|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 11.01 Billion

|

|

CAGR (2026-2031)

|

8.51%

|

|

Fastest Growing Segment

|

Therapeutic Devices

|

|

Largest Market

|

Mid-West

|

|

Market Size (2031)

|

USD 17.97 Billion

|

Market Overview

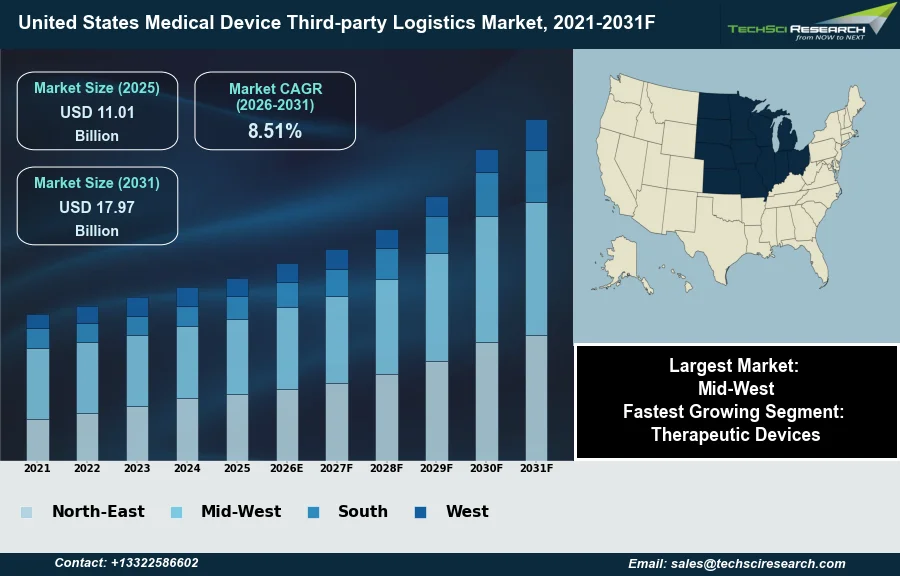

The United States Medical Device Third-party Logistics Market will grow from USD 11.01 Billion in 2025 to USD 17.97 Billion by 2031 at a 8.51% CAGR. The United States Medical Device Third-party Logistics (3PL) market involves the outsourcing of critical logistics functions, including warehousing, transportation, and inventory management, by medical device manufacturers to specialized external providers. This market is primarily driven by the increasing complexity of modern medical devices, which often necessitates specialized handling, temperature control, and secure packaging to maintain product integrity and efficacy. Manufacturers are also increasingly leveraging 3PL services to navigate stringent regulatory compliance requirements, optimize supply chain costs, and enhance operational efficiency, thereby allowing them to concentrate on core competencies such as research and development. According to AdvaMed, in July 2025, the U.S. medtech industry's annual output exceeded $250 billion, underscoring the substantial market volume managed by these logistics partners.

However, a significant challenge impeding market expansion is the continuous need to adapt to complex and evolving regulatory frameworks specific to medical devices, which demand constant investment in specialized infrastructure and compliance expertise from 3PL providers. Additionally, ensuring data security and end-to-end traceability throughout the supply chain presents an ongoing hurdle, particularly with the increasing digitization of logistics operations and interconnected medical devices. These factors necessitate robust quality management systems and transparent operational protocols to uphold product safety and efficacy.

Key Market Drivers

Technology-Driven Advancements in Medical Device 3PL

Advancements in logistics technology integration are a significant catalyst for the United States Medical Device Third-party Logistics market. The increasing adoption of sophisticated digital tools, such as artificial intelligence, internet of things devices, and advanced automation, enhances operational efficiency, improves supply chain visibility, and enables proactive management of complex logistics challenges. These technologies empower 3PL providers to offer highly specialized services, including real-time tracking, predictive analytics for demand forecasting, and optimized routing, which are crucial for sensitive medical devices. For instance, AI companies captured 55% of all health tech venture funding in 2025, underscoring the substantial investment and innovation in technology relevant to the broader healthcare ecosystem and its logistics needs.

Expansion of Cold-Chain Capabilities in Healthcare Logistics

Furthermore, the growing need for temperature-controlled logistics represents another pivotal driver for market expansion, particularly with the proliferation of temperature-sensitive medical devices, biologics, and specialized pharmaceutical products. Maintaining precise environmental conditions throughout the supply chain is paramount for product efficacy and patient safety, necessitating specialized infrastructure and expertise from 3PL partners. This demand is leading to significant investments in cold chain capabilities; for example, according to The Loadstar, in June 2026, FedEx announced a $48 million investment in its cold chain infrastructure to support healthcare traffic. Overall, the robust activity within the sector is underpinned by substantial industry commitment, with AdvaMed reporting in July 2025 that the U.S. medtech industry invests over $20 billion annually in research and development.

Download Free Sample Report

Key Market Challenges

Regulatory Complexity and Rising Costs Hindering US Medical Device 3PL Growth

The continuous need to adapt to complex and evolving regulatory frameworks specific to medical devices presents a significant impediment to the growth of the United States Medical Device Third-party Logistics (3PL) market. Medical device logistics providers must navigate an intricate web of regulations, including those from the U.S. Food and Drug Administration (FDA) pertaining to Good Manufacturing Practices, quality systems, and traceability requirements. This necessitates substantial and ongoing investment in specialized infrastructure, such as validated temperature-controlled warehousing and compliant transportation fleets, along with continuous training for personnel to maintain expertise in regulatory compliance. According to the U.S. Food and Drug Administration's published user fees, for fiscal year 2026, annual medical device establishment registration fees increased by 23%. These rising regulatory costs directly translate into increased operational expenditures for 3PL providers, impacting their service pricing and overall competitiveness. This heightened capital outlay and operational complexity also create significant barriers to entry for new 3PL entities and limit the expansion capabilities of existing providers, thereby directly hampering the market's overall growth potential.

Key Market Trends

Nearshoring and reshoring reshape US medical device 3PL

The increasing adoption of nearshoring and reshoring supply chain strategies represents a significant trend reshaping the United States Medical Device Third-party Logistics market. This shift is driven by a desire to enhance supply chain resilience, mitigate geopolitical risks, and reduce lead times for critical medical products, moving away from globalized manufacturing models. Medical device manufacturers are increasingly investing in domestic production and distribution capabilities to ensure reliable access. For instance, according to BD (Becton, Dickinson and Company), May 1, 2025, the company announced its intention to invest $2.5 billion in U.S. manufacturing capacity over the next five years. This trend necessitates that 3PL providers expand domestic warehousing networks and develop agile transportation solutions.

Decentralized healthcare drives direct-to-patient logistics

Another pivotal trend influencing the market is the continued growth of logistics for decentralized healthcare. This involves a fundamental shift in healthcare delivery, moving from traditional hospital settings towards home-based care, remote patient monitoring, and smaller ambulatory clinics. Such decentralization drives demand for specialized direct-to-patient logistics, including precise last-mile delivery to individual homes and efficient reverse logistics for devices. Third-party logistics providers must adapt service models to accommodate smaller, more frequent deliveries, often requiring enhanced patient interaction and stringent compliance. For example, according to a report on Cardinal Health's statistics, January 12, 2026, their at-Home Solutions division recorded US$3,480 million in 2025. This evolution requires 3PLs to develop robust capabilities for managing diverse delivery points and ensuring product integrity outside traditional facilities.

Segmental Insights

Rapid Expansion of Therapeutic Devices Logistics Driven by Complexity, Cold Chain Demands, and Regulation

The United States Medical Device Third-party Logistics Market is witnessing its most rapid expansion within the Therapeutic Devices segment. This significant growth stems from the increasing complexity and technological advancements inherent in therapeutic solutions, necessitating specialized handling, precise temperature control, and robust cold chain logistics throughout the supply chain to maintain product efficacy and safety. Furthermore, the escalating prevalence of chronic diseases and an aging population in the U.S. consistently fuel demand for innovative therapeutic devices, including biologics and advanced digital therapies. Adherence to stringent regulatory requirements, particularly those enforced by the U.S. Food and Drug Administration (FDA), further mandates sophisticated logistics support for these critical medical products.

Regional Insights

Midwest as a Leading Hub for Medical Device 3PL Demand

The Mid-West stands as a leading region within the United States Medical Device Third-party Logistics Market due to its significant concentration of pharmaceutical and biotechnology companies. These firms produce a wide array of healthcare products, including medical equipment and diagnostics, generating substantial demand for specialized third-party logistics services such as warehousing, shipping, and distribution. For instance, Minnesota is recognized as a global center for medical device innovation and production, fostering a robust industry cluster that necessitates advanced logistics support. This established manufacturing base and associated supply chain infrastructure drive the need for expert partners capable of adhering to stringent regulatory requirements for handling and transporting medical devices, ensuring compliance with standards set by bodies like the Food and Drug Administration (FDA).

Recent Developments

-

In September 2025, DHL Supply Chain formalized an agreement to acquire SDS Rx, a specialized provider of final-mile delivery and transportation services for healthcare. This acquisition was designed to significantly expand DHL’s life sciences and healthcare capabilities in North America, particularly enhancing its offerings for long-term care facilities, specialty pharmacies, radiopharmacies, and health system networks. By integrating SDS Rx’s operations, including its network across over 200 U.S. locations, DHL aimed to strengthen its ability to provide integrated, time-critical solutions and expand same-day and expedited delivery services for medical devices and other sensitive healthcare products. This move underscored a strategic expansion within the United States medical device third-party logistics market.

-

In April 2025, DHL Group committed over $1.1 billion towards bolstering its North American healthcare logistics operations, forming a key part of its broader global investment strategy. This substantial capital was directed at enhancing infrastructure and technology specifically for medical device, clinical trial, biopharma, and cell and gene therapy logistics. The initiatives included expanding cold chain capacity in existing facilities, establishing cross-divisional Good Distribution Practices-certified “Pharma Hubs” for multi-temperature shipments, and investing in advanced technology across storage, order fulfillment, and distribution. This strategic expansion aimed to strengthen DHL’s integrated logistics solutions, ensuring efficient and reliable delivery of essential healthcare products within the United States medical device third-party logistics market.

-

In January 2025, UPS Healthcare showcased its ongoing commitment to advanced healthcare logistics by continuing significant investments in its capabilities. The company addressed the increasing demand for complex supply chain solutions across biopharma, medical devices, and lab diagnostics. A notable development was the operation of its new 100,000 square-foot Labport facility. Positioned strategically near UPS Airlines' largest air hub, this facility was designed to accelerate diagnostic processes, ensuring that specimens arriving overnight could yield results by early morning. This initiative underscored UPS Healthcare's innovation in delivering precise treatments more rapidly within the United States medical device third-party logistics market.

-

In August 2024, Cardinal Health announced plans for a new distribution center in Walton Hills, Ohio, to bolster its U.S. Medical Products and Distribution business. Anticipated to be fully operational by spring 2025, the nearly 249,000 square-foot facility significantly expanded the company's warehouse capacity in the Cleveland area, replacing an older location. This investment integrated new technology solutions and automation aimed at improving workflows and enhancing operational efficiencies for moving medical products. The initiative was set to improve service quality for customers and daily work experiences for employees, reinforcing Cardinal Health’s presence in the United States medical device third-party logistics market.

Key Market Players

- Cardinal Health, Inc.

- Deutsche Post AG

- FedEx Supply Chain

- Kuehne + Nagel International AG

- United Parcel Service, Inc.

- SF Holding Limited

- Cencora, Inc.

- C.H. Robinson Worldwide, Inc.

- Plexus Corp.

- GXO Logistics, Inc.

|

By Service

|

By Type

|

By Device Type

|

By End Use

|

By Region

|

- Transportation

- Warehousing and Storage

|

- Cold Chain Logistics

- Non-cold Chain Logistics

|

- Diagnostic Devices

- Therapeutic Devices

|

- Medical Device Companies

- Hospitals & Clinics

- Others

|

- Northeast

- Midwest

- South

- West

|

Report Scope:

In this report, the United States Medical Device Third-party Logistics Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

United States Medical Device Third-party Logistics Market, By Service:

-

Transportation

-

Warehousing and Storage

-

United States Medical Device Third-party Logistics Market, By Type:

-

Cold Chain Logistics

-

Non-cold Chain Logistics

-

United States Medical Device Third-party Logistics Market, By Device Type:

-

Diagnostic Devices

-

Therapeutic Devices

-

United States Medical Device Third-party Logistics Market, By End Use:

-

Medical Device Companies

-

Hospitals & Clinics

-

Others

-

United States Medical Device Third-party Logistics Market, By Region:

-

Northeast

-

Midwest

-

South

-

West

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the United States Medical Device Third-party Logistics Market.

Available Customizations:

United States Medical Device Third-party Logistics Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

United States Medical Device Third-party Logistics Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com