Market Overview

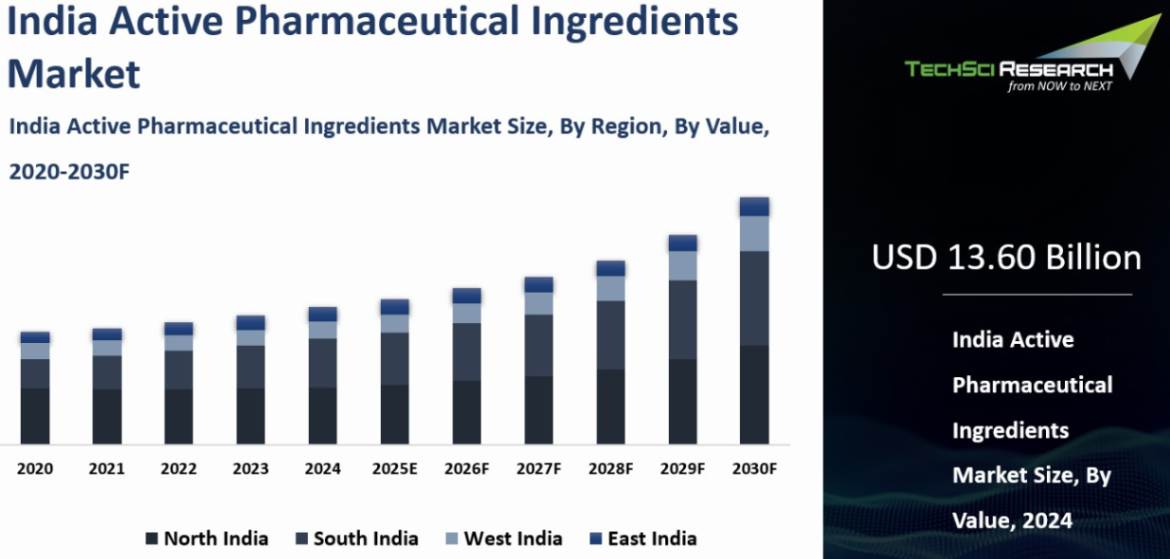

India Active Pharmaceutical Ingredients Market was valued at USD 13.60 Billion in 2024 and is anticipated to reach USD 21.99 Billion by 2030, with a CAGR of 8.30% through 2030.

|

Forecast

Period

|

2026-2030

|

|

Market

Size (2024)

|

USD

13.60 Billion

|

|

Market

Size (2030)

|

USD

21.99 Billion

|

|

CAGR

(2025-2030)

|

8.30%

|

|

Fastest

Growing Segment

|

In-house

Manufacturing

|

|

Largest

Market

|

North

India

|

Active Pharmaceutical Ingredients (APIs) are the biologically active components in medicines responsible for producing therapeutic effects. These include small molecules, peptides, proteins, and nucleic acids, which are formulated into dosage forms such as tablets, capsules, and injections. India is the world’s third-largest API producer by volume and holds around 8% of the global market share, manufacturing more than 500 APIs.

Strong investments in research and development, rising demand for generic and specialty drugs, and government initiatives such as the Production-Linked Incentive (PLI) scheme are driving market growth. Additionally, expanding custom synthesis, contract manufacturing services, and integration into global pharmaceutical supply chains are strengthening India’s position in the global API market.

Download Free Sample Report

Key Market Drivers

Rise in the Domestic Pharmaceutical Market

- India’s expanding domestic pharmaceutical market is a major demand engine for active pharmaceutical ingredients, as rising chronic disease, broader treatment access, and continued dependence on affordable generics keep medicine volumes high across therapy areas. Every increase in prescriptions for diabetes, cardiovascular disease, respiratory illness, and age-related conditions directly raises demand for APIs, drug substances, and intermediates.

- Demand is further supported by policy backing, stronger distribution networks, and a healthcare environment where patients increasingly expect low-cost therapies rather than episodic treatment. As the population ages and non-communicable diseases become more persistent, formulators are likely to strengthen sourcing ties with API suppliers offering scale, quality, and cost efficiency. For instance, Invest India states that India is the world’s third-largest pharmaceutical producer by volume, supplies about 20% of global generic drug exports, and manufactures more than 500 different APIs.

Increasing Demand of Custom Synthesis and Contract Manufacturing

- Custom synthesis and contract manufacturing are gaining importance in India’s API industry because drug developers want faster scale-up, lower manufacturing risk, and specialized partners that can take molecules from lab development to commercial supply without requiring major internal capacity expansion. This model is especially attractive for global innovators and formulators seeking flexible production for new chemical entities, high-potency compounds, intermediates, and clinical-phase materials.

- Indian providers are strengthening their value proposition through process development, analytical validation, impurity profiling, stability support, and regulatory documentation, making them more than simple capacity vendors. As customers diversify supply chains, India is becoming more relevant for demanding programs requiring speed, confidentiality, and scalable execution. For instance, Aarti Pharmalabs says it has developed processes for more than 200 products at kilo scale, commercialized more than 100, and offers capacity from 1 kilogram to 500 metric tonnes per year with over 800 kilolitres of plant volume.

Key Market Challenges

Quality Control and Assurance

- Quality control and assurance remain central challenges for India’s active pharmaceutical ingredients industry because export credibility depends on consistently meeting strict standards for purity, traceability, documentation, validation, and data integrity. Producers must control raw material qualification, process chemistry, analytical testing, deviation management, and batch release, since even minor inconsistency can disrupt downstream drug manufacturing and invite regulatory scrutiny.

- Pressure is especially high for API companies serving the United States and Europe, where approvals depend not only on product quality but also on inspection readiness, trained technical teams, and well-maintained GMP systems. This forces continued investment in laboratories, automation, audit preparedness, and skilled personnel. For instance, Aurobindo Pharma reported 13 API and intermediates facilities, 291 US DMFs, and zero observations with No Action Indicated status for its peptide API facility in FY24.

Market Access Barriers

- Market access barriers remain a persistent issue for India’s API manufacturers because entry into regulated markets depends on more than cost competitiveness and production scale. Suppliers must comply with market-specific requirements such as US DMF filings, European CEP certification, customs documentation, impurity controls, and detailed chemistry, manufacturing, and control records before commercial supply can begin.

- These barriers become harder when customers expect uninterrupted quality, patent awareness, and audit-ready manufacturing while still negotiating aggressively on price and delivery. Indian suppliers therefore need regulatory depth, documentation discipline, and multi-market credibility rather than low-cost positioning alone. For instance, Pharmexcil reported that by 11 June 2010, India had filed 2,234 type II active DMFs with the US FDA through 340 companies, representing 31.37% of the global total.

Key Market Trends

Environmental Sustainability

- Environmental sustainability is becoming a sharper strategic priority in India’s active pharmaceutical ingredients industry as manufacturers face stronger expectations on emissions, water management, waste handling, and cleaner production systems across global supply chains. For API producers, this now affects not only compliance, but also customer confidence, regulatory readiness, and the long-term economics of operating energy-intensive chemical manufacturing sites.

- Companies are therefore paying closer attention to renewable power adoption, solvent recovery, resource efficiency, and lower-impact process design that can reduce environmental burden without weakening output reliability. This also supports the broader goal of making Indian API manufacturing more resilient and globally competitive as overseas buyers increasingly seek suppliers combining cost advantages with measurable ESG progress. For instance, Dr. Reddy’s 2025 sustainability report states that the company sourced 57% of its total energy from renewable sources and achieved a 22% absolute reduction in Scope 1 and 2 emissions.

Growing Research and Development

- Growing research and development is strengthening India’s active pharmaceutical ingredients industry because innovation now extends beyond volume manufacturing into process improvement, complex chemistry, import substitution, and the development of APIs for newer therapeutic needs. R&D is especially important as manufacturers work to improve yields, reduce impurities, support regulatory filings, and commercialize more technically demanding molecules for domestic formulations and export markets.

- It also plays a critical role in building self-reliance, as India’s policy direction increasingly favors local development of critical bulk drugs, intermediates, and key starting materials that were once heavily import dependent. This makes research capability a competitive differentiator for firms moving toward higher-value custom synthesis, specialty APIs, and faster commercialization. For instance, the Department of Pharmaceuticals reported that under the bulk drugs PLI scheme, 48 projects were approved, 34 commissioned for 25 bulk drugs, and realized investment reached Rs. 4,155.77 crores by late 2024.

Segmental Insights

Method of Synthesis

Insights

In 2024, the Synthetic segment held the largest share of the India Active Pharmaceutical Ingredients Market and is expected to continue expanding over the coming years. Synthetic APIs are highly

versatile and can be used in a wide range of pharmaceutical products, including

both generic and innovative drugs. Their broad applicability makes them a

popular choice for pharmaceutical manufacturers.

Synthetic APIs are often more

cost-effective to produce compared to their natural or biologically derived

counterparts. This cost advantage is particularly appealing to pharmaceutical

companies, as it helps reduce overall production expenses. Synthetic APIs can

be manufactured with a high degree of consistency and quality control, ensuring

that each batch meets strict regulatory and quality standards.

This is crucial

for drug safety and efficacy. Many Indian pharmaceutical companies specializing

in synthetic APIs have invested in maintaining rigorous quality standards and

obtaining approvals from stringent regulatory authorities, such as the US Food and

Drug Administration (FDA) and the European Medicines Agency (EMA). Synthetic

APIs can be tailored to meet specific requirements, allowing pharmaceutical

manufacturers to create proprietary formulations and optimize drug performance.

Synthetic APIs are often associated with a reliable and consistent supply,

reducing the risk of shortages or disruptions in the pharmaceutical supply

chain.

Source Insights

In 2024, the largest share of the India Active Pharmaceutical Ingredients Market was held by the Contract Manufacturing Organizations (CMO) segment and is predicted to continue expanding over the coming years. The global pharmaceutical industry has

witnessed a growing trend of outsourcing various aspects of drug development

and manufacturing to CMOs.

This trend extends to the production of APIs, with

many pharmaceutical companies preferring to focus on research, marketing, and

sales, while outsourcing API manufacturing. CMOs often offer cost-effective

solutions for API manufacturing. They have specialized facilities, expertise,

and efficient processes that can lead to cost savings for pharmaceutical

companies. India is known for its cost-effective pharmaceutical manufacturing.

Reputed Indian CMOs have invested in meeting stringent regulatory standards,

such as those set by the US Food and Drug Administration (FDA) and the European

Medicines Agency (EMA). This compliance is critical for API manufacturing,

especially for companies seeking to export to global markets. CMOs in India

often have significant production capacities and can efficiently scale up or

down based on the needs of their clients.

This flexibility is appealing to

pharmaceutical companies looking for reliable API suppliers. Many Indian CMOs

have a skilled and experienced workforce with expertise in various chemical and

pharmaceutical processes. This expertise is crucial for the development and

production of APIs. CMOs offer customized solutions that allow pharmaceutical

companies to tailor their API production to specific requirements. This

flexibility can be especially important for companies developing novel drugs or

unique formulations.

Download Free Sample Report

Regional Insights

The North India region dominated the India Active

Pharmaceutical Ingredients Market in 2024. North India, particularly the states of Himachal Pradesh and Punjab,

has a long history of pharmaceutical manufacturing. Many well-established

pharmaceutical companies, including some of the country's largest, are based in

this region. North India offers a conducive business environment with access to

skilled labor, infrastructure, and connectivity. It has well-developed

industrial clusters that support pharmaceutical manufacturing.

The proximity of

North India to the national capital, New Delhi, is advantageous for regulatory

and administrative purposes. It facilitates interactions with government bodies

and regulatory agencies. North India is home to several prominent educational

and research institutions specializing in pharmaceutical sciences. These institutions

provide a pool of trained talent and contribute to research and development in

the pharmaceutical sector. The state governments in North India have often been

proactive in promoting pharmaceutical manufacturing through incentives,

subsidies, and the establishment of pharmaceutical parks and special economic

zones.

Recent Developments

- In November 2025, HRV Global Life Sciences and MetroChem API announced a multi-year CDMO partnership focused on the exclusive and semi-exclusive development, scale-up, and GMP manufacturing of multiple high-value NCE-1 and late-stage complex APIs for regulated and semi-regulated markets. The alliance combines HRV Pharma’s global market access across more than 50 countries and its virtual API platform with MetroChem’s process chemistry, scale-up expertise, and GMP manufacturing base, and the initial pipeline was disclosed as five programs with more molecules planned later. This was a significant API collaboration because the two companies said they would jointly handle development, validation, stability work, CMC documentation, DMF filings across major markets, and long-term supply under a unified commercialization framework.

- In April 2025, French company INTEROR said it was strengthening partnerships within India’s pharmaceutical supply chain by setting up a representative office in Mumbai to identify and structure relationships with Indian active chemical companies. The company also said it was discussing potential co-development of complex intermediates and long-term sourcing partnerships with several Indian firms, while backing the India push with a €22 million manufacturing-capacity expansion in Calais to serve regulated markets. Although no formal joint venture was announced at that stage, the development still qualified as a collaboration-driven API story because INTEROR positioned India as a strategic partner base for custom synthesis, technology transfer, and supply-chain integration.

- In November 2025, the government reported a major manufacturing breakthrough under its PLI-linked API ecosystem, stating that by September 2025 domestic capacity had been created for 26 critical KSMs, drug intermediates, and APIs that were previously largely imported. The same official update said that under the broader pharmaceuticals PLI framework, 726 APIs, KSMs, and intermediates were being manufactured in India, including 191 that were being made domestically for the first time, while cumulative domestic sales from these products had reached ₹26,123 crore. This counted as a breakthrough innovation and self-reliance milestone for the API sector because it showed India moving from policy intent to first-time domestic production of a large set of higher-value pharma inputs.

- In March 2026, India reported a notable API-sector milestone when Chemicals and Fertilizers Minister J. P. Nadda said FY25 exports of active pharmaceutical ingredients had reached about ₹41,500 crore, exceeding imports of ₹39,215 crore. The same report said the bulk-drug PLI program had already established domestic manufacturing capacity for 28 of the 41 identified critical products and generated cumulative sales of ₹2,720 crore by December 2025, including exports worth ₹527.96 crore and avoided imports worth ₹2,192.04 crore. This was one of the clearest recent breakthrough developments in India’s API space because it signaled that local capability-building was beginning to translate into measurable trade-strength and import-substitution outcomes.

Key

Market Players

- Teva Pharmaceutical Industries Ltd.

- Pfizer Inc.

- Dr. Reddy's Laboratories

Ltd.

- Sun Pharmaceutical

Industries Limited

- Cipla Limited

- Lupin Limited

- Aurobindo Pharma Limited

- Aarti Drugs Ltd.

- IOL Chemicals and

Pharmaceuticals Limited

- GSK plc

|

By

Method of Synthesis

|

By

Source

|

By

Therapeutics Application

|

By

Drug Type

|

By

Region

|

|

|

- Contact

Manufacturing Organizations

- In-house

Manufacturing

|

- Cardiovascular

Diseases

- Anti-diabetic

Drugs

- Oncology

Drugs

- Neurological

Disorders

- Musculoskeletal

Disorders

- Others

|

|

- North

India

- South

India

- West

India

- East

India

|

Report Scope:

In this report, the India Active Pharmaceutical

Ingredients Market has been segmented into the following categories, in

addition to the industry trends which have also been detailed below:

- India Active Pharmaceutical Ingredients

Market, By

Method of Synthesis:

o Synthetic

o Biological

- India Active Pharmaceutical Ingredients

Market, By

Source:

o Contact Manufacturing Organizations

o In-house Manufacturing

- India Active Pharmaceutical Ingredients

Market, By

Therapeutic Application:

o Cardiovascular Diseases

o Anti-diabetic Drugs

o Oncology Drugs

o Neurological Disorders

o Musculoskeletal Disorders

o Others

- India Active Pharmaceutical Ingredients

Market, By Drug Type:

o Generics

o Innovator

- India Active Pharmaceutical Ingredients Market, By

region:

o North India

o

South

India

o

East

India

o

West

India

Competitive Landscape

Company Profiles: Detailed analysis of the major companies presents in the India Active Pharmaceutical Ingredients Market.

Available Customizations:

India Active Pharmaceutical Ingredients

Market report with the given market data, TechSci Research offers

customizations according to a company's specific needs. The following

customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional

market players (up to five).

India Active Pharmaceutical Ingredients Market is

an upcoming report to be released soon. If you wish an early delivery of this

report or want to confirm the date of release, please contact us at sales@techsciresearch.com