|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 3.92 Billion

|

|

CAGR (2026-2031)

|

5.55%

|

|

Fastest Growing Segment

|

Cardiac Monitoring Devices

|

|

Largest Market

|

West

|

|

Market Size (2031)

|

USD 5.42 Billion

|

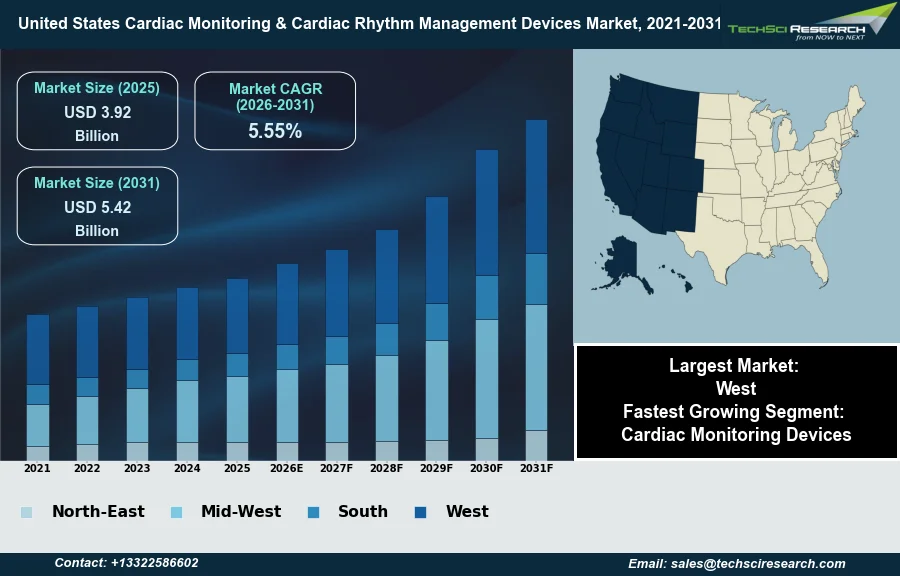

Market Overview

The United States Cardiac Monitoring & Cardiac Rhythm Management Devices Market will grow from USD 3.92 Billion in 2025 to USD 5.42 Billion by 2031 at a 5.55% CAGR. The United States Cardiac Monitoring and Cardiac Rhythm Management Devices Market encompasses medical technologies engineered to diagnose, monitor, and manage various cardiac arrhythmias and associated heart conditions, including implantable pacemakers, defibrillators, and external monitoring systems. Market expansion is primarily driven by the escalating prevalence of cardiovascular diseases and heart rhythm disorders within an aging population, coupled with continuous technological advancements enhancing device efficacy and patient comfort. For instance, according to the American Heart Association, in 2025, approximately 350,000 individuals in the U.S. experience an out-of-hospital cardiac arrest annually.

Despite robust growth drivers, a significant challenge impeding market expansion involves the substantial cost associated with advanced cardiac technologies and the complexities surrounding reimbursement policies. This factor can restrict broader access and adoption of innovative devices across various healthcare settings.

Key Market Drivers

Cardiovascular Disease Burden Spurs Market Growth

The United States Cardiac Monitoring and Cardiac Rhythm Management Devices Market is significantly propelled by the rising prevalence of cardiovascular diseases and arrhythmias among the population. The increasing burden of these conditions necessitates continuous advancements in diagnostic and therapeutic devices, driving demand across the healthcare spectrum. For instance, according to the American Heart Association, in its 2026 Heart Disease and Stroke Statistics Update, published in January 2026, between 2021 and 2023, 130.6 million US adults, or 48.9% of the adult population, had some form of cardiovascular disease. This widespread incidence underscores the critical need for effective monitoring and management solutions, directly fostering market expansion as more individuals require cardiac care.

Technological Advancements Accelerate Market Growth

Furthermore, continuous technological advancements in cardiac devices serve as a crucial accelerator for market growth. Innovations enhancing device functionality, miniaturization, and remote monitoring capabilities lead to improved patient outcomes and expanded treatment options. An example of this progress is AliveCor's January 2026 announcement of FDA clearance for the next generation of KAI 12L for its Kardia 12L ECG System, which now detects five additional cardiac determinations, bringing the total to 39 cleared determinations. Such innovations broaden the diagnostic capabilities and utility of cardiac monitoring devices, promoting their adoption. This translates into substantial market activity, with Boston Scientific's Cardiovascular segment generating approximately $3.5 billion in revenue during the first quarter of 2026. These technological leaps not only address existing clinical gaps but also create new market opportunities by offering more sophisticated and accessible cardiac care solutions.

Download Free Sample Report

Key Market Challenges

Cost and Reimbursement Barriers to Market Growth

The substantial cost associated with advanced cardiac technologies, coupled with the complexities of reimbursement policies, represents a significant impediment to the growth of the United States Cardiac Monitoring and Cardiac Rhythm Management Devices Market. These factors directly limit the widespread adoption and accessibility of innovative devices across diverse healthcare settings. High upfront costs can strain hospital budgets and patient out-of-pocket expenses, making advanced solutions less feasible for broader implementation.

Reimbursement Complexity and Underpayment Hindering Market Expansion

The intricacy of reimbursement pathways, particularly for novel technologies, often leads to delays in coverage and inadequate payment rates for healthcare providers. This financial burden can disincentivize the integration of new, advanced cardiac devices. For example, according to AdvaMed, concerning the fiscal year 2025, the Centers for Medicare and Medicaid Services (CMS) covered only 65 percent of the incremental cost difference for new technology add-on payment (NTAP) eligible devices, a figure that industry associations had previously characterized as a compromise. Such limitations directly constrain market expansion by hindering patient access and discouraging investment in next-generation cardiac monitoring and rhythm management solutions.

Key Market Trends

Leadless Pacemakers: A Less Invasive Evolution

Leadless pacemaker adoption represents a significant evolution in cardiac rhythm management, offering a less invasive alternative to traditional devices by eliminating transvenous leads and the need for a chest incision. This advancement directly addresses patient concerns regarding device visibility, infection risk associated with leads, and potential lead complications over time, thereby enhancing patient comfort and improving quality of life. The design, where the entire pacing system is encapsulated within a tiny device implanted directly into the heart, streamlines the procedure and recovery. For example, according to My Medicine Advisor, in its "Pacemaker 2026: New Leadless Tech & What Life Looks Like" article from June 2026, over 200,000 Americans received these innovative devices in 2025 alone, demonstrating a clear market shift towards these less intrusive solutions.

AI-Powered Diagnostics and Predictive Analytics in Cardiology

The expansion of artificial intelligence powered diagnostics and predictive analytics is fundamentally transforming cardiac care by enabling earlier and more accurate disease detection and risk stratification. AI algorithms analyze vast datasets from various monitoring devices to identify subtle patterns indicative of cardiac conditions that might be missed by conventional methods, moving care towards proactive intervention. This capability supports clinicians in making more informed decisions, optimizing treatment plans, and potentially preventing adverse cardiac events through personalized risk assessments. This trend is evident in the rapid development and clearance of such tools, with Cardiovascular Business reporting in March 2026 that cardiology now has more than 200 clinical AI applications available in the U.S. market, facilitating enhanced diagnostic precision and improving patient outcomes.

Segmental Insights

Drivers and Enablers of Growth in the U.S. Cardiac Monitoring Devices Market

The Cardiac Monitoring Devices segment is experiencing the most rapid expansion within the United States Cardiac Monitoring & Cardiac Rhythm Management Devices Market. This growth is primarily driven by the increasing prevalence of cardiovascular diseases and cardiac arrhythmias among an aging population, which necessitates continuous and early detection solutions. Significant technological advancements, including the development of AI-powered wearables, miniaturized devices, and remote patient monitoring systems, enhance diagnostic accuracy and patient convenience. Furthermore, the strong healthcare infrastructure in the U.S., coupled with supportive reimbursement policies and consistent approvals from regulatory bodies such as the U.S. Food and Drug Administration for innovative devices, significantly contribute to the rapid adoption and market expansion of these monitoring technologies.

Regional Insights

West Region Dominance Driven by Demographics, Infrastructure, and Innovation

The Western United States stands as a dominant region in the Cardiac Monitoring & Cardiac Rhythm Management Devices Market, driven by several specific factors. A significant population in states like California and Washington experiences a high prevalence of lifestyle-related conditions such as obesity, diabetes, and hypertension, which are major risk factors for cardiac arrhythmias and heart failure, thereby increasing demand for these devices. Furthermore, the region benefits from a robust healthcare infrastructure and an early adoption of advanced cardiac technologies, including remote patient monitoring systems. The presence of specialized cardiac centers and key medical device manufacturers also contributes substantially to market expansion in this region, solidifying the West's leadership.

Recent Developments

-

In December 2025, Abbott announced that its Volt™ Pulsed Field Ablation (PFA) System received U.S. Food and Drug Administration (FDA) approval for treating patients with atrial fibrillation (AFib). This new product launch introduced a minimally invasive cardiac ablation technology designed to use high-energy electrical pulses in targeted areas of the heart, aiming to stop irregular rhythms. The Volt PFA System is an all-in-one solution clinically proven to simplify AFib treatment, potentially leading to shorter procedure times and improved patient recovery within the United States cardiac rhythm management devices market.

-

In September 2025, Medtronic initiated a global pivotal study to investigate elevated and personalized cardiac pacing rates for treating patients with Heart Failure with preserved Ejection Fraction (HFpEF). This research represents a significant advancement within the cardiac rhythm management devices market in the United States, as it explores a novel application of pacing therapy for a patient population not currently treated by conventional pacemakers. The study aims to gather data to support a new pacing indication for HFpEF, a condition affecting millions globally, thereby potentially expanding therapeutic options and improving patient outcomes.

-

In June 2024, Endotronix received U.S. Food and Drug Administration (FDA) premarket approval for its Cordella pulmonary artery (PA) sensor, designed for remote heart failure monitoring. This new product launch introduced a system for patients with NYHA class III heart failure, combining internal PA pressure readings with non-invasive vital sign information. The device allows for seated measurements and transmits data to care teams, enabling real-time monitoring of potential congestion. This approval was set to enhance remote patient management capabilities within the United States cardiac monitoring devices market.

-

In March 2024, Wellysis, a digital healthcare company, collaborated with Artella Solutions to introduce a remote cardiac monitoring service in the United States. This partnership leverages Wellysis's FDA-cleared S-Patch ExL electrocardiogram device, which supports extended testing periods. The integrated service includes Samsung smartphones and smartwatches, aiming to provide a comprehensive end-to-end cardiac monitoring solution. This initiative enhances the accessibility of advanced cardiac diagnostics for patients, particularly in states like Texas, where the service initially launched, thereby expanding remote monitoring capabilities within the U.S. cardiac monitoring market.

Key Market Players

- Abbott Laboratories, Inc.

- Medtronic USA, Inc.

- Boston Scientific Corporation

- GE Healthcare

- Philips Healthcare

- Hill-Rom Holdings, Inc.

- BIOTRONIK, Inc.

- Alivecor, Inc.

|

By Product Type

|

By End User

|

By Region

|

- Cardiac Monitoring Devices

- Cardiac Rhythm Management Device

|

- Hospitals & Clinics

- Cardiac Care Centers

- Ambulatory Surgery Centers

- Others

|

- Northeast

- Midwest

- South

- West

|

Report Scope:

In this report, the United States Cardiac Monitoring & Cardiac Rhythm Management Devices Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

United States Cardiac Monitoring & Cardiac Rhythm Management Devices Market, By Product Type:

-

Cardiac Monitoring Devices

-

Cardiac Rhythm Management Device

-

United States Cardiac Monitoring & Cardiac Rhythm Management Devices Market, By End User:

-

Hospitals & Clinics

-

Cardiac Care Centers

-

Ambulatory Surgery Centers

-

Others

-

United States Cardiac Monitoring & Cardiac Rhythm Management Devices Market, By Region:

-

Northeast

-

Midwest

-

South

-

West

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the United States Cardiac Monitoring & Cardiac Rhythm Management Devices Market.

Available Customizations:

United States Cardiac Monitoring & Cardiac Rhythm Management Devices Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

United States Cardiac Monitoring & Cardiac Rhythm Management Devices Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com