|

Forecast Period

|

2026-2030

|

|

Market Size (2024)

|

USD 240.03 Million

|

|

Market Size (2030)

|

USD 341.35 Million

|

|

CAGR (2025-2030)

|

6.16%

|

|

Fastest Growing Segment

|

Corrective

|

|

Largest Market

|

West India

|

Market Overview

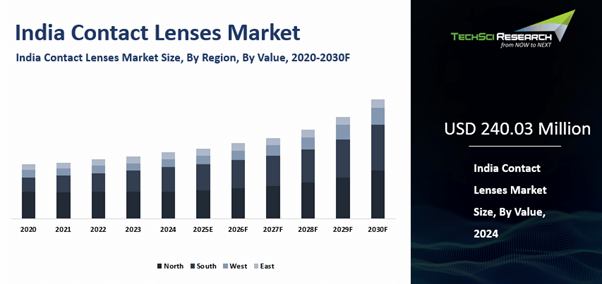

India Contact Lenses Market was valued at USD 240.03 Million in 2024 and is anticipated to reach USD 341.35 Million by 2030, with a CAGR of 6.16% during 2025-2030.

The India Contact Lenses

Market is being driven by several key factors. Increased awareness about eye

health and vision correction options among the population is fostering demand.

Advancements in technology have led to the development of more comfortable and

efficient contact lenses, appealing to a wider demographic. The rise in the

prevalence of visual impairments, coupled with lifestyle changes such as the

growing adoption of smartphones and computers, has fueled the need for

corrective eyewear like contact lenses.

A surge in disposable incomes and

changing fashion trends have also contributed to the market's growth as

individuals seek convenient and aesthetically pleasing vision correction

solutions. These factors converge to create a robust and expanding market for

contact lenses in India.

Download Free Sample Report

Key Market Drivers

Increasing Awareness And Education

- Awareness and education are becoming major demand drivers in the India contact lenses market as consumers gain better understanding of preventive eye care, safe contact lens usage, hygiene practices, replacement schedules, and the convenience of modern vision correction. This growing knowledge is helping reduce hesitation, especially among first-time users.

- Campaigns led by professional bodies and private brands are shifting contact lenses from a niche cosmetic product to a mainstream vision correction option supported by expert advice, product education, and clinical reassurance. This change is especially important in urban centers and emerging cities, where consumers often need confidence before adopting lenses regularly.

- Better education is also increasing trust in professional eye testing and lens fitting, encouraging users to move from occasional wear to more routine use. Stronger retail visibility, omni-channel consultations, and expanding organized optical chains are improving product discovery and access. For instance, the Optometry Council of India ran a nationwide eye health campaign across 2025 with five films in seven regional languages, while Lenskart expanded to 2,067 operational stores by March 2025.

Technological Advancements

- Technological advancements are strengthening the value proposition of contact lenses in India by making products more breathable, comfortable, and suitable for a broader consumer base. Innovations in material science, especially silicone hydrogel lenses, are helping reduce dryness and improve oxygen flow to the cornea, which directly addresses a major adoption barrier.

- Improved surface design, moisture retention technology, and specialized lens formats are allowing brands to better serve consumers with astigmatism, presbyopia, and intensive daily wear requirements. As a result, the India contact lenses market is moving beyond basic refractive correction toward high-performance solutions that support eye health, longer wear, and stronger user satisfaction.

- Premium innovation is also improving differentiation in the market and encouraging consumers to trade up from conventional lenses to advanced daily disposable and specialty lenses. For instance, in 2025, Alcon launched Precision1 lenses in India using Verofilcon A material designed to provide up to 16 hours of comfort, while CooperVision states that MyDay silicone hydrogel lenses offer nearly four times the oxygen transmissibility of comparable hydrogel lenses.

Prevalence Of Visual Impairments

- The growing prevalence of refractive errors remains one of the most fundamental growth drivers for the India contact lenses market, as more people across school-age, working-age, and older demographics require long-term vision correction. Rising incidence of myopia, hyperopia, astigmatism, and presbyopia is steadily expanding the addressable consumer base for corrective eye care products.

- Urban lifestyles, intensive near-work activity, lower outdoor exposure, and rising digital dependence are contributing to higher rates of visual impairment across India. Contact lenses are benefiting from this trend because they appeal not only to users seeking functional correction, but also to consumers who value aesthetics, freedom of movement, and a wider field of vision than spectacles typically provide.

- This demand trend is particularly strong among younger users and professionals who want less restrictive vision correction suited to active daily routines. Since refractive conditions often remain lifelong once diagnosed, the corrective user base continues to deepen over time, supporting recurring demand. For instance, a PRISMA-based review of eight Indian studies covering 28,600 participants found myopia among urban children aged 5 to 15 years increased from 4.44 percent in 1999 to 21.15 percent in 2019, with prevalence projected to reach 31.89 percent by 2030.

Lifestyle Changes and Digitalization

- Lifestyle changes linked to digitalization are creating a stronger use case for contact lenses in India as consumers spend more time on screens, follow busier routines, and prefer vision correction options that match mobile, appearance-conscious, and active lifestyles. These shifts are making contact lenses more relevant as both a functional and lifestyle-oriented product.

- Prolonged use of smartphones, laptops, and tablets is increasing visual fatigue, while hybrid work, online learning, gaming, and entertainment streaming are intensifying near-vision demands across age groups. In this setting, contact lenses are gaining traction because they offer unobstructed peripheral vision, convenience during movement, and better compatibility with sports, commuting, and social activities.

- Brand messaging is also evolving to address these modern lifestyle needs more directly, with stronger emphasis on moisture retention, stable all-day comfort, and reliable visual clarity under dynamic daily conditions. This is helping reposition contact lenses as a practical lifestyle solution rather than just a clinical correction tool. For instance, DataReportal reported that Indians spent an average of 6 hours and 49 minutes per day on the internet in 2025, while Bausch + Lomb says its Ultra One Day lenses are designed to maintain comfort for up to 16 hours.

Rising Disposable Incomes

- Rising disposable incomes are improving the affordability base for contact lenses in India as more consumers allocate spending toward healthcare, wellness, personal appearance, and convenience-driven products. This shift is expanding willingness to consider contact lenses not as an occasional discretionary purchase, but as a regular and aspirational eye care solution.

- As household purchasing power increases, consumers in urban middle-income groups and fast-developing tier II and tier III cities are showing greater readiness to experiment with premium eye care products. Contact lenses are benefiting because they are increasingly viewed as part of a broader lifestyle upgrade that combines visual correction, flexibility, comfort, and aesthetic appeal.

- Wider product availability across multiple price points is helping the category serve both entry-level and premium buyers, while organized retail chains and omnichannel optical platforms are making comparison, consultation, and repeat purchase easier. This is particularly important where first-time adoption depends on affordability, trust, and professional guidance. For instance, India’s per capita income rose to about INR 188,000 in fiscal year 2024 to 2025, while Lenskart expanded to 2,137 stores and Titan Eye+ to around 900 outlets, improving access across a broader set of income groups.

Key Market Challenges

Limited Awareness and Access to Eye Care Services

- Despite the growing prevalence of visual impairments in India, where nearly 55 million people live with significant vision impairment and 6.2 million are totally blind, there remains a considerable gap in awareness and access to eye care services. This is particularly true in rural communities where blindness is 1.37 times more common than in urban areas. Many individuals, especially in remote regions, lack knowledge about the importance of regular eye examinations, proper eye hygiene practices, and the availability of vision correction options like contact lenses.

- As a result, a large segment of the population remains underserved and undiagnosed, leading to delayed detection and management of vision problems, with uncorrected refractive errors being a primary cause of impairment. This gap contributes to situations where nearly 30,000 identified blind children in a single state like Odisha lack access to quality education. The shortage of qualified eye care professionals, optometrists, and ophthalmologists further exacerbates the issue, limiting the availability of specialized services such as contact lens fitting, prescription, and follow-up care, especially for conditions like cataracts which are a major cause of vision loss.

- Bridging this awareness and access

gap requires collaborative efforts from government agencies, non-profit

organizations, and private sector players to implement targeted outreach

programs, mobile eye clinics, telemedicine initiatives, and capacity-building

measures aimed at improving eye health literacy, promoting preventive care, and

expanding the reach of eye care services to remote and marginalized

populations.

Price Sensitivity and Affordability Concerns

- Price sensitivity and affordability concerns pose

significant challenges to the widespread adoption of contact lenses in India,

particularly among low and middle-income consumers. The cost of contact lenses,

including initial purchase, maintenance solutions, and periodic replacements,

can be prohibitive for many individuals, especially in a price-sensitive market

like India, where disposable incomes vary widely.

- The lack of insurance coverage

or reimbursement schemes for vision correction aids further limits

affordability and accessibility for marginalized populations. As a result, many

individuals resort to cheaper alternatives such as over-the-counter spectacles

or unregulated contact lenses, compromising visual acuity and eye health in the

long run. Addressing affordability concerns requires innovative pricing

strategies, product bundling options, and promotional schemes aimed at making

contact lenses more accessible and affordable to a wider demographic.

- Collaboration

with government agencies and healthcare payers to explore insurance coverage

and reimbursement options for vision correction aids can help alleviate

financial barriers and promote equitable access to eye care services.

Key Market Trends

Aging Population

India's demographic landscape is undergoing a significant transformation, characterized by an aging population with changing healthcare needs, with the number of individuals aged 60 and above projected to reach nearly 173 million by 2025. As individuals age, the prevalence of age-related eye conditions such as presbyopia increases, affecting an estimated 476 million people over age 40 by 2025, necessitating the use of vision correction aids like contact lenses. The desire to maintain an active and independent lifestyle among older adults has driven the demand for advanced solutions, such as Alcon's Precision1 lenses launched in April 2025 and the Dailies Total1 Multifocal, which offer clear vision and enhanced mobility without the hassle of traditional eyeglasses.

Expanding Distribution Channels

The proliferation of e-commerce platforms and online retail channels has significantly expanded the reach and accessibility of contact lenses across India, with major player Lenskart now serving over 27,500 pin codes as of March 2025. Consumers now have the convenience of browsing and purchasing contact lenses from the comfort of their homes, supported by services like Lenskart's "at-home" eye check-ups that bring certified optometrists to the doorstep. The presence of brick-and-mortar optical stores and eye care clinics in urban and semi-urban areas ensures that consumers have multiple touchpoints, with Lenskart operating 2,137 stores and Titan Eye+ managing 877 outlets by late 2025, to purchase contact lenses and seek professional guidance on fitting and usage, driving market penetration and growth.

Download Free Sample Report

Segmental Insights

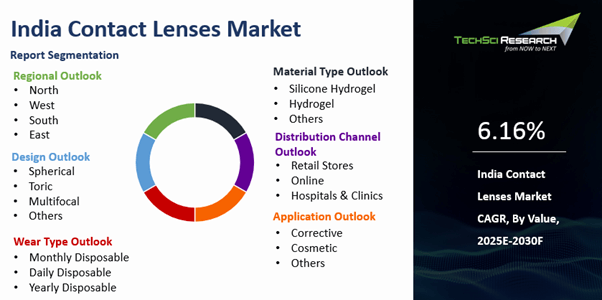

Material Type Insights

Based on the Material Type, in the dynamic landscape of the India Contact Lenses Market, Silicone Hydrogel lenses have been steadily gaining dominance over traditional Hydrogel lenses. As the largest revenue-generating material in the Indian market in 2024, Silicone Hydrogel lenses offer superior oxygen permeability, moisture retention, and comfort. These lenses allow up to six times more oxygen to pass through them than conventional soft lenses.

These lenses are made from a silicone-based material that allows more oxygen to pass through to the cornea, reducing the risk of hypoxia and enabling extended wear schedules. This advanced technology has resonated with consumers seeking enhanced comfort and convenience in their vision correction options. Silicone Hydrogel lenses are known for their resistance to protein deposits, making them easier to clean and maintain. As a result, they have become the preferred choice for individuals with active lifestyles or those who require long hours of wear, such as office professionals or students.

Silicone Hydrogel lenses have shown promising results in managing conditions like dry eye syndrome, further expanding their market appeal. While Hydrogel lenses still hold a significant share, the growing demand for Silicone Hydrogel lenses, the fastest-growing material segment, underscores a shift towards advanced materials and technologies in the India Contact Lenses Market. Manufacturers and providers continue to invest in research and development to improve further the performance, comfort, and safety of Silicone Hydrogel lenses, ensuring their continued dominance in the evolving landscape of vision correction solutions.

Application Insights

Based on Application, in the India Contact Lenses Market, corrective lenses, which represent the largest market segment, hold a dominant position compared to cosmetic lenses. Corrective contact lenses are primarily designed to address refractive errors such as myopia, hyperopia, astigmatism, and presbyopia, providing users with improved visual acuity and clarity. Given the significant prevalence of refractive errors in the Indian population a condition responsible for approximately 53% of the nation's visual impairment burden corrective contact lenses constitute the majority of sales in the market. These lenses are prescribed by optometrists or ophthalmologists based on individual eye examinations and specific vision correction needs, ensuring optimal visual outcomes and ocular health, with distribution regulated by the Central Drugs Standard Control Organization (CDSCO) through licensed professionals.

Advancements in corrective lens technologies, such as Silicone Hydrogel materials and multifocal designs, have further fuelled their popularity among consumers seeking comfortable and convenient vision correction solutions, with one survey showing that 65% of participants recognized lenses primarily for their vision correction capabilities. On the other hand, cosmetic contact lenses, which are designed to alter the appearance of the eye by changing its color or enhancing its natural features, represent a smaller segment of the market. While cosmetic lenses appeal to individuals interested in enhancing their aesthetic appeal or achieving a particular look for special occasions or performances, they are typically considered discretionary or novelty items rather than essential vision correction aids.

The use of cosmetic lenses, which are also under the purview of the CDSCO, requires careful consideration of safety and hygiene practices to avoid potential risks such as corneal abrasions or infections. While both corrective and cosmetic contact lenses cater to different consumer needs and preferences, the India Contact Lenses Market is primarily driven by the demand for corrective lenses due to the widespread prevalence of refractive errors like myopia and astigmatism and the emphasis on visual health and functionality.

Regional Insights

The Western region emerges as a dominant region,

spearheading market growth and innovation. Comprising states such as

Maharashtra, Gujarat, Rajasthan, and Goa, the Western region stands out for its

robust economic activity, urbanization, and access to healthcare

infrastructure. Major metropolitan cities like Mumbai, Pune, and Ahmedabad

serve as key hubs for eye care services, housing a dense network of eye

clinics, optometry practices, and retail outlets specializing in vision

correction solutions. The Western region boasts a diverse consumer base,

including young professionals, students, and fashion-conscious individuals, who

are increasingly embracing contact lenses as a preferred choice for vision

correction and style enhancement.

The Western region's cosmopolitan culture,

characterized by a blend of traditional values and modern trends, fosters a

receptive environment for innovative products like colored and specialty

contact lenses. This cultural dynamism, coupled with rising disposable incomes

and lifestyle aspirations, propels demand for contact lenses in the Western

region, driving market expansion and shaping industry trends.

The Western

region's strategic location and connectivity facilitate seamless distribution

and logistics, enabling contact lens manufacturers and suppliers to efficiently

reach consumers across urban and semi-urban areas. While other regions also

contribute significantly to the India Contact Lenses Market, the Western

region's combination of economic vibrancy, cultural diversity, and

infrastructural advantages position it as a dominant player driving the

market's evolution and growth trajectory.

Recent Developments

- In June 2025, Dr Agarwals Eye Hospital announced a collaboration with Menicon Co., Ltd. to advance myopia control in India through contact-lens-based treatment, especially orthokeratology. The announcement said the two organizations had signed an MoU to support joint R&D, clinical studies in Indian children using Menicon Bloom Night orthokeratology lenses, ophthalmologist and optometrist training, patient awareness efforts, and future expansion of the contact lens business in India and nearby markets. This stands out as one of the clearest India-specific contact-lens collaborations of 2025 because it links a major eye-care chain with a global lens innovator around a defined clinical need.

- In May 2025, Virohan partnered with Lenskart to launch the SureStart programme, a training and employment initiative for future optometrists in India. BioSpectrum India reported that the curriculum includes contact lenses, binocular vision, ocular pathology, and optometric procedures, while also giving students hands-on exposure, guest lectures, and paid internships at more than 2,000 Lenskart stores. Although this is not a product launch, it is directly relevant to the contact-lens market because it strengthens the professional talent pipeline that supports fitting, dispensing, and clinical adoption across India.

- In April 2025, Alcon launched PRECISION1 contact lenses in India, according to recent industry coverage summarizing 2025 market developments. The article said the product is India’s first contact lens with SMARTSURFACE technology and was designed to maintain more than 80 percent water content on the lens surface while delivering up to 16 hours of comfort, particularly for users with active and digitally intensive lifestyles. This qualifies as a meaningful product innovation because the launch brought a specific lens-material and surface-technology proposition into the Indian daily-disposable segment.

- In October 2025, Dr Agarwals Eye Hospital launched a specialised myopia clinic in Chandigarh that included soft contact lenses among its myopia-control options. BioSpectrum India reported that the clinic was designed to provide a structured set of interventions for myopia management, combining different modalities rather than relying only on glasses or routine refractive correction. This is relevant to India’s contact-lens landscape because it reflects the growing institutionalization of specialty lens use within organized eye-care delivery.

- In October 2025, Johnson & Johnson introduced ACUVUE OASYS MAX 1-Day MULTIFOCAL for ASTIGMATISM. This lens is the first daily disposable multifocal toric option for presbyopic users with astigmatism. It offers stable, clear vision across all distances and lighting conditions and is available in the U.S., Canada, and select EMEA and APAC regions with ongoing launches in India.

- In April 2025, Alcon launched PRECISION1™ contact lenses in India, supported by a strategic advertising campaign developed in collaboration with Scarecrow M&C Saatchi. The campaign addresses the common challenges faced by contact lens users in India, particularly those with digitally intensive and active lifestyles. PRECISION1™ is the first contact lens in India to feature SMARTSURFACE® technology, an innovation that maintains over 80% water content on the lens surface, delivering up to 16 hours of comfort. As a global leader in eye care, Alcon introduced the ‘Switch to PRECISION1’ campaign to promote its next-generation daily disposable lenses, offering a compelling solution for all-day wear.

- In January 2025, the global private equity firm CVC Capital Partners announced its intention to acquire OLENS, South Korea's largest contact lens brand. The deal is valued at approximately 500 billion won, which is equivalent to about $343 million. This acquisition is a major strategic step for both companies and signals a new phase of expansion for the popular Korean brand.

Key Market Players

- Bausch & Lomb India

Private Ltd.

- Alcon Laboratories (India)

Pvt. Ltd.

- Johnson & Johnson Private

Limited

- CooperVision India

- Carl Zeiss India

- Hoya Medical India Pvt. Ltd.

- GKB Ophthalmics Ltd.

- Contek Solutions India

- Excellent Hicare Pvt Ltd.

- Omni Lens Pvt Ltd.

|

By Material Type

|

By Design

|

By Application

|

By Wear Type

|

By Distribution Channel

|

By Region

|

- Silicone Hydrogel

- Hydrogel

- Others

|

- Spherical

- Toric

- Multifocal

- Others

|

|

- Monthly Disposable

- Daily Disposable

- Yearly Disposable

|

- Retail Stores

- Online

- Hospitals & Clinics

|

|

Report Scope:

In this report, the India Contact Lenses Market has

been segmented into the following categories, in addition to the industry

trends which have also been detailed below:

- India Contact Lenses Market, By Material Type:

o Silicone Hydrogel

o Hydrogel

o Others

- India Contact Lenses Market, By Design:

o Spherical

o Toric

o Multifocal

o Others

- India Contact Lenses Market, By Application:

o Corrective

o Cosmetic

o Others

- India Contact Lenses Market, By Wear Type:

o Monthly Disposable

o Daily Disposable

o Yearly Disposable

- India Contact Lenses Market, By Distribution Channel:

o Retail Stores

o Online

o Hospitals & Clinics

- India Contact Lenses Market, By Region:

o North

o South

o West

o East

Competitive Landscape

Company Profiles: Detailed analysis of the major companies

present in the India Contact Lenses Market.

Available Customizations:

India Contact Lenses Market report with the

given market data, TechSci Research offers customizations according to a

company's specific needs. The following customization options are available for

the report:

Company Information

- Detailed analysis and

profiling of additional market players (up to five).

India Contact Lenses Market is an upcoming

report to be released soon. If you wish an early delivery of this report or

want to confirm the date of release, please contact us at sales@techsciresearch.com