|

Forecast

Period

|

2026-2030

|

|

Market

Size (2024)

|

USD

4.68 Billion

|

|

Market

Size (2030)

|

USD

7.49 Billion

|

|

CAGR

(2025-2030)

|

8.11%

|

|

Fastest

Growing Segment

|

Plastics

& Polymers

|

|

Largest

Market

|

West

India

|

Market Overview

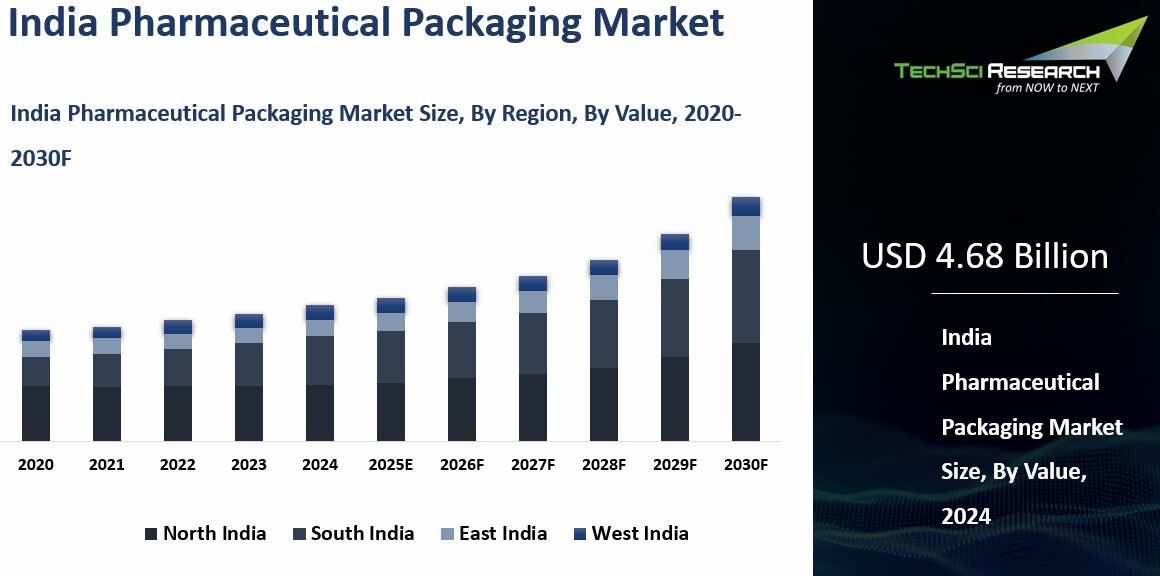

The India Pharmaceutical Packaging Market was valued at USD 4.68 billion in 2024 and is expected to reach USD 7.49 billion by 2030, growing with a CAGR of 8.81% in the forecast period.

The pharmaceutical packaging market in India has grown significantly in recent years and is forecast to continue its upward

trajectory. The expansion of the healthcare sector in India, coupled with an

increasing number of pharmaceutical manufacturing units and higher healthcare

spending, serves as a key catalyst for this market’s growth. The market is set

for continued expansion, fueled by ongoing developments within the

pharmaceutical industry, advancements in packaging technologies, and rising

demand for healthcare products.

Companies

in this sector are increasingly focusing on innovation, sustainability, and

adhering to rigorous regulatory standards to leverage emerging opportunities.

These factors are shaping a competitive environment where companies are

investing in cutting-edge solutions to enhance safety, product integrity, and

supply chain efficiency. The Indian pharmaceutical packaging market is

positioned for robust growth, presenting significant opportunities for both

established market leaders and new entrants seeking to capitalize on the

evolving landscape of the pharmaceutical industry.

Download Free Sample Report

Key Market Drivers

Expansion of the

Pharmaceutical Industry

The expansion of India’s pharmaceutical industry is directly accelerating demand for high quality pharmaceutical packaging because the country is the third largest pharmaceutical producer by volume, supplies about 20 percent of global generic medicines, provides 55 to 60 percent of UNICEF’s vaccine needs, and exports medicines to around 200 countries and territories, all of which increase the volume of products that must be protected, preserved, and shipped in compliant packaging formats.

This growing output spans generics, vaccines, OTC products, and increasingly sensitive formulations, which raises the need for specialized blister packs, bottles, laminates, aseptic packs, tamper evident features, and contamination resistant formats that can meet stricter domestic and export quality requirements. Regulatory pressure is also reshaping packaging choices, as India mandated QR codes on the top 300 pharmaceutical brands to help curb counterfeit medicines and improve product traceability for inspectors and consumers.

For instance, UFlex says its Sanand aseptic packaging facility in Gujarat has capacity for 7 billion packs annually, while the company also stated in FY25 updates that debottlenecking would raise annual output at the plant to 12 billion packs, showing how large packaging companies are scaling infrastructure and security oriented solutions in step with India’s expanding pharmaceutical production and compliance demands.

Technological Advancements in

Packaging Materials

Technological advancements in packaging materials are becoming a major growth catalyst for the Indian pharmaceutical packaging market because drug makers increasingly need solutions that preserve product stability, improve traceability, and align with tighter sustainability expectations across domestic and export supply chains.

Advanced barrier materials are playing a central role in this shift, with UFlex introducing specialty high barrier polyester film with an oxygen transmission rate of less than 6 cubic centimeters per square meter per day and also developing pharmaceutical strip pack laminates with holography based brand protection while maintaining required barrier performance and regulatory conformity for pharma applications.

Smart packaging is also becoming compliance driven in India, as CDSCO’s official FAQs state that the top 300 pharmaceutical brands covered under the 2022 notification must carry a barcode or QR code for authentication and product identification, directly pushing wider adoption of coding and track and trace systems. Sustainability is gaining equal weight, with Amcor’s recyclable AmSky blister system removing PVC from pharmaceutical blister packaging and delivering up to 70 percent lower carbon footprint than typical alternatives while remaining child resistant and senior friendly for regulated healthcare use.

For instance, UFlex says its pharmaceutical packaging operations are supported by state of the art packaging facilities at multiple locations in India with installed capacity of around 1,35,000 tonnes per annum and certifications including ISO 9001, ISO 14001, HACCP, and BRC, showing how major companies are scaling high quality manufacturing infrastructure to support more advanced, compliant, and efficient pharmaceutical packaging in India.

Rising Healthcare Expenditure

Rising healthcare expenditure in India is becoming a strong driver of pharmaceutical packaging demand because higher public spending is expanding treatment access, increasing medicine utilization, and raising expectations for safer, more compliant primary and secondary packaging across the care continuum.

The National Health Accounts for 2021 to 2022 show that Government Health Expenditure reached Rs. 4,34,163 crore, equivalent to 1.84 percent of GDP and 48 percent of total health expenditure, up from 1.13 percent of GDP in 2014 to 2015, which indicates a broader healthcare system now handling larger volumes of packaged medicines, injectables, and hospital consumables.

This demand is being amplified by large public care platforms, as AB PMJAY had created 43.52 crore Ayushman cards and empanelled 36,229 hospitals by February 28 2026, expanding patient flow through organized facilities that require dependable bottles, blister packs, vials, ampoules, and specialty packs for chronic therapies, emergency care, and inpatient treatment. At the same time, the growing use of vaccines, injectables, and biologics is pushing the market toward higher performance packaging that offers stronger barrier protection, sterility assurance, and cold chain resilience.

For instance, Borosil’s pharmaceutical packaging business states that its Klasspack facility has installed capacity of more than 450 million glass ampoules and over 165 million glass vials annually, illustrating how manufacturers are scaling advanced packaging infrastructure to serve rising healthcare utilization and the need for safer drug delivery formats in India.

Key Market Challenges

Stringent Regulatory

Compliance and Standards

Regulatory complexity remains a meaningful challenge for India’s pharmaceutical packaging industry because manufacturers supplying both domestic and export markets must align packaging formats, labeling, traceability, and quality systems with increasingly stringent requirements designed to improve safety and authenticity across the drug supply chain.

This burden has intensified as India made QR code or barcode based identification mandatory for the top 300 drug brands and also mandated machine readable QR codes for all active pharmaceutical ingredients at every level of packaging, adding new compliance steps across primary, secondary, and tertiary packs. The transition is not equally easy for all players, since DTAB discussions cited by industry reporting noted that many pharmaceutical companies had expressed inability to introduce such sophisticated technology into their manufacturing processes, underscoring the operational and cost pressure that evolving rules can create, particularly for smaller firms with limited resources.

For instance, Bilcare’s 2023 to 2024 annual reporting shows how packaging suppliers must keep investing in systems such as ISO 14001 2015, ISO 45001 2018, BIS 17658 2021 applicability work, and continuous R and D for innovative packaging solutions for global pharma customers, demonstrating that regulatory compliance in India is no longer a one time exercise but an ongoing technology and quality investment challenge.

High Raw Material Costs and

Supply Chain Challenges

The

rising cost of raw materials used in pharmaceutical packaging, such as

plastics, glass, and specialized films, is a significant challenge faced by

packaging manufacturers in India. The prices of raw materials are influenced by

global supply chain disruptions, fluctuations in petroleum prices, and a

reliance on imports for certain specialized packaging materials. These cost

pressures are often passed down the supply chain, increasing the overall cost

of packaging and making it harder for manufacturers to offer affordable

solutions, especially in a price-sensitive market like India.

In

addition to raw material costs, supply chain inefficiencies further exacerbate

the situation. The lack of robust infrastructure in some regions, coupled with

logistical challenges, can lead to delays in sourcing materials, production,

and distribution. For pharmaceutical packaging companies, these inefficiencies

can result in prolonged lead times, unpredictable supply costs, and inventory

management challenges. This creates market instability, making it harder

for manufacturers to plan, manage costs, and scale operations in line with

growing demand.

Key Market Trends

Increased Adoption of Smart

and Connected Packaging

The adoption of smart and connected packaging is emerging as a defining trend in India’s pharmaceutical packaging market because manufacturers are under growing pressure to improve drug safety, patient authentication, and supply chain transparency across increasingly complex distribution networks.

This shift has moved beyond theory into regulation, as the Ministry of Health notification cited by GS1 India requires the top 300 pharmaceutical brands to carry a barcode or QR code on primary or secondary packaging, while CDSCO’s implementation FAQs made the requirement effective from August 1 2023 and specified that consumers must be able to verify details such as product name, batch number, expiry date, and manufacturer identity.

India has also mandated QR code based labeling for all active pharmaceutical ingredients, widening track and trace expectations beyond finished formulations and adding another layer of compliance across the packaging value chain. At the company level, packaging suppliers are responding with more advanced anti counterfeiting formats, with UFlex highlighting multi level embossed QR codes, holographic blister foils, lidding foils, and UV sensitive security elements designed specifically for pharmaceutical brand protection and supply chain authenticity.

Sustainability and

Eco-friendly Packaging Innovations

Sustainability is becoming a central focus in India’s pharmaceutical packaging market, driven by regulatory pressure and rising demand for eco-friendly solutions. Growing concerns over plastic waste and the push toward a circular economy are encouraging companies to adopt environmentally responsible packaging practices.

Innovations in materials such as biodegradable plastics, recycled PET (rPET), and plant-based alternatives are gaining traction, offering improved recyclability and reduced environmental impact. These solutions also enhance brand reputation, especially as global consumers increasingly prioritize sustainability. In India, this shift is further supported by investments in recycling infrastructure and collaborations with waste management firms. As sustainability becomes a key design criterion, the pharmaceutical packaging market is expected to transition toward greener materials and processes in the coming years.

Segmental Insights

Material Insights

Based

on the category of Material, the Plastics & polymers segment emerged as the

dominant in the India pharmaceutical packaging market in 2024. The Plastics

& Polymers segment dominates the Indian pharmaceutical packaging market due

to their versatility, cost-effectiveness, and ability to meet the unique

demands of the pharmaceutical industry. Plastics and polymers, including

materials such as polyethylene, polypropylene, polyethylene terephthalate

(PET), polyvinyl chloride (PVC), and others, are the most used materials for

packaging pharmaceutical products.

This dominance is driven by several key

factors that align with both the operational needs of pharmaceutical

manufacturers and consumer preferences. The major factors driving the dominance of plastics and

polymers in pharmaceutical packaging are their cost-effectiveness. Compared to

alternative materials such as glass or metal, plastics are generally less

expensive to produce, transport, and store. They are lightweight, reducing both

raw material costs and logistical expenses. In a price-sensitive market like

India, where affordability is a key concern, the cost advantages of plastic

packaging make it the material of choice for both local and international

pharmaceutical companies.

Plastics

and polymers are highly scalable in production, allowing packaging

manufacturers to meet the large and growing demand for pharmaceutical products.

With the rapid expansion of the pharmaceutical industry in India, the ability

to produce plastic packaging at scale is a significant advantage, enabling

manufacturers to meet increasing demand without compromising production efficiency. Plastics and polymers offer unmatched versatility when

it comes to customizing packaging solutions. These materials can be easily

molded into a variety of shapes and sizes, making them suitable for packaging a

wide range of pharmaceutical products, from tablets and capsules to liquids,

creams, and injectables. Plastics can be used to create bottles, blister packs,

jars, pouches, tubes, and ampoules, each with specific functions depending on the type of pharmaceutical product being packaged. These factors are

expected to drive the growth of this segment.

Download Free Sample Report

Regional Insights

West

India emerged as the dominant in the India pharmaceutical packaging market in

2024, holding the largest market share in terms of value. West India,

comprising key states such as Maharashtra, Gujarat, and Rajasthan, holds the

largest share of the Indian pharmaceutical packaging market. This region is

home to a robust pharmaceutical manufacturing infrastructure, which is a major

driver for the demand for packaging materials.

Maharashtra,

particularly Mumbai, is the center of the pharmaceutical industry in India,

housing numerous pharmaceutical companies and multinational corporations.

Gujarat, with its established industrial base and strategic location, is

another key pharmaceutical manufacturing hub. These states are not only major

producers of generic drugs but also serve international markets, driving demand for advanced packaging solutions. West India plays a crucial role in the

export of pharmaceutical products.

The region’s well-developed infrastructure,

including ports such as Jawaharlal Nehru Port (JNPT) and Mumbai Port,

facilitates the global export of pharmaceuticals, which requires compliance

with international packaging standards. This drives the demand for high-quality

packaging solutions like tamper-evident and child-resistant features, as well

as compliance with serialization requirements. West India is home to several

leading packaging companies that specialize in providing innovative packaging

solutions to the pharmaceutical industry. The region benefits from significant

investments in research and development (R&D), with companies focusing on

introducing new materials, smart packaging technologies, and sustainable

solutions. The concentration of these packaging manufacturers helps fuel the

growth of the pharmaceutical packaging market in West India.

Recent Developments

- In November 2025, Zydus Lifesciences partnered with SIG to launch Deriphyllin CoughGo in single-serve spouted pouches, introducing a new pharmaceutical packaging format in India for cough medication. Zydus said the pouch uses SIG’s advanced filling technology to make medicine intake more consumer-friendly while also helping reduce product waste and improve dosing convenience. The launch stood out because it moved beyond conventional bottle-based formats and showed how flexible packaging innovation is entering patient-facing pharmaceutical products in India.

- In October 2025, Siegwerk announced its entry into India’s pharmaceutical packaging segment with a dedicated range of mineral oil-free inks aimed at improving packaging safety and compliance. The company said the move responds to rising concerns over ink migration and is backed by an INR 350 crore investment to support next-generation safe and sustainable ink solutions for high-stakes applications such as pharma packaging. This development was significant because India still lacks specific guidelines for printing inks used in pharmaceutical packaging, so Siegwerk positioned the launch as both a product entry and a standards-upgrade play.

- In November 2025, Selig Group showcased its pharmaceutical liner solutions at PMEC 2025 and highlighted its partnership with Mumbai-based Altek for warehousing and product fulfilment across India. Selig said the local base helps Indian customers benefit from shorter lead times, local currency transactions, and avoidance of import taxes while supporting more secure, durable, and sustainable pharmaceutical packaging. The development is notable because it tied packaging-material specialization to a practical India-market collaboration model, improving access to liner technology for pharma packagers and manufacturers.

Key Market Players

- Amcor

Flexibles India Pvt. Ltd.

- Becton

Dickinson India Private Limited

- Aptar

Pharma India Pvt. Ltd

- Gerresheimer

AG

- SCHOTT

Poonawalla

- West

Pharmaceutical Services, Inc

- SGD

Pharma India Private Limited

|

By

Material

|

By

End User

|

By

Region

|

- Plastics

& Polymers

- Paper

& Paperboard

- Glass

- Aluminium

Foil

- Others

|

- Pharmaceutical

& Biotechnology companies

- Contract

Manufacturers

- Others

|

- North

India

- South

India

- East

India

- West

India

|

Report Scope:

In this report, the India Pharmaceutical Packaging

Market has been segmented into the following categories, in addition to the

industry trends which have also been detailed below:

- India Pharmaceutical Packaging Market, By Material:

o Plastics & Polymers

o Paper & Paperboard

o Glass

o Aluminium Foil

o Others

- India Pharmaceutical Packaging Market, By End User:

o Pharmaceutical & Biotechnology companies

o Contract Manufacturers

o Others

- India Pharmaceutical Packaging Market, By

Region:

o North India

o South India

o West India

o East India

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the India Pharmaceutical

Packaging Market.

Available Customizations:

India Pharmaceutical

Packaging market report with the given market data, Tech Sci Research

offers customizations according to a company's specific needs. The following

customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional

market players (up to five).

India Pharmaceutical Packaging Market is an

upcoming report to be released soon. If you wish an early delivery of this

report or want to confirm the date of release, please contact us at sales@techsciresearch.com