|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

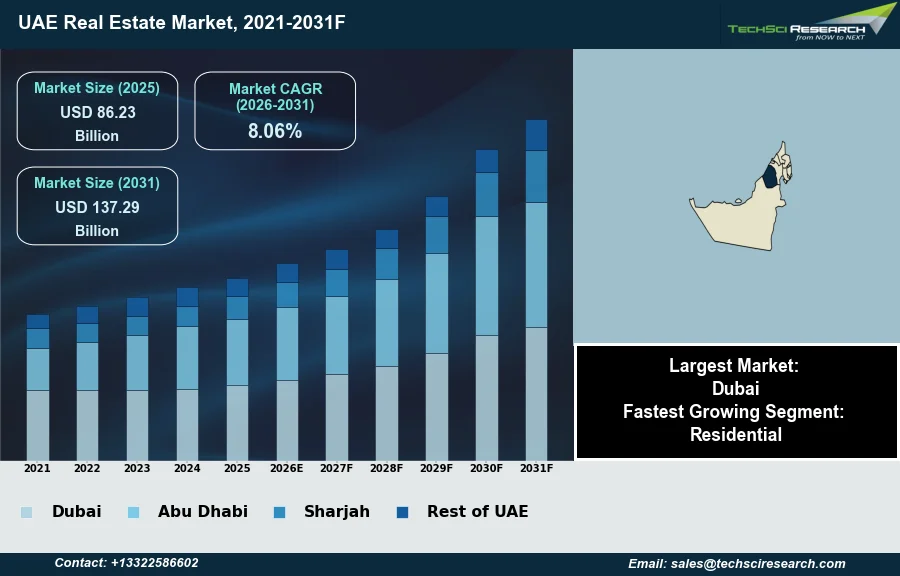

Market Size (2025)

|

USD 86.23 Billion

|

|

CAGR (2026-2031)

|

8.06%

|

|

Fastest Growing Segment

|

Residential

|

|

Largest Market

|

Dubai

|

|

Market Size (2031)

|

USD 137.29 Billion

|

Market Overview

The UAE Real Estate Market will grow from USD 86.23 Billion in 2025 to USD 137.29 Billion by 2031 at a 8.06% CAGR. The UAE Real Estate Market comprises the comprehensive development, sale, leasing, and management of residential, commercial, industrial, and hospitality properties throughout the Emirates. Its sustained growth is fundamentally driven by proactive government initiatives fostering economic diversification, a consistently stable and attractive regulatory framework, and substantial foreign direct investment. According to the Dubai Land Department, in Q1 2026, total real estate transactions in Dubai reached AED 252 billion, marking a 31 percent increase in value year-on-year. Concurrently, the Abu Dhabi Real Estate Centre reported Q1 2026 transactions totaling approximately AED 66 billion, representing a 160.7 percent increase in value compared to the same period in 2025.

This expansion is further propelled by robust population growth and continuous infrastructure development, drawing both local and international investors seeking stable, long-term asset opportunities. Nevertheless, a significant challenge that could hinder market expansion is the escalating affordability concerns among mid-income buyers, as property prices and rental rates continue to rise substantially across key segments.

Key Market Drivers

Diversified Economy Drives UAE Real Estate

Robust economic growth and diversification serve as a fundamental driver for the UAE real estate market, fostering an environment conducive to investment and development. The nation's strategic efforts to lessen reliance on oil revenues have stimulated expansion across various non-oil sectors, including tourism, finance, and logistics. This diversification translates into job creation and increased disposable income, directly boosting demand for both residential and commercial properties. According to the Federal Competitiveness and Statistics Centre, as reported by The National News, in May 2026, the UAE's non-oil gross domestic product grew by 6.8 percent in 2025, reaching AED 1.5 trillion. This sustained economic momentum encourages businesses to expand operations, leading to higher occupancy rates in office spaces and industrial parks, while also supporting consumer confidence in property purchases.

Population Growth and Expatriates Drive Housing Demand

Significant population growth and a continuous inflow of expatriates are further propelling the real estate sector. The UAE’s attractive lifestyle, career opportunities, and progressive visa reforms consistently draw a diverse international workforce and resident base. This demographic expansion directly fuels demand for housing, ranging from apartments to villas, and contributes to a dynamic rental market. According to DXB Interact, in October 2025, Dubai's population reached 4,036,863, representing a 5.43 percent annual increase with over 208,030 new residents. The sustained influx of residents necessitates ongoing residential development and infrastructure upgrades to accommodate the growing community. Overall, Dubai's real estate market closed 2025 with property sales surging 30.64 percent year on year to more than Dh682.49 billion, as reported by Gulf News in January 2026.

Download Free Sample Report

Key Market Challenges

Affordability Pressures Constrain Mid-Income Demand

The escalating affordability concerns among mid-income buyers pose a direct challenge to the UAE Real Estate Market's expansion. Significant rises in property prices and rental rates restrict the purchasing power of a critical demographic, consequently limiting their ability to engage in the ownership market or secure long-term leases. This constraint directly impacts market liquidity by narrowing the pool of viable purchasers and renters for various property segments.

Rising Rents and Declining Transaction Volumes Damp Market Growth

For example, according to property analytics platform DXB Interact, in July 2025, average apartment rents in Dubai climbed 21.7% year-on-year, reaching AED 103,000 annually. Villa rents similarly rose 19.6%, averaging AED 328,000 per year. These substantial increases disproportionately burden household budgets, forcing mid-income individuals to defer property acquisition. The resulting decline in accessible housing options can hinder sustained population growth and impact the inflow of professionals. This trend also manifested in Abu Dhabi, where, according to Cavendish Maxwell, apartment transaction volumes dropped 60.5% year-on-year in Q1 2025. Such reduced transactional activity ultimately impedes the overall growth trajectory of the real estate sector.

Key Market Trends

Off-Plan Sales as a Barometer of Investor Confidence

Prevalence of off-plan property sales and investment represents a key trend, indicating sustained investor confidence and a forward-looking market sentiment. This segment allows buyers to secure properties at potentially advantageous prices before completion, attracting both local and international investors seeking capital appreciation and future rental income. The robust demand in this area underscores the market's long-term growth expectations and developers' ability to fund new projects. For instance, according to Gulf News, May 2026, in the 'Dubai Home Sales Hit Dh139 Billion as Off-Plan Deals Surge and Rent Growth Cools in Q1 2026' article, off-plan units accounted for Dh105.5 billion in Dubai sales during the first quarter of 2026, reflecting a significant year-on-year increase.

Sustainable and Smart Building Technologies in Development

The emergence of sustainable and smart building technologies is also a significant trend, transforming development practices and aligning the market with global environmental and technological advancements. Developers are increasingly incorporating energy-efficient designs, smart home systems, and eco-friendly materials to meet evolving buyer preferences and regulatory requirements. This shift enhances property value and operational efficiency while contributing to the UAE's broader sustainability goals. As reported by Property Shop Investment, May 2026, Abu Dhabi announced a major Dh42 billion investment for smart city, infrastructure, and sustainability development, demonstrating a substantial commitment to integrating advanced solutions into its urban fabric.

Segmental Insights

Residential Real Estate Leads UAE Market Amid Visa Reforms

The UAE Real Estate Market demonstrates robust momentum, with the residential segment emerging as the fastest-growing area. This rapid expansion is primarily driven by progressive government visa reforms, such such as the Golden Visa program, which attract a consistent influx of expatriates and international investors seeking long-term residency and quality living. Furthermore, the nation's strategic economic diversification initiatives beyond hydrocarbon dependence create sustained job growth and population increases, consequently boosting demand for diverse housing solutions across major emirates like Dubai and Abu Dhabi.

Regional Insights

Dubai leads UAE real estate through diversification and global positioning

Dubai leads the UAE Real Estate Market, primarily due to its robust economic diversification strategy, positioning it as a premier global city and an international financial hub. Progressive government policies, including attractive long-term residency visas and a favorable tax structure, consistently draw significant foreign investment and high-net-worth individuals. The emirate's world-class infrastructure, meticulous urban planning, and the transparent regulatory framework overseen by the Dubai Land Department and its Real Estate Regulatory Agency, collectively foster a secure and trustworthy investment environment. These strategic advantages, coupled with consistent population growth, solidify Dubai's dominance as a resilient and appealing regional market.

Recent Developments

-

In July 2025, Nakheel announced the final phase of its Bay Grove Residences, situated on Dubai Islands, following the successful sell-out of its earlier waterfront residential units. This phase of the sought-after development comprised 257 urban residential units within four contemporary buildings. The offerings included one to four-bedroom apartments and a unique penthouse, all positioned to provide panoramic views of the Arabian Gulf and exclusive access to Crystal Beach, enhancing luxury living in the UAE Real Estate Market.

-

In June 2025, Aldar Properties revealed the master plan for Fahid Island, a new destination in Abu Dhabi with a gross development value exceeding Dh40 billion ($10.8 billion). Located between Yas Island and Saadiyat Island, this extensive project spans 2.7 million square meters and features an 11-kilometer coastline. Plans included over 6,000 residences, ranging from apartments to luxury villas, alongside a focus on wellness, sustainable design, and the introduction of an educational experience through a partnership with an international institution.

-

In February 2025, Aldar Properties launched "The Wilds" in Dubai, an eco-luxury community strategically situated along Sheikh Mohammed bin Zayed Road. This development in the UAE Real Estate Market introduced approximately 1,700 thoughtfully designed villas and apartments, with starting prices from AED 5.1 million. The Wilds aimed to balance nature immersion with urban accessibility and was recognized as the UAE's first residential development to achieve both LEED Platinum and Fitwel 3-Star certifications, setting new standards for sustainable luxury living.

-

In January 2025, DAMAC Properties unveiled "Riverside Views," marking its inaugural development of the year within the newly introduced DAMAC Riverside community in Dubai. This project by the leading UAE property developer offered a collection of stylish one- and two-bedroom apartments across eight distinctively themed clusters. The design was focused on connecting residents with nature and community through a blend of greenery and water features, providing a unique lifestyle experience in the UAE Real Estate Market.

Key Market Players

- Emaar Properties PJSC

- DAMAC Properties

- Meraas Holding

- Nakheel

- Wasl Asset Management

- Aldar Properties

- Majid Al Futtaim Properties

- Dubai Properties

- Jumeirah Group

- Emirates Real Estate

|

By Property Type

|

By Business

|

By End User

|

By Region

|

- Residential

- Commercial

- Industrial

- Hospitality

- Others

|

|

- Owner-occupied

- Rented

- Institutional buyers

- Government buyers

|

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

|

Report Scope:

In this report, the UAE Real Estate Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

UAE Real Estate Market, By Property Type:

-

Residential

-

Commercial

-

Industrial

-

Hospitality

-

Others

-

UAE Real Estate Market, By Business:

-

UAE Real Estate Market, By End User:

-

Owner-occupied

-

Rented

-

Institutional buyers

-

Government buyers

-

UAE Real Estate Market, By Region:

-

Dubai

-

Abu Dhabi

-

Sharjah

-

Rest of UAE

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the UAE Real Estate Market.

Available Customizations:

UAE Real Estate Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

UAE Real Estate Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com