|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

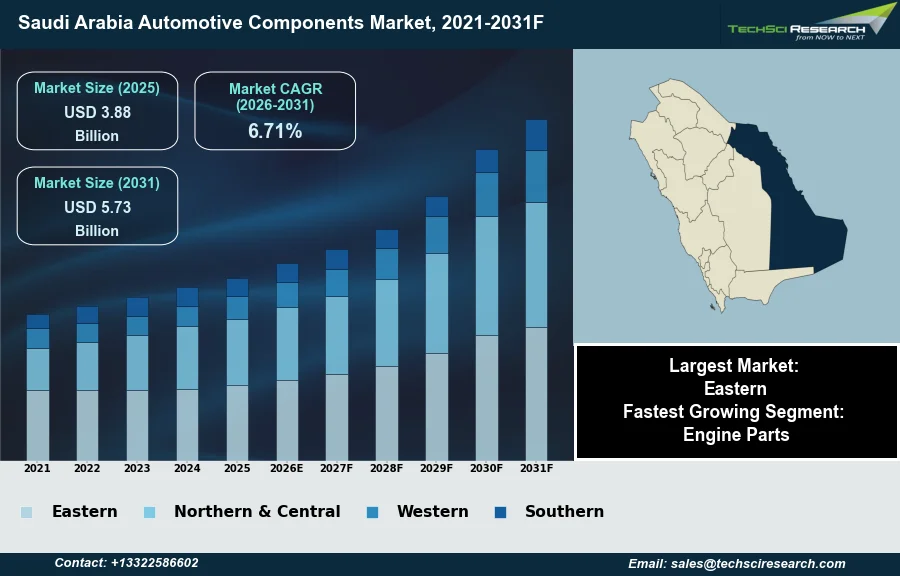

Market Size (2025)

|

USD 3.88 Billion

|

|

CAGR (2026-2031)

|

6.71%

|

|

Fastest Growing Segment

|

Engine Parts

|

|

Largest Market

|

Eastern

|

|

Market Size (2031)

|

USD 5.73 Billion

|

Market Overview

The Saudi Arabia Automotive Components Market will grow from USD 3.88 Billion in 2025 to USD 5.73 Billion by 2031 at a 6.71% CAGR. Automotive components encompass parts and systems used in vehicle manufacturing, assembly, maintenance, and repair, including engine, chassis, electrical, and interior elements. The Saudi Arabia Automotive Components Market is experiencing significant expansion, primarily driven by Vision 2030 economic diversification initiatives and a concerted localization push to reduce import dependence. According to the Saudi Ministry of Industry in 2025, the Kingdom reported 160 automotive-related factories, including 33 dedicated auto-parts plants. Rising vehicle ownership and expanding infrastructure development further support this market's growth.

A substantial challenge impeding market expansion is the heavy reliance on imported components due to an underdeveloped local manufacturing ecosystem. Despite governmental efforts, the domestic sector faces hurdles such as high capital requirements and a scarcity of advanced research and development infrastructure, making significant localization a long-term prospect.

Key Market Drivers

Policy-driven localization and domestic manufacturing

Vision 2030 and automotive localization mandates represent a primary driver for the Saudi Arabia Automotive Components Market. This strategic national initiative aims to reduce import reliance by fostering a robust domestic manufacturing ecosystem for vehicles and their constituent parts. Efforts are concentrated on attracting foreign direct investment and establishing joint ventures to build local capabilities. For instance, according to Ceer, in February 2025, the company secured SAR 5.5 billion (approximately $1.4 billion) in agreements for vehicle parts and equipment, with over 80% sourced from Saudi firms, reinforcing its 45% localization target. This government-led push directly influences component demand by stipulating local content requirements for new vehicle production within the Kingdom, thereby incentivizing investment across the automotive supply chain.

EV-led transition and local component demand

Simultaneously, the technological integration and electric vehicle (EV) shift are significantly shaping the market. The Kingdom is actively transitioning towards sustainable mobility solutions, which necessitates the development of new component manufacturing capabilities, particularly for EV powertrains, batteries, and advanced electronics. According to Arab Wheels, in January 2026, Lucid Motors is slated to begin full-scale electric vehicle production at its Jeddah factory by late 2026, aiming for an annual capacity of 150,000 vehicles by 2029. This move establishes a foundational demand for locally sourced EV components. Overall, the Saudi automotive sector demonstrates strong market potential, with Saudi Arabia being the largest light vehicle market in MENA with 791,000 vehicles sold in 2024, according to Invest Saudi.

Download Free Sample Report

Key Market Challenges

Import Dependence and Underdeveloped Local Manufacturing

The Saudi Arabia Automotive Components Market faces a significant challenge due to its heavy reliance on imported components and an underdeveloped local manufacturing ecosystem. This dependency directly impedes market growth by exposing the industry to global supply chain vulnerabilities, increased transportation costs, and foreign exchange rate fluctuations. Such external factors can lead to higher operational expenses for automotive manufacturers and aftermarket service providers within the Kingdom, ultimately impacting consumer prices and market competitiveness.

Weak Domestic Supplier Network and High Import Share

The absence of a robust domestic supplier network hinders local value creation and limits opportunities for technology transfer and skill development. According to TradeInt, in 2025, Saudi Arabia's imports for "Vehicles & auto parts (HS 87)" reached $15.60 billion, underscoring the substantial volume of components sourced from international markets. This reliance means that despite governmental initiatives aimed at localization, the domestic sector continues to grapple with foundational hurdles, making the establishment of a comprehensive local ecosystem a prolonged endeavor.

Key Market Trends

Digital Transformation and E-Commerce Growth in Saudi Automotive Components

Digital transformation across aftermarket channels represents a significant trend, reshaping how automotive components are distributed, sold, and maintained within Saudi Arabia. The increasing proliferation of online platforms and digital solutions is revolutionizing component accessibility for both workshops and individual consumers, moving away from traditional physical retail models. This shift facilitates real-time inventory checks, seamless transactions, and efficient delivery services, thereby streamlining the supply chain for various parts. This transformation is part of a broader e-commerce acceleration, with the statistical bulletin issued by the Saudi Central Bank in May 2025 reporting that e-commerce sales via "Mada" cards during the first quarter of 2025 reached over SAR69.3 billion, an annual growth of 56% compared to the same period in 2024. This substantial growth underscores the expanding digital engagement that influences customer expectations and operational strategies for component suppliers and service providers.

Sustainability and Circular Economy Initiatives in Automotive Components

The integration of sustainable and circular economy practices is another pivotal trend influencing the Saudi Arabia Automotive Components Market. This trend emphasizes reducing waste, maximizing resource utilization, and promoting the recycling and remanufacturing of components throughout their lifecycle. Efforts are focused on encouraging the adoption of eco-friendly materials and designing components for durability and recyclability, aligning with the Kingdom's broader environmental objectives. This strategic push is evidenced by initiatives like the Ministry of Industry and Mineral Resources' Acceleration Circular Economy Initiative, which aims to implement circular economy concepts in eighty factories over two years, focusing on the central and western regions. Such programs are fostering a new industrial environment where sustainability considerations directly impact component manufacturing processes, material selection, and end-of-life management, thereby reducing environmental impact and creating new value streams.

Segmental Insights

Drivers of Engine Parts Demand: Aging Fleet, Harsh Climate, and Regulatory Oversight

In the Saudi Arabia Automotive Components Market, the Engine Parts segment is notably the fastest growing. This expansion is driven by the Kingdom's aging vehicle fleet, which inherently increases demand for replacement engine components due to extended usage and wear. The harsh climate, marked by extreme heat and dust, also accelerates the degradation of engine parts, necessitating more frequent maintenance and replacements. Additionally, increased vehicle utilization and stringent regulatory frameworks, including mandatory periodic technical inspections overseen by the General Directorate of Traffic and quality standards enforced by the Saudi Standards, Metrology and Quality Organization (SASO), ensure consistent demand for high-quality, compliant engine components.

Regional Insights

Eastern Province: Strategic Automotive Hub Fueled by Port Access, Oil & Gas Activity, and Industrial Growth

The Eastern Province stands as a leading region within the Saudi Arabia automotive components market, propelled by its strategic importance and robust industrial foundation. Its coastal location, particularly the presence of King Abdulaziz Port in Dammam, establishes a critical entry point for automotive imports, significantly enhancing parts availability and distribution efficiency across the Kingdom. This dominance is firmly rooted in its role as a key oil and gas hub, accommodating extensive operations for Saudi Aramco and numerous petrochemical facilities that necessitate large vehicle fleets, thereby creating substantial demand for both original equipment and aftermarket components. Furthermore, ongoing industrial expansion and population growth in major urban centers like Dammam, Khobar, and Jubail, along with developments such as the King Salman Energy Park and Jubail Industrial City, consistently generate considerable demand for passenger and commercial vehicle aftermarket services.

Recent Developments

-

In November 2025, a memorandum of understanding was signed between Saudi Arabia's Ministry of Investment, the National Industrial Development Center, Stellantis, and its local partner, Petromin Corporation. This agreement outlined a feasibility study for establishing a comprehensive vehicle manufacturing plant within the Kingdom. The proposed facility is intended to produce both passenger and commercial vehicles, with a strategic focus on increasing localization rates across the automotive supply chain in Saudi Arabia.

-

In February 2025, Ceer, Saudi Arabia's first electric vehicle brand, announced 11 new partnerships valued at SAR 5.5 billion (approximately $1.5 billion) at the Public Investment Fund Public Sector Forum. The majority of these agreements were established with Saudi companies to supply Ceer with essential vehicle components and charging equipment. These collaborations underscore Ceer's commitment to achieving a 45 percent localization target for its manufacturing operations, significantly contributing to the expansion and stimulation of the Saudi automotive sector in alignment with the goals of Saudi Vision 2030.

-

In June 2024, Ceer finalized a significant contract worth SAR 8.2 billion (approximately USD 2.18 billion) with Hyundai Transys. This agreement secures the supply of Hyundai Transys' innovative "three-in-one" integrated electric drive system for Ceer's electric vehicles. The advanced system combines the electric motor, inverter, and reduction gear into a single unit, which aims to reduce size, weight, and cost while enhancing power efficiency. This partnership represents a key development in the technological capabilities and component sourcing for electric vehicle manufacturing in Saudi Arabia.

-

In 2025, Hyundai Motor Manufacturing Middle East, a joint venture between the Public Investment Fund and Hyundai, commenced construction on its first manufacturing facility in the Middle East. Located within the King Salman Automotive Cluster at King Abdullah Economic City, this plant is designed to produce 50,000 gas and electric vehicle units annually, with operations projected to begin in the fourth quarter of 2026. This initiative is expected to support the localization of automotive components and foster skill development within Saudi Arabia's growing automotive industry.

Key Market Players

- Bosch KSA

- Continental KSA

- Denso KSA

- Honeywell KSA

- Infineon KSA

- NXP KSA

- Sensata KSA

- TE Connectivity KSA

- Valeo KSA

- Delphi KSA

|

By Vehicle Type

|

By Component

|

By Demand Category

|

By Region

|

- Passenger Car

- Commercial Vehicle

|

- Engine Parts

- Body & Chassis

- Suspension & Brakes

- Drive Transmission & Steering Parts

- Electrical Parts and Equipment

|

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Automotive Components Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Automotive Components Market, By Vehicle Type:

-

Passenger Car

-

Commercial Vehicle

-

Saudi Arabia Automotive Components Market, By Component:

-

Engine Parts

-

Body & Chassis

-

Suspension & Brakes

-

Drive Transmission & Steering Parts

-

Electrical Parts and Equipment

-

Saudi Arabia Automotive Components Market, By Demand Category:

-

Saudi Arabia Automotive Components Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Automotive Components Market.

Available Customizations:

Saudi Arabia Automotive Components Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Automotive Components Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com