovascular conditions, and kidney disorders further increases the need for regular biochemical testing like blood glucose, lipid profiles, and renal function tests.

Additionally, the growing burden of liver and kidney diseases, which require continuous monitoring through tests such as creatinine and liver function panels, is reinforcing demand. Overall, the high frequency and essential nature of these tests are sustaining the dominance of the clinical chemistry segment in India.

Product Insights

The reagents segment is expected to witness strong growth, driven by its critical role in diagnostic testing. Reagents are essential for detecting and measuring biomarkers in samples such as blood, urine, and tissue, making them indispensable across all diagnostic processes.

Their widespread use across clinical chemistry, hematology, immunology, microbiology, and molecular diagnostics ensures consistent demand. Rising cases of chronic diseases like diabetes, cardiovascular conditions, and cancer, along with infectious diseases such as tuberculosis and COVID-19, are further increasing the need for reagent-based tests.

Additionally, advancements in biotechnology have improved reagent sensitivity and accuracy, while the growing adoption of automated and high-throughput diagnostic systems is driving the need for high-quality, compatible reagents. Overall, these factors are supporting sustained growth of the reagents segment in India.

Download Free Sample Report

Regional Insights

North India emerged as the dominant in the India In-vitro Diagnostics Reagents market in 2024, holding the largest market share in terms of value. North India is home to several major metropolitan cities such as Delhi, Noida, Gurgaon, Chandigarh, and Jaipur. These cities serve as healthcare hubs with a high concentration of hospitals, diagnostic laboratories, and healthcare centers. The presence of these facilities increases the demand for IVD reagents to support a wide range of diagnostic tests.

The region boasts renowned specialty hospitals and medical centers that attract patients from across the country and neighboring regions. These facilities require a constant supply of high-quality IVD reagents for routine diagnostic tests as well as specialized assays in areas like oncology, cardiology, and nephrology. North India has a dense population, including urban centers with a significant demand for healthcare services. The densely populated states of Uttar Pradesh, Punjab, Haryana, and Delhi-NCR collectively contribute to a substantial volume of diagnostic tests, thereby driving the demand for IVD reagents. The region has witnessed significant investments in healthcare infrastructure, including the establishment of new hospitals, clinics, and diagnostic centers. This development has expanded access to healthcare services and increased the utilization of diagnostic tests, supporting the growth of the IVD reagents market.

Recent Developments

- In March 2026, the Technology Development Board under the Department of Science and Technology backed Chennai-based Acrannolife Genomics to establish a manufacturing facility for advanced indigenous IVD diagnostic kits.The project was described as a scale-up effort for the company’s Trunome GrafAssure and TBFYND products, with the stated goal of expanding domestic molecular-diagnostics manufacturing and reducing reliance on imported technologies.

- In November 2025, Servier India launched a biomarker-testing initiative in collaboration with MedGenome and Strand Life Sciences to expand access to molecular diagnostics for acute myeloid leukaemia and cholangiocarcinoma across India. The partners said the program would introduce customized IDH1 and IDH2 biomarker panels at subsidized rates, with free testing in the government sector, making advanced diagnostic reagents and associated testing more accessible in routine oncology care.

- In February 2025, GOQii and Acrannolife Genomics partnered to launch GrafCare, a post-transplant care program that combines Acrannolife’s Trunome genomic diagnostic test with GOQii’s smart vital-monitoring device and AI-led care support. The companies positioned the launch as a precision-diagnostics innovation for organ-transplant recipients, with the Trunome blood test designed to detect early signs of organ rejection or infection and feed actionable insights into a more personalized monitoring pathway.

Key Market Players

- Abbott Laboratories Inc.

- Becton, Dickinson and Company

- F. Hoffmann-La Roche Ltd

- Transasia Bio-Medicals Ltd

- Thermo Fisher Scientific Inc.

By Test Type | By Product | By Usability | By Application | By End User | By Region |

- Clinical Chemistry

- Molecular Diagnostics

- Hematology

- Immuno Diagnostics

- Test Types

| | | - Infectious Disease

- Diabetes

- Cancer/Oncology

- Cardiology

- Autoimmune Disease

- Nephrology

- Other

| - Diagnostic Laboratories

- Hospitals and Clinics

- Other

| - North India

- South India

- East India

- West India

|

Report Scope:

In this report, the India In-vitro Diagnostic Reagents Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

- India In-vitro Diagnostic Reagents Market, By Test Type:

o Clinical Chemistry

o Molecular Diagnostics

o Hematology

o Immuno Diagnostics

o Test Types

- India In-vitro Diagnostic Reagents Market, By Product:

o Instrument

o Reagent

o Other

- India In-vitro Diagnostic Reagents Market, By Usability:

o Disposable

o Reusable

- India In-vitro Diagnostic Reagents Market, By Application:

o Infectious Disease

o Diabetes

o Cancer/Oncology

o Cardiology

o Autoimmune Disease

o Nephrology

o Other

- India In-vitro Diagnostic Reagents Market, By End User:

o Diagnostic Laboratories

o Hospitals and Clinics

o Other

- India In-vitro Diagnostic Reagents Market, By Region:

o North India

o South India

o West India

o East India

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the India In-vitro Diagnostic Reagents Market.

Available Customizations:

India In-vitro Diagnostic Reagents market report with the given market data, Tech Sci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

India In-vitro Diagnostic Reagents Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com