|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 2.21 Billion

|

|

CAGR (2026-2031)

|

5.69%

|

|

Fastest Growing Segment

|

Fitness Equipment

|

|

Largest Market

|

ACT and New South Wales

|

|

Market Size (2031)

|

USD 3.08 Billion

|

Market Overview

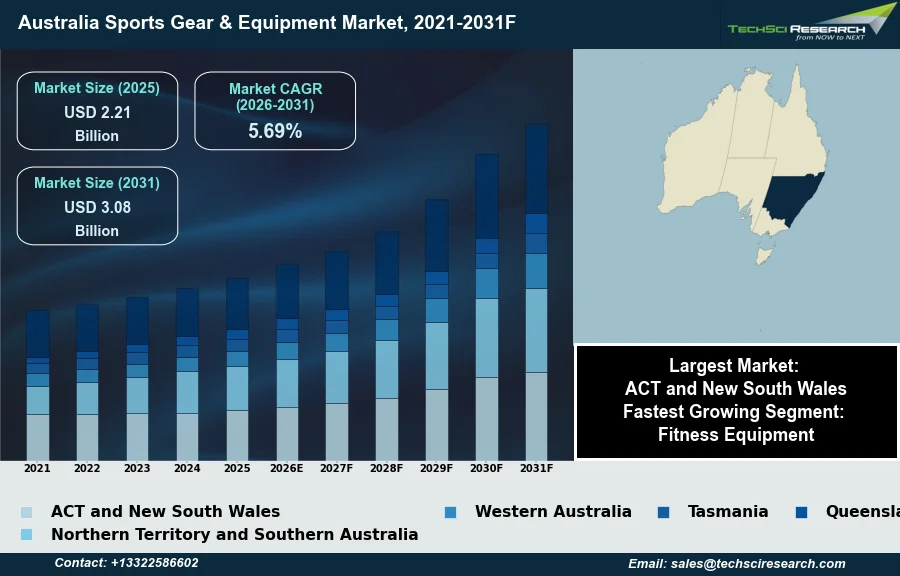

The Australia Sports Gear & Equipment Market will grow from USD 2.21 Billion in 2025 to USD 3.08 Billion by 2031 at a 5.69% CAGR. The Australia Sports Gear and Equipment Market encompasses a diverse range of products, including athletic apparel, footwear, protective equipment, and specialized tools designed for various sports and physical activities. This market's growth is primarily driven by escalating participation rates in sports and fitness across the population, concurrent government initiatives aimed at promoting public health and active lifestyles, and increasing discretionary income among consumers.

According to the AusPlay survey conducted by the Australian Sports Commission and cited by the Australian Institute of Health and Welfare, approximately 19.2 million Australians aged 15 and over participated in sport or physical activity at least once in 2024–25. However, a significant challenge impeding market expansion is the persistent global supply chain disruptions, which can lead to increased operational costs and delayed product availability, thereby affecting consumer access and pricing stability within the Australian market.

Key Market Drivers

Health Awareness Drives Participation and Gear Demand

Increasing health and fitness awareness among the Australian populace is a primary driver for the Sports Gear and Equipment Market, directly correlating with rising participation in various physical activities. This heightened consciousness leads consumers to invest in specialized gear and apparel that support their active lifestyles. For example, according to Football Australia's 2025 National Participation Report, released in February 2026, 1.93 million Australians participated in football across clubs, schools, social formats, futsal, and inclusion programs in 2025, underscoring a significant engagement in organized sports. This broad engagement drives demand for items such as athletic footwear, team uniforms, and protective equipment tailored to specific sports.

Online Retail Expansion Driving Accessibility and Sales Growth

The expansion of online retail channels further influences the Australia Sports Gear and Equipment Market by enhancing product accessibility and consumer purchasing options. Digital platforms provide a convenient avenue for consumers to explore a wide array of products, from niche equipment to mainstream athletic wear. This channel growth is evidenced by Super Retail Group's fiscal first half report, issued in February 2026, which stated that Rebel Sports, a leading Australian specialty sporting goods retailer, saw its online sales increase by 5.9 percent year-over-year to A$146.3 million in the fiscal half ended December 31, 2025, constituting 19.8 percent of its total sales. Overall, Super Retail Group reported total group sales of A$2.2 billion for the fiscal first half ended December 31, 2025, marking a 4.2 percent increase from the prior-year period, reflecting a resilient market performance.

Download Free Sample Report

Key Market Challenges

Global Supply Chain Disruptions Elevate Costs and Delay Availability

A significant challenging factor impeding the expansion of the Australia Sports Gear and Equipment Market is the persistent global supply chain disruptions. These disruptions directly lead to increased operational costs for businesses involved in manufacturing and distributing sports equipment and can result in delayed product availability for consumers. The reliance on international sourcing for raw materials, components, and finished goods means that global logistical issues, such as shipping delays and freight cost volatility, disproportionately affect the Australian market.

Cost Pressures and Delays Push Up Prices and Damp Demand

For instance, according to the Australian Industry Group, in early 2026, 47% of Australian industrial businesses experienced supply chain disruptions, with 81% of those businesses reporting increased costs as the leading impact. Such elevated costs ultimately translate into higher retail prices for athletic apparel, footwear, and specialized equipment, potentially reducing consumer purchasing power and dampening overall market demand. Furthermore, prolonged delays in product delivery can lead to stock shortages, impacting sales opportunities and consumer satisfaction.

Key Market Trends

Technological Integration and Investment in Australian Sports Gear

Increasing Technological Integration in Sports Equipment significantly influences the Australia Sports Gear & Equipment Market. This trend incorporates advanced electronics, sensors, and innovative materials into athletic apparel, footwear, and specialized gear. Such integration enhances user performance, provides real-time feedback, and aids in injury prevention. This caters to athletes and enthusiasts seeking data-driven insights and a competitive edge, driving demand for premium products. According to Teamworks, a technology provider, in its February 2025 report titled "Powering Performance: Australia's Bold Investment in Sports Technology for Olympic Success," the Australian Sports Commission committed $385 million in high-performance sports over 18 months, with technology identified as a key component for athlete performance.

Sustainable and Eco-Friendly Sports Gear Demand

Another prominent trend shaping the Australian market is the Growing Demand for Sustainable and Eco-Friendly Products. Consumers increasingly prioritize environmental responsibility, leading to a rising preference for sports gear and equipment manufactured using sustainable practices and materials. This includes products from recycled plastics, organic cotton, or ethical supply chains. Brands are investing in innovative manufacturing and transparent sourcing to meet these expectations, driving product differentiation. For example, according to Scimex, reporting on new Swinburne research in November 2025, 57% of Australians expressed a willingness to pay more for clothing made from natural fibres, indicating a strong market pull.

Segmental Insights

Wellness-Driven Growth Fueled by At-Home Fitness and Smart Technology

The Fitness Equipment segment is currently the fastest-growing area within the Australia Sports Gear & Equipment Market, reflecting a significant shift in consumer priorities and lifestyle trends. This rapid expansion is primarily driven by escalating health and wellness awareness among the Australian populace, fostering a greater demand for versatile fitness solutions. Furthermore, the increasing preference for convenient, home-based workouts and personalized fitness experiences, coupled with advancements in smart fitness technology, significantly fuels the segment's growth. This allows individuals to integrate exercise seamlessly into their daily routines, promoting sustained engagement with physical activity.

Regional Insights

ACT and NSW: Regional Leaders Driving Sports Gear Demand

The Australian Capital Territory and New South Wales emerge as key regional contributors to Australia's sports gear and equipment market, demonstrating a leading position through their demographic and cultural characteristics. These regions benefit from substantial urban populations, particularly in major centers such as Sydney, fostering a high level of engagement in diverse sports and fitness activities. This robust participation is underpinned by a well-developed sports infrastructure, encompassing numerous recreational facilities and active sports clubs. Furthermore, sustained government initiatives encouraging physical activity among residents contribute to a consistent demand for sports equipment and apparel, driven by the prevailing focus on health and wellness within these populous areas.

Recent Developments

-

In January 2025, New Balance unveiled its new Australian Open Collection, serving as the official performance apparel and footwear partner for the tournament. The collection offered a range of performance-oriented apparel and footwear designed for both athletes and fans. This line featured new colors inspired by the Australian landscape and showcased the company's focus on combining functionality with sports fashion. The new collection was available for purchase at New Balance's retail activations during the Australian Open, online, and at select retail stores in Australia.

-

In December 2024, global athletic brand Under Armour announced a strategic partnership and investment in ISC Sport, an Australian custom teamwear provider, by becoming a shareholder. This collaboration aimed to integrate Under Armour's product expertise with ISC's local market knowledge. The initial phase of this partnership involved the launch of a new basketball teamwear range and an online customisation tool in January 2025, which allowed Australian teams to design bespoke uniforms. ISC Sport serves over 2,500 amateur clubs, leagues, and schools across Australia annually.

-

In March 2024, Speedo unveiled the new Australian team uniforms for the Paris 2024 Olympics and Paralympics, highlighting breakthrough research in swimwear technology. The Fastskin® LZR® Intent 2.0 and LZR Valor 2.0 swimsuits were engineered by Speedo's Aqualab® research and development facility using Lamoral® Space Tech. This advanced material significantly improved hydrophobic qualities, resulting in lower water absorption and more durable water repellence. These innovative suits, developed by an all-female R&D team, were designed to enhance athlete performance for the Australian aquatics team.

-

In January 2024, PUMA globally launched its "Phenomenal Pack" football boots, which included the latest iterations of its FUTURE, ULTRA, and KING models. This product introduction was supported by a campaign featuring prominent Australian athletes from various football codes, demonstrating the brand's commitment to the Australian sports gear market. These advanced football boots, incorporating new innovations and technology, were made available for pre-sale through PUMA stores, PUMA.com, and specialist retailers across Australia, aiming to engage football enthusiasts ahead of the 2024 season.

Key Market Players

- Nike Inc.

- Adidas AG

- Puma SE

- Under Armour Inc.

- Decathlon S.A.

- Amer Sports Corporation

- Callaway Golf Company

- Yonex Co. Ltd.

- ASICS Corporation

- Wilson Sporting Goods Company

|

By Type

|

By Sales Channel

|

By Region

|

- Ball Over Net Games

- Ball Games

- Fitness/Strength Equipment

- Athletic Training Equipment

- Others

|

- Supermarkets/Hypermarkets

- Specialty Stores

- Online

- Others

|

- Australia Capital Territory & New South Wales

- Northern Territory & Southern Australia

- Western Australia

- Queensland

- Victoria & Tasmania

|

Report Scope:

In this report, the Australia Sports Gear & Equipment Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Australia Sports Gear & Equipment Market, By Type:

-

Ball Over Net Games

-

Ball Games

-

Fitness/Strength Equipment

-

Athletic Training Equipment

-

Others

-

Australia Sports Gear & Equipment Market, By Sales Channel:

-

Supermarkets/Hypermarkets

-

Specialty Stores

-

Online

-

Others

-

Australia Sports Gear & Equipment Market, By Region:

-

Australia Capital Territory & New South Wales

-

Northern Territory & Southern Australia

-

Western Australia

-

Queensland

-

Victoria & Tasmania

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Australia Sports Gear & Equipment Market.

Available Customizations:

Australia Sports Gear & Equipment Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Australia Sports Gear & Equipment Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com