|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 89.34 Million

|

|

CAGR (2026-2031)

|

6.51%

|

|

Fastest Growing Segment

|

Disposable Gowns

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 130.43 Million

|

Market Overview

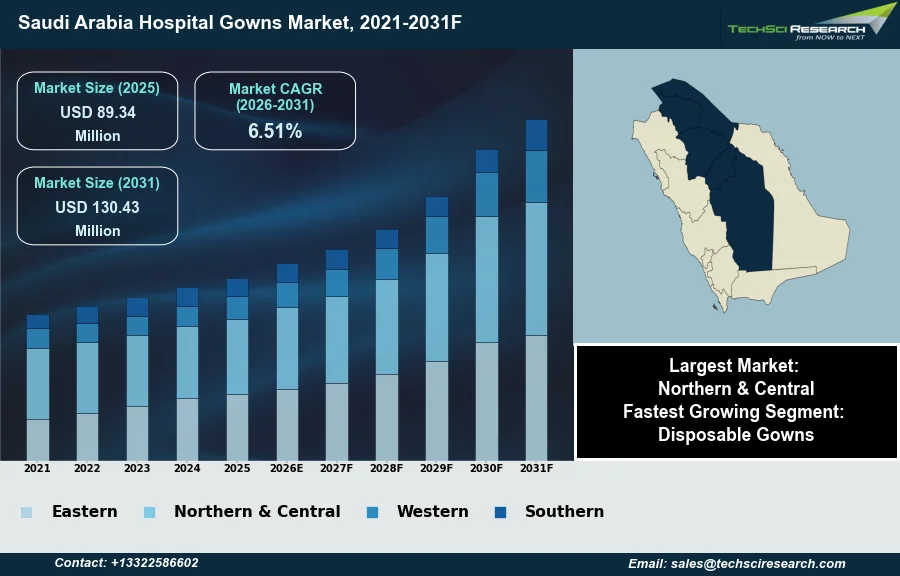

The Saudi Arabia Hospital Gowns Market will grow from USD 89.34 Million in 2025 to USD 130.43 Million by 2031 at a 6.51% CAGR. Hospital gowns are essential medical garments designed to provide a protective barrier for patients and healthcare professionals within clinical environments, facilitating hygiene and infection control during examinations, procedures, and recovery. The Saudi Arabia Hospital Gowns Market is primarily driven by the nation's significant investment in healthcare infrastructure expansion under Vision 2030, an increasing volume of surgical procedures, and a heightened emphasis on stringent infection prevention protocols across medical facilities. Furthermore, the rising prevalence of chronic diseases and an aging population contribute to greater hospital admissions and the subsequent demand for diverse gown types.

According to the Ministry of Finance, in its 2025 official budget, Saudi Arabia allocated SAR 260 billion (approximately USD 69 billion) to the health and social development sector, signaling substantial government commitment to the healthcare ecosystem. This robust financial backing underpins the growth in demand for medical supplies, including hospital gowns. However, a significant challenge impeding market expansion is the substantial reliance on imported medical consumables, which exposes the market to potential supply chain disruptions and currency fluctuations.

Key Market Drivers

Government Investment and Healthcare Expansion Fuel Gown Demand

Government Healthcare Investments and Vision 2030 Initiatives serve as a fundamental catalyst for the Saudi Arabia Hospital Gowns Market. These strategic investments aim to significantly expand the nation's healthcare infrastructure, including the construction of new medical cities, hospitals, and specialized clinics. Such expansion directly translates into an increased demand for essential medical consumables, with hospital gowns being a primary requirement for newly established and upgraded facilities. According to the Saudi Press Agency, February 2026, in its report via Fast Company Middle East, Saudi Arabia has launched healthcare projects valued at more than $266 million in Makkah, which includes the 500-bed Makkah General Hospital. This substantial investment underpins the growth in demand for diverse gown types.

Infection Control Standards and Capacity Expansion Drive Gown Demand

The heightened emphasis on infection prevention and control standards profoundly influences the demand for hospital gowns within Saudi Arabia. Stringent regulations and protocols are being implemented across healthcare institutions to mitigate the risk of healthcare-associated infections (HAIs), thereby necessitating the consistent use of high-quality, often disposable, gowns for both patient and staff protection during examinations, procedures, and routine care. According to the Saudi Press Agency, February 2026, the Ministry of Health reported a 50% reduction in deaths from infectious diseases in its 2025 annual health system report due to enhanced protocols. This focus on improved patient outcomes drives the adoption of gowns that meet rigorous safety and hygiene specifications. Furthermore, according to Knight Frank, in 2026, current bed density in Saudi Arabia stands at 2.0 beds per 1,000 people, indicating an ongoing need for capacity development.

Download Free Sample Report

Key Market Challenges

Import Dependence Elevates Supply-Chain Risk and Costs

The Saudi Arabia Hospital Gowns Market faces a significant impediment to growth due to its substantial reliance on imported medical consumables. This dependency renders the market highly susceptible to global supply chain disruptions, where external factors like geopolitical instability or logistical challenges can impede the timely availability of essential garments, risking operational continuity and compromising patient care. Additionally, fluctuations in international currency exchange rates directly inflate procurement costs for local buyers, increasing expenditure on hospital gowns and potentially constraining budget allocations for other critical healthcare areas.

Import Dependence Undermines Domestic Manufacturing and Economic Growth

According to the Ministry of Investment of Saudi Arabia (MISA), in 2024, over 90% of medical devices and hospital supplies within the Kingdom were imported. This high level of import dependency directly impacts the hospital gowns market by limiting the development of robust domestic manufacturing capabilities. Reduced local production curtails opportunities for internal economic growth, job creation, and the transfer of critical manufacturing expertise, which is a key objective under Vision 2030. This sustained reliance also creates a vulnerability to price volatility, affecting the long-term planning and financial stability of healthcare providers.

Key Market Trends

Localization Drives Domestic Gown Production and Supply-Chain Resilience

The Saudi Arabia Hospital Gowns Market is notably influenced by the increasing localization of medical manufacturing. This trend reflects the Kingdom's strategic imperative under Vision 2030 to bolster domestic production capabilities, thereby reducing reliance on imports and enhancing the resilience of its healthcare supply chain. This shift is driving significant investment into establishing and expanding local facilities for various medical consumables, including hospital gowns. For instance, according to the Saudi Press Agency, January 2026, in its report "Major Investments in Saudi Pharma and Medical Supplies Announced in Jeddah," a medical supplies factory expansion was backed by a SAR220 million investment, specifically aimed at meeting domestic demand and supporting regional exports. This focus on localization directly supports the development of a robust local ecosystem for gown production, fostering self-sufficiency and mitigating risks associated with global supply chain disruptions.

Digitalization of the Gown Supply Chain and Procurement

Another significant trend shaping the market is the digitalization of the healthcare supply chain and procurement for gowns. Healthcare providers in Saudi Arabia are increasingly adopting advanced digital solutions to streamline logistics, enhance transparency, and optimize inventory management for essential medical garments. These systems leverage real-time data and analytics to improve efficiency in the acquisition, distribution, and utilization of hospital gowns. According to the Global Health Exhibition 2024, in its content published December 2025, advanced traceability systems are providing near 100% visibility into medical supply chains, which minimizes shortages and disruptions while aligning with Saudi Arabia's goal of achieving minimum waste by 2030. This digitalization optimizes procurement processes for hospital gowns, ensures consistent availability, and reduces operational inefficiencies.

Segmental Insights

Disposable Gowns: Fastest-Growing Segment Driven by Infection Control and Regulatory Mandates.

The key segmental insight for the Saudi Arabia Hospital Gowns Market reveals that Disposable Gowns are the fastest-growing segment. This rapid expansion is primarily driven by an intensified focus on infection control and patient safety within the Kingdom's healthcare facilities. Strict regulatory protocols issued by the Saudi Ministry of Health mandate the use of high-quality, sterile protective apparel, particularly in surgical and high-risk environments, to mitigate hospital-acquired infections. The inherent convenience and assured sterility of single-use disposable gowns align perfectly with these stringent standards, making them the preferred choice for medical professionals. Furthermore, the ongoing expansion of healthcare infrastructure and increasing surgical volumes further propel the demand for this segment.

Regional Insights

Northern & Central Region Drives Market Leadership through Robust Healthcare Infrastructure

The Northern & Central region leads the Saudi Arabia Hospital Gowns Market due to its robust and concentrated healthcare infrastructure. This region, particularly Riyadh, serves as the core of the national healthcare system, hosting numerous major public and private hospitals, specialized treatment centers, and prominent research institutions. The high concentration of advanced medical facilities, coupled with a significant population density, drives substantial demand for hospital gowns, especially surgical gowns, essential for a large volume of surgical procedures. Furthermore, ongoing government investments and strategic initiatives by the Ministry of Health to expand and modernize healthcare services in these central areas further solidify their market dominance.

Recent Developments

-

In November 2025, the Saudi Fashion Commission unveiled its pioneering Red Sea Seaweed Project, a breakthrough in bio-textile development. This initiative, launched at the Misk Global Forum, introduced a sustainable textile created from marine algae sourced from the Red Sea. The innovative fabric, made from a blend of Lyocell with an algae additive and organic cotton, showcased natural origin and skin-friendly properties. Developed in collaboration with King Abdullah University of Science and Technology (KAUST) and PYRATEX, this research demonstrated a commitment to unlocking new material solutions and promoting a responsible textile sector within the Kingdom. Such advancements in sustainable textile research could eventually offer new material options for the manufacturing of eco-conscious hospital gowns in Saudi Arabia.

-

In October 2025, India and Saudi Arabia deepened their textile partnership, signaling new investment and innovation opportunities. A high-level delegation from Saudi Arabia met with India's Ministry of Textiles to discuss expanding bilateral trade, particularly focusing on Man-Made Fibre (MMF) and technical textiles. This collaboration aimed to strengthen manufacturing linkages and foster mutual growth in the textile and apparel sectors. Given India's role as a major textile exporter to Saudi Arabia, this strategic partnership was expected to drive advancements and increased supply of high-quality, value-added textile products, including specialized fabrics suitable for hospital gowns, within the Saudi Arabian market.

-

In September 2025, the third Saudi Fashion and Textile Expo in Jeddah showcased significant strides in sustainable and innovative textile products. International and local companies presented novel fabrics, yarns, and sustainable fashion products, reflecting a growing interest in the Saudi market. The event emphasized sustainability as a key focus, with exhibitors bringing forward advancements in materials, including recycled polyesters and organic fabrics. These innovations in textile technology, while featured in fashion, represented potential for broader applications in various fabric-based products. Such developments could influence the future design and manufacturing of hospital gowns by introducing more environmentally friendly or performance-enhanced materials to the Saudi Arabian healthcare sector.

-

In July 2025, a significant collaboration was announced between King Faisal Specialist Hospital and Research Center and NUPCO, the National Unified Procurement Company for Medical Supplies, to strengthen Saudi Arabia's medical supply chains. This partnership, solidified by a Memorandum of Understanding, aimed to modernize healthcare procurement systems across the Kingdom. The agreement encompassed developing a digital procurement marketplace, unifying product catalogs, and improving logistics services for medical supplies. These enhancements were intended to boost efficiency and ensure reliable access to a wide range of essential medical products, including hospital gowns, for healthcare facilities nationwide, aligning with national efforts for resilient supply chains.

Key Market Players

- Medline Industries

- Cardinal Health

- Ansell Healthcare

- Halyard Health

- Mölnlycke

- Top Glove

- Hartalega

- Supermax

- Semperit

- Kossan Rubber

|

By Type

|

By Usability

|

By Risk Type

|

By Region

|

- Surgical Gowns

- Non-Surgical Gowns

- Patient Gowns

|

- Disposable Gowns

- Reusable Gowns

|

- Minimal

- Low

- Moderate

- High

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Hospital Gowns Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Hospital Gowns Market, By Type:

-

Surgical Gowns

-

Non-Surgical Gowns

-

Patient Gowns

-

Saudi Arabia Hospital Gowns Market, By Usability:

-

Disposable Gowns

-

Reusable Gowns

-

Saudi Arabia Hospital Gowns Market, By Risk Type:

-

Minimal

-

Low

-

Moderate

-

High

-

Saudi Arabia Hospital Gowns Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Hospital Gowns Market.

Available Customizations:

Saudi Arabia Hospital Gowns Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Hospital Gowns Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com