|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

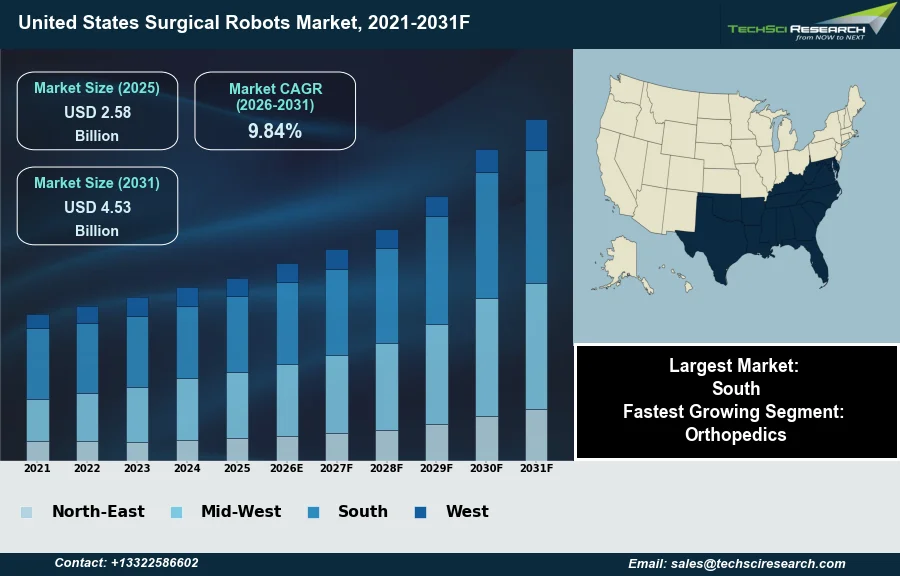

Market Size (2025)

|

USD 2.58 Billion

|

|

CAGR (2026-2031)

|

9.84%

|

|

Fastest Growing Segment

|

Orthopedics

|

|

Largest Market

|

South

|

|

Market Size (2031)

|

USD 4.53 Billion

|

Market Overview

The United States Surgical Robots Market will grow from USD 2.58 Billion in 2025 to USD 4.53 Billion by 2031 at a 9.84% CAGR. Surgical robots are advanced robotic systems engineered to assist surgeons in executing medical procedures with heightened precision, control, and dexterity, facilitating minimally invasive surgical techniques. Key drivers supporting the market's expansion include the escalating demand for less invasive surgical interventions, which offer benefits such as reduced recovery times and diminished patient trauma, alongside a growing aging population experiencing a rise in chronic diseases necessitating surgical care. Furthermore, increasing surgical workforce shortages contribute to the adoption of robotic platforms.

According to AdvaMed, the overall United States medical technology market was valued at $257 billion in 2024, with surgical robotics representing a significant and innovative component within this sector. However, a substantial impediment to market growth remains the considerable capital expenditure required for acquiring these advanced robotic systems, alongside ongoing maintenance costs, which can limit broader adoption across healthcare facilities.

Key Market Drivers

Rising MIS Adoption Drives U.S. Surgical Robotics Growth

Growing Adoption of Minimally Invasive Surgery (MIS) is a primary factor influencing the expansion of the United States surgical robots market. These procedures, characterized by smaller incisions and reduced tissue trauma, offer patients benefits such as faster recovery times, decreased post-operative pain, and shorter hospital stays. Robotic platforms provide surgeons with enhanced visualization, stability, and control, making complex MIS procedures more feasible and safer. This precision facilitates the execution of delicate surgical tasks, further encouraging the shift from traditional open surgeries to minimally invasive techniques across various medical specialties. According to Intuitive's CEO, in the Q1 2026 earnings call held in April 2026, da Vinci procedures in the United States increased by 14% year-over-year. The demonstrated advantages for both patients and healthcare providers contribute significantly to the increasing integration of robotic systems in surgical suites nationwide.

Ongoing Technological Advances and Strategic Investments in Robotic Platforms

Continuous Technological Advancements in Robotic Platforms represent another critical driver for market growth. Ongoing innovation leads to the development of more sophisticated and versatile robotic systems, incorporating features like improved haptic feedback, advanced imaging capabilities, and artificial intelligence-powered analytics. These enhancements broaden the application scope of robotic surgery, allowing for its use in an expanding array of procedures within orthopedics, urology, gynecology, and general surgery. According to AdvaMed, in October 2025, Stryker announced a commitment of over $150 million in 2025 to enhance its U.S. manufacturing facilities and technology upgrades. Such progress reinforces the value proposition of these systems to healthcare institutions, despite the fact that, according to the American College of Surgeons, in June 2026, robotic surgical systems often carry substantial costs, frequently exceeding $1 million per unit.

Download Free Sample Report

Key Market Challenges

Capital and maintenance costs constrain adoption of robotic systems

A substantial impediment to the expansion of the United States surgical robots market is the considerable capital expenditure required for acquiring these advanced systems, alongside ongoing maintenance costs. These significant financial demands directly restrict the broader adoption of robotic platforms across healthcare facilities. Many hospitals and surgical centers, particularly those with existing budget constraints, find it challenging to allocate the necessary funds for such high upfront investments. The continuous operational expenses for servicing and upkeep further compound this financial burden.

Budget constraints and delayed equipment upgrades slow market growth

This situation directly hampers market growth by limiting the number of new systems purchased. Healthcare providers often prioritize other pressing financial needs, delaying or forgoing investments in capital-intensive technologies like surgical robots. According to the American Hospital Association, in 2026, 94% of healthcare administrators expected to delay equipment upgrades to manage financial strain. This widespread deferral of equipment purchases translates directly into reduced sales volumes for manufacturers, thereby slowing the overall penetration and growth of the surgical robotics market.

Key Market Trends

ASC Expansion: Cost Efficiency and Access

A significant trend reshaping the United States surgical robots market is the expansion into Ambulatory Surgical Centers (ASCs). This strategic shift is driven by the advantages ASCs offer, including reduced operational costs, increased patient throughput, and the growing preference for outpatient surgical interventions, making advanced robotic procedures more accessible beyond traditional hospital settings. This decentralization of robotic surgery platforms also fosters greater competition and encourages the development of more compact and versatile robotic systems suited for smaller clinical environments. For instance, according to MedTech Dive, in June 2026, Stryker's Mako Robotic Power System, a miniaturized variant cleared by the FDA in August 2025, entered limited market release in early 2026, specifically targeting ambulatory surgical centers. This move signifies a clear market direction towards enabling robotic surgery in more cost-efficient outpatient facilities.

AI and Haptic Feedback in Robotic Surgery

Another prominent trend involves the deepening integration of Artificial Intelligence and advanced haptic feedback capabilities within robotic surgical systems. This integration transcends general technological advancements by providing surgeons with intelligent assistance for preoperative planning, real-time intraoperative guidance, and enhanced tactile sensation during delicate maneuvers. Artificial intelligence algorithms are increasingly used to process vast amounts of surgical data, improving procedural consistency and enabling predictive analytics for better patient outcomes. According to CMR Surgical, in March 2026, the company contributed nearly 500 hours of anonymized surgical data from its Versius Surgical Robotic System to Open-H, the world's largest open dataset for healthcare robotics, designed to train the next generation of intelligent surgical systems. Such efforts are crucial for developing sophisticated AI models that will further augment surgical precision and decision-making.

Segmental Insights

Orthopedics: Fastest-Growing Segment Driven by Demand, Precision Robotics, and Regulatory Approvals

In the United States Surgical Robots Market, Orthopedics stands out as the fastest-growing segment, driven by several compelling factors. The escalating prevalence of osteoarthritis, sports injuries, and age-related musculoskeletal conditions significantly increases the demand for total knee and hip replacement surgeries. Robotic-assisted systems offer enhanced accuracy in implant positioning, alignment, and bone preparation, which directly translates to improved patient mobility and reduced revision rates. This precision, coupled with the growing demand for minimally invasive procedures, leads to better patient outcomes, including shorter hospital stays and faster recovery. Regulatory approvals from bodies such as the U.S. Food and Drug Administration further support the adoption and innovation of orthopedic surgical robotics.

Regional Insights

Regional Leadership in Surgical Robotics: Hospitals, Investment, Demographics, and Training

The Southern United States stands as a leading region in the surgical robots market due to several key contributing factors. The region features a substantial number of large, high-capacity hospitals and surgical centers, which actively adopt advanced surgical technologies to perform complex procedures efficiently. This proactive integration is further supported by significant private and public investment in healthcare technology across the South. Furthermore, demographic patterns, including elevated rates of an aging population and obesity, drive increased demand for minimally invasive surgeries across various specialties. The presence of prominent medical schools and specialized robotic surgery training centers also fosters continuous surgeon training and technological innovation, consequently boosting market penetration.

Recent Developments

-

In December 2025, Medtronic announced a significant development in the United States surgical robots market with the U.S. Food and Drug Administration (FDA) clearance of its Hugo robotic-assisted surgery (RAS) system for urologic surgical procedures. This regulatory approval represented a crucial step, allowing Medtronic to initiate commercial adoption of the Hugo RAS platform within the U.S. healthcare system. The system's clearance for urologic procedures is a foundational move toward expanding access to minimally invasive care and increasing competition in the robotic surgery segment.

-

In April 2025, Johnson & Johnson MedTech marked a key milestone in the United States surgical robots market by completing the initial clinical trial cases for its OTTAVA Robotic Surgical System. This achievement followed the system's investigational device exemption (IDE) approval from the U.S. Food and Drug Administration in late 2024. The OTTAVA system is engineered to provide a versatile platform for various general surgery procedures, including those in the upper abdomen such as gastric bypass. This advancement signals progress in developing new robotic solutions for complex soft-tissue surgeries.

-

In March 2025, Stryker introduced several innovations to the United States surgical robots market at a major industry event. The company launched Mako Total Hip with Advanced Primary and Revision, which notably incorporated a robotic hip revision capability, a first in the market for surgical robots. Additionally, Stryker unveiled its fourth-generation Mako System, known as Mako 4. These product enhancements expand the capabilities of robotic-assisted surgery for hip and knee procedures, providing surgeons with advanced tools for both primary and revision total hip arthroplasty.

-

In February 2024, Stryker showcased significant enhancements to its Mako surgical robotic platform, impacting the United States surgical robots market. These updates included the introduction of new joint replacement technologies and the development of the myMako application for Apple Vision Pro and iPhone, designed to extend surgeons' Mako SmartRobotics experience. The company also announced plans to launch Mako Spine and Mako Shoulder applications in the latter half of 2024, further broadening the system's utility across orthopaedic procedures in the U.S. These developments aimed to improve surgical planning and execution.

Key Market Players

- Medtronic USA, Inc

- Intuitive Surgical, Inc.

- Stryker Corporation

- Johnson & Johnson

- Medrobotics Corporation

- TransEnterix, Inc.

- Zimmer Biomet Holdings, Inc.

- Think Surgical, Inc.

- Accuray Incorporated

- Globus Medical, Inc.

|

By Application

|

By End User

|

By Region

|

- Orthopedics

- Neurology

- Urology

- Gynecology

- Others

|

|

- Northeast

- Midwest

- South

- West

|

Report Scope:

In this report, the United States Surgical Robots Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

United States Surgical Robots Market, By Application:

-

Orthopedics

-

Neurology

-

Urology

-

Gynecology

-

Others

-

United States Surgical Robots Market, By End User:

-

United States Surgical Robots Market, By Region:

-

Northeast

-

Midwest

-

South

-

West

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the United States Surgical Robots Market.

Available Customizations:

United States Surgical Robots Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

United States Surgical Robots Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com