|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 456.78 Million

|

|

CAGR (2026-2031)

|

8.91%

|

|

Fastest Growing Segment

|

EV Battery

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 762.28 Million

|

Market Overview

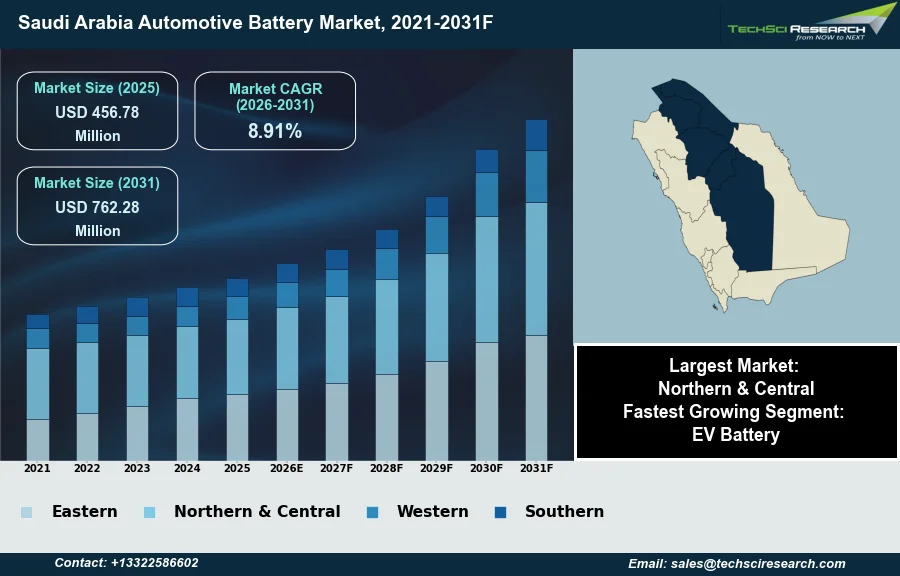

The Saudi Arabia Automotive Battery Market will grow from USD 456.78 Million in 2025 to USD 762.28 Million by 2031 at a 8.91% CAGR. The Saudi Arabia automotive battery market pertains to components supplying electrical power for vehicle ignition, lighting, and accessories across diverse vehicle types, including traditional and hybrid electric models. Market expansion is propelled by an increasing national vehicle fleet, higher vehicle ownership driven by population growth, and strategic Vision 2030 initiatives promoting automotive sector localization and economic diversification. Furthermore, the region's harsh climatic conditions accelerate battery wear, thus sustaining aftermarket replacement demand.

According to the International Organization of Motor Vehicle Manufacturers, in 2025, new vehicle sales in Saudi Arabia reached 827,544 units, representing a 2.80% increase from 2024, which directly influences original equipment battery demand. However, a significant impediment to market growth is the considerable reliance on imported automotive components due to a nascent domestic manufacturing ecosystem, potentially impacting supply chain stability and overall market efficiency.

Key Market Drivers

Growing vehicle fleet and climate-driven battery demand

The expanding vehicle parc in Saudi Arabia significantly drives demand within the automotive battery market, particularly for replacement units. The Kingdom’s harsh climatic conditions, characterized by high temperatures, accelerate battery degradation, necessitating more frequent replacements for the diverse vehicle fleet. This environmental factor, coupled with overall growth in vehicle ownership and utilization, sustains a robust aftermarket for various battery types. According to the Saudi Zakat, Tax and Customs Authority (ZATCA), vehicle imports to Saudi Arabia reached approximately 959,403 units by 2025, contributing substantially to the expanding number of vehicles on the roads and, consequently, the sustained demand for replacement batteries.

Policy and investment initiatives accelerating EV manufacturing and battery demand

Government-led initiatives for electric vehicle (EV) adoption and localized manufacturing profoundly reshape the Saudi Arabia automotive battery market. Vision 2030 aims to establish the Kingdom as a regional automotive hub, with a strong focus on developing domestic EV production capabilities and infrastructure. For instance, according to the Ministry of Industry and Mineral Resources, in February 2025, a joint venture between the Public Investment Fund and Hyundai Motor Company initiated construction of a vehicle manufacturing plant with an investment exceeding $500 million, targeting an annual production capacity of 50,000 vehicles, integrating both internal combustion engine and electric vehicle production. Such investments foster demand for original equipment and advanced battery technologies. This governmental support is further underscored by broader economic goals; according to Saudipedia, by the end of 2025, the Public Investment Fund aimed to inject at least SAR150 billion annually into the local economy, contributing to overall industrial diversification.

Download Free Sample Report

Key Market Challenges

Import Dependence Impedes Saudi Automotive Battery Growth

The Saudi Arabia automotive battery market's growth is significantly hampered by its substantial reliance on imported automotive components, attributed to a nascent domestic manufacturing ecosystem. This dependency creates inherent vulnerabilities in the supply chain, subjecting the market to international logistical complexities, volatile global pricing, and potential disruptions. A limited local production capacity for automotive batteries and their constituent parts means the market cannot adequately buffer against external shocks. This also leads to increased operational expenditures for market participants through import duties, higher transportation costs, and currency fluctuations. According to the Saudi General Authority for Statistics, imports of vehicles, aircraft, vessels, and related transport equipment collectively amounted to SAR 129.6 billion in 2025. This considerable import volume reflects the underdeveloped indigenous manufacturing capabilities, directly impacting the automotive battery sector by restricting local sourcing and elevating overall market costs.

Key Market Trends

Strengthening resilience through domestic production and local sourcing

The Saudi Arabia automotive battery market is significantly influenced by the accelerating trend of domestic production and local sourcing of battery components. This strategic shift aims to reduce the Kingdom's reliance on imported components, thereby strengthening supply chain resilience and fostering industrial self-sufficiency. Local manufacturing initiatives are crucial for supporting the burgeoning electric vehicle sector and broader energy storage goals. For instance, according to MEED, in June 2026, China's ZOE Energy Storage signed a joint venture to establish Saudi Arabia's first large-scale battery energy storage manufacturing facility, with its first phase targeting an annual production capacity of 6 gigawatt-hours by the first quarter of 2027. This development not only contributes to economic diversification but also facilitates technology transfer and skill development within the local workforce, creating a robust indigenous battery industry.

Circular economy in battery lifecycle management

Another prominent trend shaping the market is the increasing integration of circular economy principles for battery lifecycle management. This involves initiatives focused on sustainable sourcing of raw materials, repurposing, and recycling of end-of-life batteries to minimize environmental impact and recover valuable resources. Such efforts are vital for addressing resource scarcity and ensuring sustainable growth of the automotive and energy storage sectors. According to Aramco, in January 2025, Aramco and Ma'aden announced the signing of non-binding Heads of Terms for a minerals exploration and mining joint venture, focusing on energy transition minerals, including extracting lithium from high-concentration deposits with commercial production potentially commencing by 2027. This initiative supports a more sustainable closed-loop system for battery materials, thereby enhancing the long-term viability and environmental footprint of the automotive battery market in the Kingdom.

Segmental Insights

Fastest-Growing EV Battery Segment Fueled by Vision 2030 and Infrastructure Expansion

In the Saudi Arabia Automotive Battery Market, the Electric Vehicle (EV) Battery segment stands out as the fastest-growing. This rapid expansion is primarily driven by the nation's ambitious Saudi Vision 2030, which prioritizes economic diversification, reduced oil dependence, and environmental sustainability. Consequently, the government, through entities like the Public Investment Fund (PIF), is making substantial investments in electric vehicle initiatives, including incentives for EV adoption and fostering local manufacturing capabilities for EVs and their batteries. Concurrently, significant resources are being allocated to expand charging infrastructure, exemplified by the Electric Vehicle Infrastructure Company (EVIQ), which is deploying numerous charging points across the Kingdom to support widespread EV adoption and mitigate range anxiety.

Regional Insights

Northern & Central Region Drives Saudi Arabia Automotive Battery Market Leadership

The Northern & Central region demonstrably leads the Saudi Arabia Automotive Battery Market due to several interconnected factors. This dominance stems primarily from rapid urbanization and a dense population base concentrated in key administrative and commercial hubs like the capital city, Riyadh. The region's strategic position and economic vitality foster significant vehicle demand, supported by a concentration of wealth, corporate headquarters, and extensive residential developments. Additionally, ongoing infrastructure development projects, including new highways and smart city initiatives, contribute to a high demand for both personal and commercial vehicles. The presence of a well-established industrial infrastructure and robust automotive retail ecosystem, coupled with accessible vehicle financing options, further solidifies Northern & Central's leading position in the market.

Recent Developments

-

In April 2025, Saudi Aramco and BYD, a prominent manufacturer of new energy vehicles and power batteries, agreed to explore closer collaboration on new energy vehicle technologies. A joint development agreement was signed by Saudi Aramco Technologies Company, a wholly owned subsidiary of Aramco, and BYD, aiming to foster the development of innovative technologies that enhance efficiency and environmental performance. This collaboration leverages the research and development capabilities of both global companies to achieve breakthroughs, directly supporting the advancement of automotive battery systems within Saudi Arabia and its sustainability objectives.

-

In January 2025, Saudi Aramco Oil Company and Saudi Arabian Mining Company (Ma'aden) signed non-binding Heads of Terms to establish a joint venture. This collaboration focuses on lithium extraction from high-concentration deposits and recycled batteries, directly impacting the automotive battery market in Saudi Arabia. The companies plan to achieve commercial production by 2027, utilizing advanced direct lithium extraction technologies at the Ghawar oil field, which is a key step in developing a domestic supply chain for critical battery raw materials.

-

In January 2025, Lucid Motors announced that its upcoming Gravity electric SUV would incorporate Panasonic Energy's latest-generation high-performance electric vehicle batteries. This product development holds significance for the Saudi Arabia automotive battery market, considering Lucid operates a manufacturing plant in the Kingdom where it assembles and intends to fully produce electric vehicles. The integration of these advanced batteries aims to provide the Gravity SUV with an extended driving range and enhance its overall performance within the region's expanding EV infrastructure.

-

In October 2024, Ceer, Saudi Arabia's inaugural electric vehicle brand, entered a significant partnership with Rimac Technology to source high-performance, fully integrated electric drive systems for its flagship electric vehicle models. This collaboration marks Rimac's first venture into Gulf-scale production, expanding its portfolio beyond hypercars to include mass-market applications. The agreement directly contributes to the technological capabilities and component sourcing for electric vehicles and their associated battery systems manufactured in Saudi Arabia, supporting the Kingdom's evolving automotive industry.

Key Market Players

- Bosch Battery KSA

- Exide KSA

- Amaron KSA

- GS Yuasa KSA

- Al Futtaim Battery

- Al Habtoor Battery

- Al Tayer Battery

- Local Battery Suppliers KSA

- Al Rajhi Battery

- Manlift Battery

|

By Type

|

By Vehicle Type

|

By Battery Type

|

By Region

|

- Starter Battery

- EV Battery

|

- Passenger Cars

- Light Commercial Vehicles

- Two-Wheeler

|

- Lead Acid

- Lithium Ion

- and Others

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Automotive Battery Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Automotive Battery Market, By Type:

-

Starter Battery

-

EV Battery

-

Saudi Arabia Automotive Battery Market, By Vehicle Type:

-

Passenger Cars

-

Light Commercial Vehicles

-

Two-Wheeler

-

Saudi Arabia Automotive Battery Market, By Battery Type:

-

Lead Acid

-

Lithium Ion

-

and Others

-

Saudi Arabia Automotive Battery Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Automotive Battery Market.

Available Customizations:

Saudi Arabia Automotive Battery Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Automotive Battery Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com