|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 86.24 Billion

|

|

CAGR (2026-2031)

|

7.81%

|

|

Fastest Growing Segment

|

Non-Food Retail

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 135.41 Billion

|

Market Overview

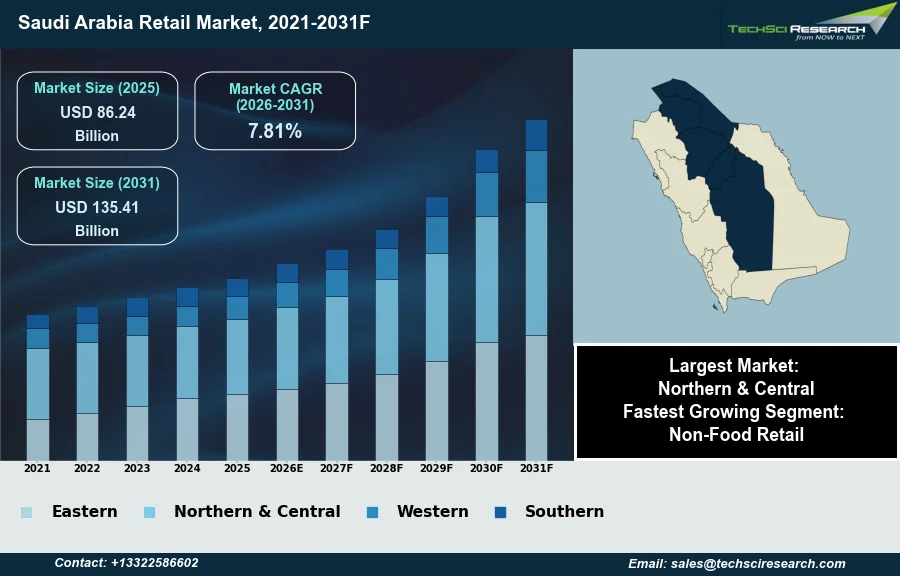

The Retail Market in Saudi Arabia will grow from USD 86.24 Billion in 2025 to USD 135.41 Billion by 2031 at a 7.81% CAGR. The Saudi Arabia Retail Market encompasses the direct sale of goods and services to end-consumers across diverse channels, including traditional brick-and-mortar establishments and rapidly expanding e-commerce platforms. This market's robust growth is primarily driven by ambitious government initiatives under Vision 2030, which foster economic diversification and attract foreign investment. Additionally, a large, youthful population with increasing disposable incomes and substantial government investments in tourism and urban infrastructure significantly bolster consumer spending and market expansion.

Illustrating this trajectory, according to the General Authority for Statistics (GASTAT), in the first quarter of 2026, Saudi Arabia's wholesale and retail trade revenue experienced a year-on-year growth of 7.3%. Despite this positive outlook, a notable challenge for market expansion stems from navigating the evolving regulatory landscape. Retailers must continually adapt to new compliance requirements, particularly regarding data protection and Saudization policies, which can impact operational frameworks.

Key Market Drivers

Vision 2030 Diversification Drives Retail Growth

Vision 2030 Economic Diversification Initiatives represent a fundamental driver for the Saudi Arabia Retail Market, fostering significant structural shifts that support non-oil sector growth. These initiatives aim to reduce the economy's reliance on hydrocarbons by stimulating various sectors, including retail, through strategic investments and regulatory reforms. The focus on developing new cities, expanding tourism, and enhancing infrastructure directly translates into increased consumer bases and demand for retail offerings. Illustrating this diversification, non-oil activities recorded a 2.8% increase year-on-year in the first quarter of 2026, according to the General Authority for Statistics. This sustained growth in non-oil sectors contributes to a more robust and varied economic landscape, directly benefiting retail through enhanced consumer purchasing power and a broader market.

Digital Transformation and E-commerce Fuel Retail Expansion

Accelerated Digital Transformation and E-commerce significantly influence the market by reshaping consumer behavior and expanding retail channels. The Kingdom's young, digitally literate population readily adopts online shopping platforms and digital payment solutions, driving substantial growth in e-commerce. Government support for digital infrastructure and cashless transactions further facilitates this transition, creating a dynamic environment for online retailers. For instance, e-commerce spending via Mada cards recorded a 28% year-on-year increase to SR35.4 billion in March 2026, according to the Saudi Central Bank. This shift towards digital transactions and online retail complements the overall market expansion, which saw consumer spending in Saudi Arabia rise 17.5% year-on-year to SAR 133.9 billion in April 2026, according to Cairo Scene.

Download Free Sample Report

Key Market Challenges

Regulatory Landscape Impeding Growth

The evolving regulatory landscape presents a notable impediment to the Saudi Arabia Retail Market's growth. Retailers face increased complexities in adapting to new compliance requirements, particularly concerning Saudization policies and data protection regulations. These mandates directly impact operational frameworks and financial outlays.

Rising Compliance Costs from Saudization and Data Protection

Saudization policies, which require specific employment quotas for Saudi nationals, significantly elevate operational costs. According to Hays, in 2025, operational costs for most retailers have increased by an estimated 15-25% due to higher wage requirements for Saudi nationals compared to expatriate workers. This surge in labor expenditure necessitates substantial investment in recruitment and training programs to align the workforce with new nationalization targets, straining financial resources, especially for small and medium-sized enterprises. Concurrently, strict adherence to the Personal Data Protection Law mandates considerable investment in data governance and secure infrastructure, diverting capital that could otherwise be allocated to market expansion or technological innovation. These evolving regulations collectively constrain market development by increasing compliance overheads and complicating strategic planning.

Key Market Trends

Immersive Experiential Retail reshapes Saudi shopping landscape

Immersive Experiential Retail is reshaping the Saudi Arabian market by transforming traditional shopping into engaging leisure activities. Retailers are investing in multi-sensory environments that blend shopping with entertainment, dining, and cultural attractions, providing compelling reasons for consumers to visit physical stores. This trend helps differentiate brick-and-mortar establishments from online competition, encouraging longer visits and fostering stronger brand connections through memorable experiences. It addresses a growing consumer desire for social interaction and entertainment within retail settings. According to a February 2026 report on the Saudi Entertainment Industry, between 2024 and 2025 alone, government entities channeled over SAR 50 billion into leisure infrastructure, anchoring numerous entertainment and retail destinations across the Kingdom.

AI-Driven Personalization enhances the Saudi retail experience

AI-Driven Customer Personalization represents another significant trend, as retailers increasingly adopt advanced analytical tools to understand and cater to individual consumer preferences. This involves utilizing artificial intelligence to process extensive customer data, enabling the delivery of highly relevant product suggestions, customized promotions, and tailored service interactions. Such personalization enhances the shopping journey, improves customer satisfaction, and builds loyalty by making each interaction feel unique and relevant to the individual. According to TahawulTech.com, in its May 2026 article 'AI becomes the default for Saudi consumers as Deloitte's 2026 Digital Consumer Trends Report reveals a decisive shift', two-thirds of consumers in Saudi Arabia (66%) now actively use AI tools, indicating strong consumer engagement with AI-powered experiences.

Segmental Insights

Non-Food Retail Drives Saudi Market Expansion Under Vision 2030

The Saudi Arabia Retail Market is experiencing significant expansion, with Non-Food Retail identified as the fastest-growing segment. This acceleration is primarily driven by the Kingdom's Vision 2030 economic diversification initiatives, which stimulate increased consumer spending and attract investments into diverse sectors beyond oil. A youthful, digitally aware population with rising disposable incomes fuels demand for a broader array of products, including international brands, electronics, and fashion, alongside a preference for enhanced shopping experiences. Concurrently, the rapid growth of e-commerce, combined with substantial urbanization and infrastructure development, provides consumers with greater accessibility and a wider selection of non-food retail offerings.

Regional Insights

Northern & Central Region: Core Retail Hub Fueled by Urban Growth and Vision 2030

The Northern & Central region is a pivotal force within the Saudi Arabia Retail Market, primarily driven by its significant urban development and concentrated population. As the nation's administrative and economic center, it encompasses Riyadh, a key urban hub boasting a substantial consumer base with considerable purchasing power. This region features extensive modern retail infrastructure, including numerous large shopping malls and supermarkets, catering to diverse consumer needs. Furthermore, ongoing government initiatives under Vision 2030, which foster economic diversification and infrastructure enhancements, significantly contribute to the region's retail expansion and its role as a central distribution and retail destination.

Recent Developments

-

In October 2025, Lulu Group, a major retail conglomerate, inaugurated its 70th hypermarket in Saudi Arabia, strategically expanding its reach to the city of Taif. The new hypermarket spans nearly 196,000 square feet, offering an extensive selection of products ranging from groceries and electronics to fashion and dining options. This expansion underscores Lulu Group's continuous commitment to strengthening its presence within the Saudi Arabian retail market, enhancing shopping experiences for the local community, and contributing to the Kingdom's economic development and job creation initiatives.

-

In October 2024, Panda Retail Company, a prominent retailer in Saudi Arabia, formed a strategic partnership with the Saudi Company for Artificial Intelligence (SCAI) and Faden Media. This collaboration aims to transform in-store advertising across Panda's retail network by integrating advanced artificial intelligence technologies and comprehensive data analytics. The initiative is designed to offer a more personalized shopping journey for customers and provide brands with deeper insights into consumer behavior. This innovative approach seeks to elevate the advertising experience and improve customer satisfaction within the Saudi Arabian retail sector.

-

In June 2024, Spinneys, a supermarket chain from the United Arab Emirates, made its entry into the Saudi Arabia retail market by opening its first store in Riyadh. Located in the La Strada Yard mixed-use development, the 43,520 square feet store offers a wide array of premium products, including imported goods and locally sourced items, alongside in-house produced bakery, meats, and meal solutions. This launch marks a significant milestone in Spinneys' regional expansion strategy, with plans for three additional stores in Riyadh and Jeddah later in 2024, reinforcing its commitment to the Kingdom's evolving retail landscape.

-

In April 2024, Lulu Group announced its continued expansion within the Saudi Arabia retail market by finalizing two new hypermarket projects in Makkah and Madinah. This initiative involves collaborations with Jabal Omar Development Company for a store within Makkah's Jabal Omar 3 development and with Al Manakha Urban Project Development Company for the Madinah location. These projects are set to significantly enhance Lulu Group's presence and offer an expanded retail experience for customers in these key Saudi Arabian cities, aligning with broader economic development goals. The expansion plans anticipate the creation of 1,000 new employment opportunities, further contributing to the local workforce.

Key Market Players

- Al Othaim Retail

- Lulu Hypermarket

- HyperPanda

- Carrefour KSA

- Bin Dawood

- Amazon.sa

- Jarir Marketing

- Extra Stores

- Alshaya Retail

- Al Hokair Retail

|

By Type

|

By Retail Store Type

|

By Region

|

- Food Retail

- Non-Food Retail

|

- Supermarket/Hypermarket

- Online

- Baqala Stores

- Departmental Stores

- Exclusive Stores

- Convenience Stores

- Others

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Retail Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Retail Market, By Type:

-

Food Retail

-

Non-Food Retail

-

Saudi Arabia Retail Market, By Retail Store Type:

-

Supermarket/Hypermarket

-

Online

-

Baqala Stores

-

Departmental Stores

-

Exclusive Stores

-

Convenience Stores

-

Others

-

Saudi Arabia Retail Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Retail Market.

Available Customizations:

Saudi Arabia Retail Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Retail Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com