|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

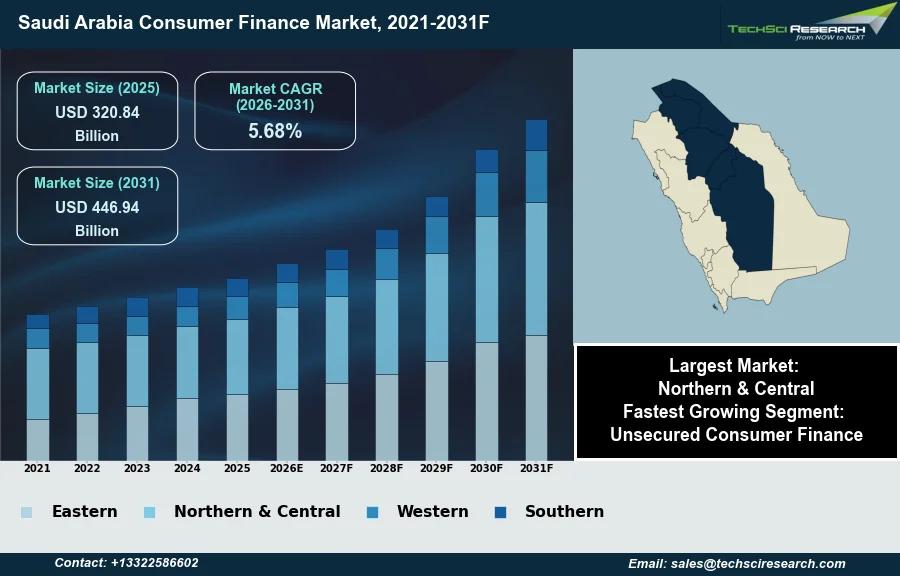

Market Size (2025)

|

USD 320.84 Billion

|

|

CAGR (2026-2031)

|

5.68%

|

|

Fastest Growing Segment

|

Unsecured Consumer Finance

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 446.94 Billion

|

Market Overview

The Saudi Arabia Consumer Finance Market will grow from USD 320.84 Billion in 2025 to USD 446.94 Billion by 2031 at a 5.68% CAGR. The Saudi Arabia consumer finance market broadly defines credit products extended to individuals for personal consumption, including personal loans, vehicle financing, and credit cards. This market's expansion is fundamentally supported by the Kingdom's economic diversification efforts under Vision 2030, a growing young population, and sustained government-backed housing initiatives. Additionally, robust consumer confidence and increasing digitization of financial services act as key drivers.

According to the Saudi Central Bank, personal loans in the Kingdom reached SAR 510.44 billion by the end of the first quarter of 2025, demonstrating substantial market activity. This growth is further propelled by the adoption of digital platforms, with electronic payments constituting 85% of total retail payments in 2025, an increase from 79% in 2024. However, a notable challenge for sustained market expansion lies in the increasing loan-to-deposit ratio, indicating a potential strain on funding as credit growth outpaces deposit accumulation.

Key Market Drivers

Regulatory Support Fuels Fintech Transformation

The accelerated digital transformation and robust fintech innovation are profoundly reshaping the Saudi Arabia consumer finance market by enabling new service delivery channels and expanding financial inclusion. The Saudi Central Bank's proactive regulatory stance, including its open banking program launched in March 2026, fosters a dynamic environment for fintech companies to develop innovative solutions. This supportive ecosystem has driven substantial investment, with Saudi fintech attracting $1.52 billion in total funding by March 2026, signifying strong investor confidence and growth potential in digital financial services. This influx of capital supports the development of advanced payment systems, digital lending platforms, and personalized financial management tools, making consumer finance more accessible and efficient for a wider population. The increasing proliferation of digital solutions streamlines application processes and enhances user experience, catering to the Kingdom's tech-savvy demographic.

BNPL and E-commerce Drive Consumer Finance Growth

The proliferation of e-commerce and Buy Now, Pay Later (BNPL) services significantly fuels the expansion of the Saudi consumer finance market. The rapid adoption of online shopping platforms has created a fertile ground for BNPL solutions, which offer flexible, interest-free installment payment options that resonate with consumer preferences, particularly for Sharia-compliant products. According to AstuteAnalytica India Pvt. Ltd., in January 2026, BNPL market penetration in Saudi e-commerce checkouts hovered around 35-40%, underscoring its integration into mainstream purchasing behavior. This growth is further supported by a youthful population with increasing disposable income and a high propensity for digital transactions. Overall, the Saudi Arabia consumer finance landscape continues to grow, reflecting sustained consumer reliance on credit products to manage purchases and investments. According to the Saudi Central Bank, in March 2026, the country's household debt reached USD 137.4 billion.

Download Free Sample Report

Key Market Challenges

Funding constraints from a rising loan-to-deposit ratio

The increasing loan-to-deposit ratio presents a notable challenge for sustained expansion of the Saudi Arabia consumer finance market. This trend indicates that credit growth is outpacing deposit accumulation, creating a direct strain on the funding liquidity available to financial institutions. A persistently high loan-to-deposit ratio limits banks' capacity to originate new personal loans, vehicle financing, and credit cards, thereby restricting the overall supply of consumer credit in the market. This inherent funding constraint directly impedes market growth by reducing the readily available capital for new lending initiatives.

Deposits growth lags credit growth, signaling liquidity management pressures

This funding pressure is underscored by recent data. According to the Saudi Central Bank (SAMA), total money supply, representing deposits, grew by 8.4% year-on-year to over SAR3.109 trillion by the end of July 2025. In contrast, bank credit extended to the public and private sectors recorded a more substantial annual growth of 15.8% by the end of June 2025. This significant divergence highlights that strong credit demand, when matched by slower deposit growth, compels the banking sector to manage liquidity carefully, impacting its ability to support further expansion in consumer finance product offerings.

Key Market Trends

Rising Sharia-compliant finance reshapes Saudi consumer credit

The growing demand for Sharia-compliant financial products represents a significant trend reshaping the Saudi Arabia consumer finance market, driven by a culturally and religiously conservative populace seeking ethical financial solutions. This trend extends beyond traditional banking to encompass various consumer credit offerings structured to adhere to Islamic principles, thereby fostering trust and engagement among consumers. The increasing preference for such products encourages financial institutions to innovate and expand their Sharia-compliant portfolios, including personal finance, auto loans, and housing finance that avoid interest-based transactions. According to the Saudi Central Bank, January 2026, Shariah-compliant finance contracts in Saudi Arabia reached SAR 2.71 trillion in the third quarter of 2025, marking a 13% year-on-year increase.

AI-driven credit assessment enhances precision and inclusion

Another profound trend influencing the market is the enhanced application of AI and machine learning in credit assessment processes. This technological advancement allows financial institutions to move beyond conventional credit scoring methods by analyzing vast and diverse datasets, leading to more precise risk evaluations and personalized lending decisions. The integration of AI and machine learning also facilitates faster application processing and broader financial inclusion by enabling assessments for individuals with limited traditional credit histories. This shift is crucial for mitigating risks and optimizing portfolio performance in a rapidly evolving market. According to Finastra, February 2026, only one percent of financial institutions in Saudi Arabia report no use or no plans to use artificial intelligence, while 46% prioritize AI for improving accuracy and reducing errors.

Segmental Insights

Unsecured Consumer Finance: Fastest-Growing Segment Driven by Vision 2030 and Fintech Regulation

A key segmental insight for the Saudi Arabia Consumer Finance Market reveals Unsecured Consumer Finance as the fastest-growing segment. This rapid expansion is primarily driven by the Kingdom's Vision 2030 initiatives, which foster economic diversification and enhance financial inclusion across a broad population base. The increasing demand from a young, financially independent demographic, coupled with rising disposable incomes, fuels the uptake of accessible personal loans and credit cards. Furthermore, the robust digital transformation and significant advancements in fintech, actively supported and regulated by the Saudi Central Bank (SAMA) through progressive laws, provide convenient and streamlined access to these unsecured financing options, contributing significantly to their accelerated growth.

Regional Insights

Northern & Central region: Growth engine for Saudi consumer finance under Vision 2030

The Northern & Central region stands as a dominant force in the Saudi Arabia Consumer Finance Market, primarily driven by significant urbanization, sustained population growth, and robust economic development. This prominence is largely attributed to major cities such as Riyadh, which serves as the Kingdom's financial, political, and commercial hub, fostering extensive consumer demand for diverse financial products. Government initiatives under Vision 2030, aimed at improving infrastructure and diversifying the economy beyond oil, further concentrate economic activity and job creation in this central region. The regulatory oversight by the Saudi Central Bank ensures a stable and conducive environment for financial institutions, supporting market expansion and consumer confidence.

Recent Developments

-

In September 2025, the Saudi Central Bank (SAMA) granted a license to Muhlah Zamaniyah for its consumer microfinance activities. This licensing event expanded the number of authorized finance companies operating in Saudi Arabia, specifically bolstering the microfinance segment of the consumer finance market. This development allowed Muhlah Zamaniyah to provide specialized financing solutions, catering to niche and underserved consumer segments. The continuous expansion of licensed finance companies highlights SAMA's commitment to supporting the finance sector, increasing financial transaction efficiency, and promoting financial inclusion aligned with Vision 2030 objectives.

-

In December 2024, D360 Bank commenced its operations as a fully licensed digital-only and Sharia-compliant bank in Saudi Arabia. This launch introduced a new player into the consumer finance market, providing innovative app-based banking services to retail and business customers. The bank offered digital current and savings accounts, cost-effective transfers, and digital payment cards. D360 Bank's entry reflected a growing trend towards digital-first financial experiences, aiming to cater to the tech-savvy population seeking convenient and accessible financial solutions within the Kingdom.

-

In October 2024, a significant collaboration occurred within the Saudi Arabia consumer finance market as the Ministry of Finance formalized an agreement with Al Rajhi Bank, Arab National Bank, and Simplified Financial Solutions Company (SiFi). This partnership aimed to enhance the method of disbursing advances through the expanded use of bank cards. The initiative supports digital transformation efforts and contributes to the Financial Sector Development Program's objectives of increasing digital financial transactions across the Kingdom. This move is aligned with the broader goals of Saudi Vision 2030, which emphasizes improving financial oversight and efficiency.

-

In the second half of 2024, Samsung Pay officially launched its services through the national payment system, "mada," within the Kingdom of Saudi Arabia. This introduction marked a new product offering directly impacting the consumer finance market by expanding digital payment options. The integration of Samsung Pay into the widely utilized mada network provided consumers with increased convenience and security for their retail transactions. This development underscored the continuous progress in Saudi Arabia's payments sector, meeting the evolving needs of individuals and businesses through efficient and secure digital solutions.

Key Market Players

- Saudi National Bank

- Al Rajhi Bank

- Riyad Bank

- Banque Saudi Fransi

- SABB

- Emirates NBD

- HSBC Saudi Arabia

- Arab National Bank

- Alinma Bank

- Samba Financial Group

|

By Type

|

By Region

|

- Unsecured Consumer Finance

- Secured Consumer Finance

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Consumer Finance Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Consumer Finance Market, By Type:

-

Unsecured Consumer Finance

-

Secured Consumer Finance

-

Saudi Arabia Consumer Finance Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Consumer Finance Market.

Available Customizations:

Saudi Arabia Consumer Finance Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Consumer Finance Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com