|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

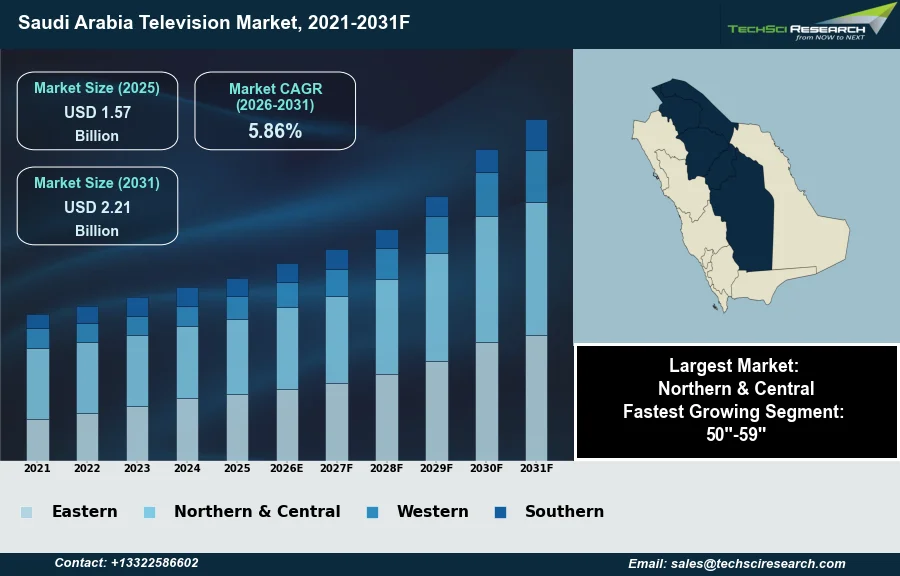

Market Size (2025)

|

USD 1.57 Billion

|

|

CAGR (2026-2031)

|

5.86%

|

|

Fastest Growing Segment

|

50''-59''

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 2.21 Billion

|

Market Overview

The Television Market in Saudi Arabia will grow from USD 1.57 Billion in 2025 to USD 2.21 Billion by 2031 at a 5.86% CAGR. The Saudi Arabia Television Market encompasses the distribution and consumption of linear broadcasting and over-the-top video content, alongside the retail of associated television receiving equipment. Market expansion is primarily driven by high rates of media consumption across various platforms, robust internet penetration, and increasing disposable incomes among a youthful, digitally engaged population. Government initiatives under Vision 2030 further stimulate demand through investments in digital infrastructure and entertainment sector diversification. According to the Saudi Press Agency, in December 2025, Saudi Arabia was unanimously re-elected to head the Arab States Broadcasting Union (ASBU) for its third consecutive term, underscoring its pivotal role in regional broadcasting cooperation.

A significant challenge impeding market expansion stems from stringent content restrictions and censorship imposed by regulatory bodies. These guidelines prohibit material deemed contrary to public morals or Islamic teachings, often necessitating content alteration or removal by platforms. Such regulatory mandates can create operational complexities for international media providers and limit content diversity available to consumers.

Key Market Drivers

OTT Streaming Drives Saudi Arabia's TV Market Growth

The proliferation of Over-the-Top (OTT) streaming platforms significantly drives the Saudi Arabia Television Market by reshaping content consumption habits. These platforms, offering diverse on-demand video content, have gained substantial traction among a tech-savvy population, leading to increased demand for smart televisions and robust internet connectivity. The convenience and personalization offered by OTT services are transitioning viewers from traditional linear broadcasting, compelling television manufacturers to integrate advanced smart features. According to Communicate Staff, April 2026, in "Saudi Arabia's television and video market becomes prime growth arena for advertisers", OTT revenues in Saudi Arabia were projected to grow at an 11.9 percent compound annual growth rate from 2019 through 2025. This growth underscores the critical role of streaming in the market's evolution.

Rising Incomes and Digital Engagement Fuel Demand for Modern TV Tech

Rising household disposable incomes further stimulate the market by enhancing consumer purchasing power for advanced television sets and premium entertainment subscriptions. As economic diversification initiatives continue to yield results, a growing segment of the population is willing to invest in higher-resolution displays and sophisticated home theater systems, elevating the overall quality of home entertainment. According to the Mastercard Economics Institute's Economic Outlook 2025 for Saudi Arabia, December 2024, consumer spending in the Kingdom was predicted to rise by 4.5% in 2025. This increased spending directly translates into demand for modern television technology and services. Overall, digital engagement remains exceptionally high; according to the Communications, Space and Technology Commission, in 2025, approximately 48.6 percent of internet users in Saudi Arabia spent seven hours or more daily online.

Download Free Sample Report

Key Market Challenges

Censorship and regulatory constraints limit programming diversity and market growth

Stringent content restrictions and censorship represent a significant challenge to the growth of the Saudi Arabia Television Market. Regulatory bodies impose guidelines that prohibit material deemed contrary to public morals or Islamic teachings, necessitating content alteration or complete removal by media platforms. This directly limits the diversity of programming available to consumers, reducing overall choice and potentially decreasing engagement with compliant services.

Regulatory burdens impede foreign entrants and market dynamism

Such mandates create considerable operational complexities for both local and international media providers. Foreign entities, in particular, face the burden of adapting their global content libraries to local standards, which can involve significant resource allocation for review, editing, and compliance management. These administrative and financial burdens can deter new international entrants and constrain the expansion of existing foreign media providers, thereby impeding the overall dynamism and competitiveness of the Saudi television market.

Key Market Trends

Rising Local Content and Audience Demand in Saudi TV

Increasing local content production and consumption is significantly shaping the Saudi Arabia Television Market, driven by government initiatives to foster a vibrant domestic creative economy. This trend reflects a cultural shift towards narratives that resonate with local audiences and leverage indigenous talent. The growing emphasis on local storytelling across film and television platforms is cultivating a stronger sense of national identity in media. According to the Saudi Film Commission, April 10, 2026, in "Saudi box office 2025: SAR 921M revenue, 18.8M tickets sold", Saudi films generated total revenues of SAR 122.6 million in 2025, achieved through 11 films and 2.8 million tickets sold. This demonstrates a clear audience appetite and financial growth within the local content segment.

Expansion of Connected TV Advertising in MENA

The expansion of targeted Connected TV advertising represents another pivotal trend, enabling advertisers to engage specific audience segments with greater precision than traditional linear broadcasting. As consumers increasingly adopt smart televisions and streaming platforms, the ability to deliver personalized advertisements based on viewing habits and demographic data becomes a valuable asset for brands. This shift provides an enhanced return on investment for advertisers by minimizing wasted impressions and improving campaign relevance. According to IAB MENA, June 09, 2026, as reported in "Digital ad spend in MENA reaches $8b in 2025, IAB report reveals", the Middle East and North Africa digital advertising market reached $8.185 billion in 2025, marking 17.8 percent year-on-year growth, with dedicated estimates for Connected TV included for the first time within this expanding market.

Segmental Insights

50–59 inch TVs: fastest-growing segment driven by rising incomes and demand for immersive, communal 4K/smart viewing.

The Saudi Arabia Television Market is experiencing a notable transformation, with the 50''-59'' segment emerging as the fastest-growing category, driven by evolving consumer preferences for enhanced home entertainment experiences. This rapid expansion is primarily fueled by increasing disposable incomes across the Kingdom, allowing households to invest in larger, more technologically advanced displays. Saudi consumers prioritize immersive viewing for communal entertainment, a deep-rooted cultural tradition, making larger screens ideal for shared experiences such as watching movies, sports, and streaming content. Furthermore, the availability of high-resolution 4K and smart TV features within this size range, coupled with a general decline in the per-inch cost of larger displays, makes the 50''-59'' segment an attractive and attainable upgrade for many households seeking superior visual quality and integrated digital services.

Regional Insights

Population Density and Urban Infrastructure Drive Regional Market Leadership

The Northern & Central region holds a prominent position within the Saudi Arabia Television Market, primarily driven by its significant population concentration and extensive urban development. This region, encompassing major economic hubs such as Riyadh, benefits from a substantial aggregation of households. Consumers here generally exhibit higher purchasing power and increased disposable incomes, enabling greater investment in advanced television technologies and diverse entertainment systems. Furthermore, the robust retail infrastructure and well-developed telecommunications networks in these urban centers facilitate strong consumer demand and access to modern viewing platforms, reinforcing the region's market leadership.

Recent Developments

-

In July 2025, Netflix formed a strategic partnership with the Saudi Arabia-based MBC Group, a prominent media and entertainment conglomerate. The collaboration introduced a bundled service offering to subscribers, combining access to MBC's traditional linear television channels, its Shahid streaming platform, and the comprehensive Netflix content catalog. This alliance aimed to provide a unified and more economical entertainment solution for consumers across Saudi Arabia and the wider MENA region. The partnership represented a significant development in the Saudi television market, merging the offerings of major streaming and broadcasting entities.

-

In December 2024, stc tv, the digital entertainment service under stc Group's subsidiary Intigral, received the "Best Content Strategy of the Year" award at the BroadcastPro ME Awards. This recognition highlighted stc tv's effective approach to delivering high-quality content experiences through innovative and customer-focused strategies in the Saudi Arabian television market. The company integrated innovative AI solutions within its content strategy to enhance consumer interaction and experience. This strategic success affirmed stc tv's dedication to developing advanced digital entertainment solutions for its regional audience.

-

In October 2024, stc tv, a digital entertainment platform operating in Saudi Arabia, was recognized with the “Best Voice of the Customer” award at the 2024 Customer Experience & Loyalty Summit & Awards held in Riyadh. This accolade acknowledged stc tv’s commitment to improving entertainment platforms through innovative customer feedback strategies. The company notably utilized an AI-powered feedback analysis tool, which contributed to an 86% customer satisfaction score during the year. This achievement underscored the platform's focus on user experience through advanced research and technology within the Saudi Arabian television market.

-

In May 2024, Intigral, the media arm of stc Group, entered into a collaboration agreement with Beyond ONE, a digital services provider. This partnership facilitated the integration of stc tv services for Virgin Mobile KSA customers in Saudi Arabia. The initiative marked a significant expansion for Intigral, aiming to enrich the digital entertainment landscape within the Kingdom. Through this agreement, Virgin Mobile KSA subscribers gained access to an extensive library of content, including over 28,000 video-on-demand titles and more than 200 linear television channels, enhancing their viewing options.

Key Market Players

- Samsung TV KSA

- LG TV KSA

- Sony TV KSA

- Hisense KSA

- TCL KSA

- Alshaya TV

- Jarir TV

- Extra TV

- Lulu TV

- HyperPanda TV

|

By Screen Size

|

By Display Type

|

By Sales Channel

|

By Region

|

- 50''-59''

- 40''-49''

- 39'' and Below

- Above 59''

|

|

- Supermarkets/Hypermarkets

- Multi Branded Stores

- Online

- Others

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Television Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Television Market, By Screen Size:

-

50''-59''

-

40''-49''

-

39'' and Below

-

Above 59''

-

Saudi Arabia Television Market, By Display Type:

-

Saudi Arabia Television Market, By Sales Channel:

-

Supermarkets/Hypermarkets

-

Multi Branded Stores

-

Online

-

Others

-

Saudi Arabia Television Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Television Market.

Available Customizations:

Saudi Arabia Television Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Television Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com