|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

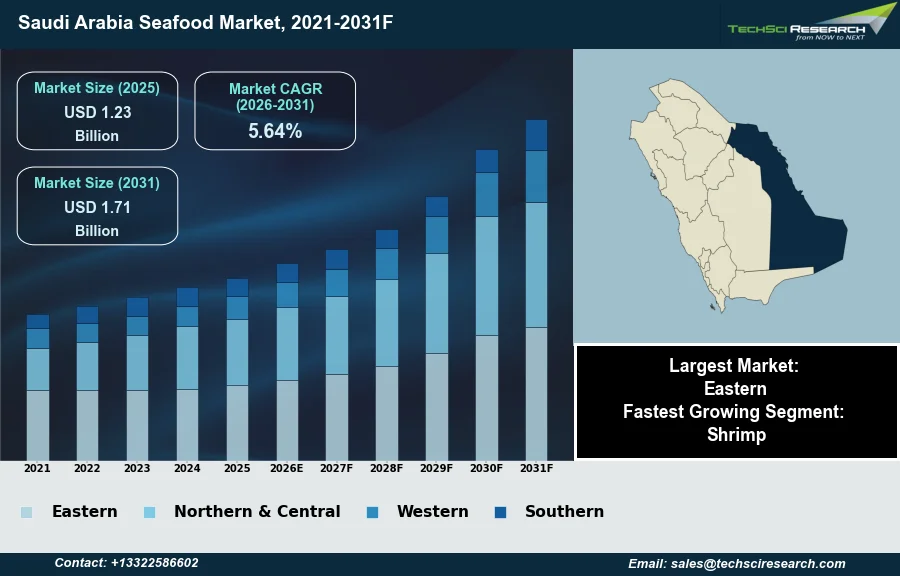

Market Size (2025)

|

USD 1.23 Billion

|

|

CAGR (2026-2031)

|

5.64%

|

|

Fastest Growing Segment

|

Shrimp

|

|

Largest Market

|

Eastern

|

|

Market Size (2031)

|

USD 1.71 Billion

|

Market Overview

The Seafood Market in Saudi Arabia will grow from USD 1.23 Billion in 2025 to USD 1.71 Billion by 2031 at a 5.64% CAGR. Seafood in the Saudi Arabian market encompasses all marine and freshwater aquatic animals harvested for human consumption, including finfish, crustaceans, and mollusks, prepared and consumed in fresh, frozen, or processed forms. The market's expansion is fundamentally driven by a growing population, increasing consumer disposable incomes, and robust governmental initiatives aimed at enhancing food security and domestic aquaculture production. According to the Vice Minister of Environment, Water and Agriculture, as announced in January 2026, aquaculture output surpassed 192,000 tons.

Additionally, a shifting dietary landscape, reflecting a greater preference for diverse protein sources, further supports demand, alongside a burgeoning tourism sector. However, a significant challenge impeding market growth remains the sustainable management of water resources, which is critical for expanding aquaculture operations in an arid climate.

Key Market Drivers

Vision 2030-driven investment reshapes the Saudi seafood market

Government-led Vision 2030 Initiatives and significant aquaculture investment are fundamentally reshaping the Saudi Arabia Seafood Market by strategically directing capital towards enhancing food security and diversifying the economy. The Kingdom's Vision 2030 prioritizes reducing reliance on oil and fostering agricultural self-sufficiency, with aquaculture identified as a key growth sector. These governmental initiatives attract both local and international investors, funding crucial infrastructure development, technological adoption, and research within the aquaculture industry. For instance, according to the Ministry of Environment, Water, and Agriculture, in October 2025, during the Saudi Agricultural Exhibition 2025, over SAR 3.5 billion in total investment agreements were signed, demonstrating robust financial commitment to the sector. This strong governmental push provides a stable regulatory environment and financial incentives, fostering an attractive ecosystem for aquaculture businesses.

Domestic capacity expansion strengthens supply stability and self-sufficiency

The tangible expansion of domestic aquaculture production capacity directly contributes to the market's supply stability and growth. Increased local output reduces dependence on imported seafood, enhancing food security and creating a more resilient supply chain. This expansion involves establishing new farms, upgrading existing facilities, and implementing advanced farming technologies to maximize yield and efficiency. According to Aquafeed.com, in June 2025, citing a USDA Foreign Agricultural Service report, Saudi Arabia's aquaculture output surged to 139,949 tons by 2023, representing 65% of total seafood production, demonstrating substantial progress in self-sufficiency. This growth also benefits from advancements in cold chain logistics and infrastructure, ensuring that freshly harvested seafood reaches consumers efficiently. The overall Saudi Arabian seafood market continues to expand, with consumption patterns evolving. According to OCO Global, in October 2024, citing the Food & Agriculture Organization of the UN (FAO), the Kingdom's per capita fish consumption was around 13.5 kg per year.

Download Free Sample Report

Key Market Challenges

Water scarcity and costs constrain aquaculture growth

The sustainable management of water resources is a critical challenging factor directly impeding the growth of the Saudi Arabia Seafood Market. The inherent aridity of the climate creates a fundamental limitation on expanding domestic aquaculture operations, which are essential for increasing local seafood supply. Acquiring or treating water for aquaculture, whether through desalination or advanced recycling, involves significant capital outlay and ongoing operational expenses. These elevated costs reduce the economic viability of establishing new aquaculture projects and expanding existing facilities, consequently deterring potential investment and slowing the overall development of the sector.

Rising water costs and regulatory requirements constrain expansion amid desalination investment

The high cost of water provision directly translates to increased production costs for seafood, impacting market competitiveness and consumer prices. Furthermore, the stringent requirements for sustainable water use in aquaculture necessitate careful planning and adherence to environmental regulations to prevent resource depletion. This limits the scale at which production can be expanded, even with technological advancements. According to the Saudi Water Authority, in June 2025, a total financing of USD 650 million was allocated to modernize desalination plants, highlighting the substantial financial burden associated with ensuring adequate water supply for various national needs, including industrial and agricultural sectors like aquaculture.

Key Market Trends

Rising Demand for Processed Seafood Drives Capacity Expansion

Rising demand for processed and ready-to-cook seafood represents a significant trend, driven by evolving consumer lifestyles and a growing preference for convenience. As urbanization increases and household structures change, consumers increasingly seek time-saving meal solutions that require minimal preparation. This shift reflects a broader global trend where convenience is a key factor in food purchasing decisions. Reinforcing this trend, Almunajem Foods Company announced in April 2024 its board's approval for establishing a new food factory in Jeddah, with an investment of SAR 157 million, designed to produce 35,000 tonnes annually of various food products, including seafood, thereby enhancing the capacity for processed offerings.

Expansion of Online and Dark Kitchen Seafood Delivery

The expansion of online and dark kitchen seafood delivery services is another prominent trend reshaping the market, fundamentally changing how consumers access seafood. This growth is underpinned by increasing internet penetration and widespread smartphone adoption, which enable seamless digital ordering and home delivery. Consumers increasingly value the convenience of having fresh or prepared seafood delivered directly to their doorstep, bypassing traditional retail or dine-in experiences. The broader delivery sector in Saudi Arabia, which includes food, demonstrated robust growth, recording over 118 million orders in the first quarter of 2026, representing a 49 percent annual increase, according to the Saudi Transport General Authority. This substantial growth in the overall delivery ecosystem creates a fertile ground for the expansion of specialized seafood delivery services and dedicated dark kitchens.

Segmental Insights

Key Drivers of Shrimp Growth in Saudi Arabia

In the Saudi Arabia Seafood Market, shrimp stands out as the fastest-growing segment, driven by several strategic factors. A primary catalyst is the Kingdom's robust commitment to aquaculture development under Vision 2030, with significant support from the Ministry of Environment, Water and Agriculture (MEWA) through initiatives like the Aquaculture Development Program. This governmental push fosters investment in sustainable farming infrastructure and modern cultivation technologies, enhancing local production capabilities. Concurrently, rising consumer health consciousness and a preference for protein-rich, lean seafood options have boosted demand for shrimp. Furthermore, the expanding foodservice and tourism sectors significantly contribute to the increased consumption of shrimp, valued for its culinary versatility.

Regional Insights

Eastern Region: Coastal Hub Driving Supply and Demand

The Eastern region holds a prominent position within the Saudi Arabia seafood market, largely attributable to its extensive coastline along the Arabian Gulf and abundant marine resources, which make it a significant hub for both farmed and wild seafood production. Dammam's strategic proximity to major ports and industrial zones facilitates efficient import and distribution channels across the region and beyond. Furthermore, the presence of numerous licensed fish-farming projects and robust government support, notably from the Ministry of Environment, Water, and Agriculture, underscores its crucial role in enhancing domestic supply and export capabilities. Local consumer preferences for fresh seafood, coupled with a substantial expatriate and industrial workforce, further drive demand in this key area.

Recent Developments

-

In May 2025, MAT-KULING signed a new contract with Saudi Arabia's National Aquaculture Group (NAQUA) for the development of a next-generation Barramundi hatchery. This advanced facility is designed to be the most technologically innovative of its kind within the region, showcasing a commitment to cutting-edge research and development in the Saudi Arabia seafood market. This collaboration supports NAQUA's vision for sustainable expansion and a substantial increase in its production capacity, diversifying the range of locally sourced seafood.

-

In November 2024, the Saudi Fisheries Company announced the spin-off of a new aquaculture entity. This strategic restructuring was undertaken to enhance operational efficiency and focus specifically on sustainable seafood production within the Kingdom. The establishment of this specialized entity is a key component of the government's broader strategy. It aims to substantially increase fish farming output and improve the overall sustainability of the Saudi Arabian seafood sector, reflecting a commitment to local production capabilities.

-

In June 2024, King Abdullah University of Science and Technology (KAUST), in collaboration with the Ministry of Environment, Water, and Agriculture (MEWA), initiated the Aquaculture Development Program. This significant partnership is designed to revolutionize Saudi Arabia's aquaculture landscape. The program anticipates boosting domestic seafood production from 280,000 tons in 2024 to an estimated 530,000 tons annually by 2030, thereby strengthening national food security and research capabilities within the Saudi Arabian seafood market.

-

In February 2024, NEOM and Tabuk Fisheries Company established Topian Aquaculture, a joint venture directly linked to the Saudi Arabia seafood market. This collaboration aims to develop a fish farming operation with a projected output of 20,000 tonnes per year. The initiative includes constructing a hatchery, which is expected to become the largest in the MENA region by the end of 2024. This strategic partnership significantly contributes to Saudi Arabia's national objective of increasing annual fish product output to 600,000 tonnes by 2030, bolstering domestic seafood supply.

Key Market Players

- Saudi Fisheries Company

- National Fishing Company

- Almarai Seafood

- Al Rabie Seafood

- Al Othaim Seafood

- Lulu Seafood

- HyperPanda Seafood

- Carrefour Seafood

- Bin Dawood Seafood

- Amazon.sa Seafood

|

By Product

|

By Type

|

By Application

|

By Distribution Channel

|

By Region

|

- Fish

- Shrimp

- Crab

- Lobster

- Others

|

|

- Retail

- Institution Sales

- Food Service

|

- Supermarket/Hypermarket

- Departmental Stores

- Specialized Stores

- Online

- Others

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Seafood Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Seafood Market, By Product:

-

Fish

-

Shrimp

-

Crab

-

Lobster

-

Others

-

Saudi Arabia Seafood Market, By Type:

-

Saudi Arabia Seafood Market, By Application:

-

Retail

-

Institution Sales

-

Food Service

-

Saudi Arabia Seafood Market, By Distribution Channel:

-

Supermarket/Hypermarket

-

Departmental Stores

-

Specialized Stores

-

Online

-

Others

-

Saudi Arabia Seafood Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Seafood Market.

Available Customizations:

Saudi Arabia Seafood Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Seafood Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com