|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 42.11 Billion

|

|

CAGR (2026-2031)

|

4.46%

|

|

Fastest Growing Segment

|

OTC

|

|

Largest Market

|

Northern France

|

|

Market Size (2031)

|

USD 54.71 Billion

|

Market Overview

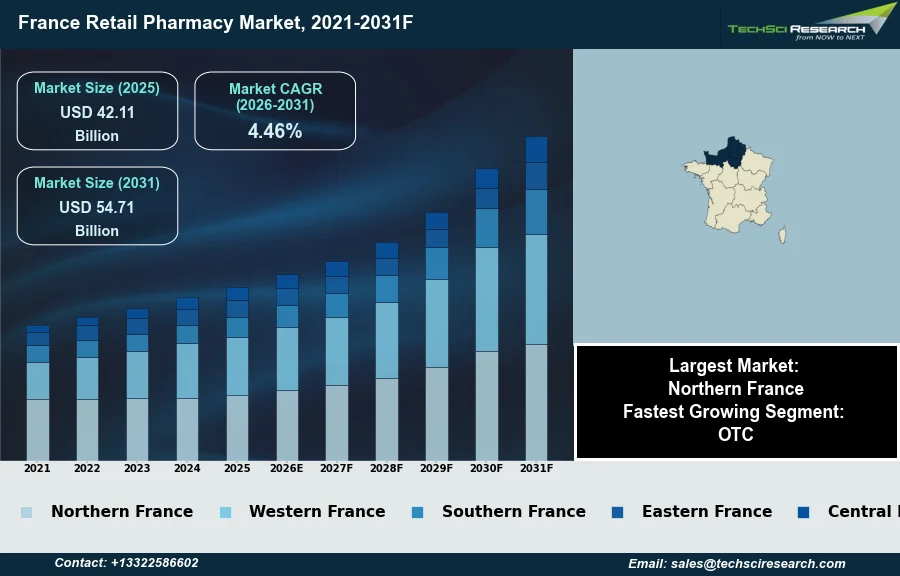

The France Retail Pharmacy Market will grow from USD 42.11 Billion in 2025 to USD 54.71 Billion by 2031 at a 4.46% CAGR. The France Retail Pharmacy Market encompasses healthcare establishments authorized to dispense prescription and over-the-counter medications, medical devices, and natural health products, forming an extensive and regulated distribution network crucial for national healthcare provision. Key growth drivers include France's aging population and the increasing burden of chronic diseases, which generate sustained demand for pharmaceutical products. Additionally, the expanding clinical responsibilities delegated to pharmacists, such as vaccination and health screenings, enhance their role as primary healthcare providers. According to the Fédération des Syndicats Pharmaceutiques de France (FSPF), in 2025, the pharmacy network recorded 135 million euros in additional remuneration, primarily due to the structural effect of the pharmaceutical market.

However, a significant challenge impeding market expansion is the ongoing decline in the number of physical pharmacies. According to the Ordre National des Pharmaciens, in 2024, France counted 19,627 pharmacies in metropolitan France, representing a decrease of 1.3% compared to 2023. This reduction, often characterized by unreplaced closures, can lead to reduced territorial coverage, particularly impacting rural and underserved areas, thereby constraining accessibility and potential for service growth.

Key Market Drivers

Aging population sustains demand for medicines and health products.

France's aging population and the increasing prevalence of chronic diseases continue to be fundamental drivers for the retail pharmacy market. As the demographic landscape shifts, a larger segment of the population requires sustained pharmaceutical care and ongoing health management. The consistent rise in the elderly demographic directly fuels demand for both prescription medications and a broader range of over-the-counter health products. According to INSEE, in January 2026, 22% of France's population was aged 65 or over, indicating a substantial cohort with heightened healthcare needs for chronic conditions and preventive care. This demographic trend ensures a steady and growing consumption of medicines and ancillary health services provided by retail pharmacies.

Expansion of advanced clinical services and policy support strengthens pharmacy viability.

Further bolstering the market is the ongoing expansion of advanced clinical and preventive pharmacy services, which critically enhances the role of pharmacists as accessible healthcare providers. These expanded services, such as vaccinations and health screenings, not only diversify revenue streams for pharmacies but also improve public health outcomes by increasing accessibility to primary care. According to Charles River Associates, in April 2026, analysis of the Social Security Financing Act 2026 indicated that conventional aid for pharmacies in difficulty was extended, a change expected to benefit around 800 additional pharmacies. This evolution supports the financial viability of pharmacies and positions them as integral hubs for community health. Moreover, according to the Ordre National des Pharmaciens, in January 2026, 75,731 pharmacists were registered in France, indicating a robust professional workforce supporting this expanding service provision.

Download Free Sample Report

Key Market Challenges

Decline in Physical Pharmacies Hinders Market Growth and Access

A significant challenge impeding the growth of the France Retail Pharmacy Market is the ongoing decline in the number of physical pharmacies. This reduction in the pharmacy network directly hampers market expansion by diminishing territorial coverage, particularly impacting rural and underserved populations. Consequently, patient access to essential medications and pharmaceutical services is constrained.

Network Contraction Limits Service Capacity and Reach

This trend directly limits the potential for service growth, despite the expanding clinical responsibilities delegated to pharmacists. Fewer physical locations mean a reduced capacity to implement and scale new healthcare services, such as vaccinations and health screenings, across the nation. According to the Ordre National des Pharmaciens, in 2026, France counted 19,990 pharmacies across its national territory, a decrease from 20,242 in 2025. This continuous contraction of the pharmacy network restricts the overall reach and efficacy of the national healthcare provision, thereby impeding the market's ability to capitalize on underlying demand drivers.

Key Market Trends

Digitalization of pharmacy services in France

Digitalization of pharmacy services represents a transformative trend within the France Retail Pharmacy Market, shifting how patients access care and manage their health. This trend encompasses the increasing adoption of online prescription refills, digital health records, and the growing availability of teleconsultation services. These digital advancements enhance convenience and accessibility for consumers, particularly in areas facing reduced physical pharmacy coverage. The market for remote healthcare in France, a key aspect of this digitalization, is projected to reach $7.5 billion by 2025, reflecting a significant expansion of virtual health platforms and digital interactions between pharmacists and patients. This evolution positions pharmacies as integral digital health hubs, enabling more seamless and efficient engagement with the healthcare system.

Omnichannel growth and online sales in French pharmacies

Concurrently, the evolution towards omnichannel retail experiences is significantly influencing the market by integrating online and physical sales channels for a comprehensive consumer journey. This trend extends beyond traditional pharmaceutical dispensing to include the sale of parapharmacy and non-prescription health products through diverse digital platforms. While pharmacies maintain their physical presence, the growing consumer preference for online purchasing compels them to develop robust e-commerce capabilities, often complementing in-store offerings with digital services. In the broader French retail landscape, e-commerce accounted for an estimated 12% of overall retail product sales in 2025, underscoring the necessity for retail pharmacies to adapt to these shifting consumer behaviors to remain competitive and relevant. This integration allows for a unified brand experience, accommodating varied customer preferences for purchasing and service access.

Segmental Insights

OTC Growth Driven by Self-Medication, Wellness Trends, and ANSM-Enabled Access

The Over-The-Counter (OTC) segment is the fastest-growing within the France Retail Pharmacy Market, driven by several interconnected factors. This robust expansion is primarily attributed to a notable rise in consumer self-medication practices and an increasing focus on personal well-being among the French population. The government actively encourages the use of non-prescriptive drugs, which helps alleviate demand on the healthcare service. Furthermore, regulatory adjustments facilitated by the National Agency for the Safety of Medicines and Health Products (ANSM) have allowed for greater direct access to eligible medicines within pharmacies, while pharmacists continue to play a crucial role in providing essential guidance to consumers.

Regional Insights

Northern France: Demographics, Infrastructure, and Regulation Driving Retail Pharmacy Demand

Northern France leads the France Retail Pharmacy Market, primarily driven by its dense and diverse population, especially within urban centers like Île-de-France. This high concentration of residents, including a substantial aging demographic, generates consistent demand for both prescription and over-the-counter medications. The region also benefits from a robust healthcare infrastructure, encompassing numerous hospitals, clinics, and diagnostic centers, which ensures a steady flow of prescriptions to retail pharmacies. Furthermore, comparatively higher income levels and consumer spending capacity in Northern France contribute to increased purchases of premium health products. The market operates under the stringent oversight of bodies like the Ordre National des Pharmaciens, ensuring regulatory compliance and quality of service.

Recent Developments

-

In February 2025, Datapharm, a UK-based provider of medicines information, established a strategic partnership with VIDAL, a prominent French platform for medical and drug information. This collaboration aimed to enhance access to essential medicines information for healthcare professionals in France. Through this alliance, Datapharm's Scientific Response Document (SRD) Search technology was integrated into VIDAL's platform, providing French healthcare professionals with comprehensive and up-to-date data on medical therapies. This initiative directly supported the France Retail Pharmacy Market by improving the resources available to pharmacists for informed decision-making and patient care.

-

In August 2024, Delpech Pharmacy in France achieved a significant milestone by becoming the first to legally introduce a new GS-441524-based treatment for Feline Infectious Peritonitis (FIP). This breakthrough offered new hope for treating a disease previously considered fatal for cats. Subsequently, in January 2025, Delpech Pharmacy hosted an event where CurifyLabs presented pioneering research on the potential of 3D-printed pharmaceuticals for personalized veterinary medicine. This development underscores the role of French retail pharmacies in adopting and advancing innovative treatments and research within the market.

-

In January 2024, the French health service initiated a program offering free medical check-ups, known as "mon bilan prévention," which became available through various healthcare providers, including pharmacies. Further expanding their roles, qualified pharmacists in France were authorized in June 2024 to conduct rapid diagnostic tests for throat infections and cystitis. If a test yielded a positive result, pharmacists could then dispense the appropriate antibiotic. These new services enhanced the scope of practice for retail pharmacists, making essential health checks and immediate treatment more accessible to the public.

-

In 2025, Valbiotis, a French laboratory specializing in dietary supplements, significantly expanded its product portfolio and distribution network within the France Retail Pharmacy Market. The company launched two new products in its ValbiotisPRO® range: ValbiotisPRO® Metabolic Health in February and ValbiotisPRO® Cardio-circulation in June. Additionally, five new ValbiotisPLUS® dietary supplements became available in pharmacies by October 2025. Valbiotis also strengthened its presence through agreements with three new pharmacy groups, including Leadersanté, CPC/Kare Santé, and the Evecial Group alliance, collectively covering over 1,500 pharmacies.

Key Market Players

- CVS Health Corporation

- Walgreens Boots Alliance, Inc.

- McKesson Corporation

- Phoenix Pharmahandel GmbH & Co KG

- Alliance Healthcare Group

- Celesio AG

- Galenica AG

- Sanofi S.A.

- Bayer AG

- Pfizer Inc.

|

By Product

|

By Type

|

By Region

|

|

|

|

- Northern France

- Western France

- Southern France

- Eastern France

- Central France

|

Report Scope:

In this report, the France Retail Pharmacy Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

France Retail Pharmacy Market, By Product:

-

France Retail Pharmacy Market, By Type:

-

France Retail Pharmacy Market, By Region:

-

Northern France

-

Western France

-

Southern France

-

Eastern France

-

Central France

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the France Retail Pharmacy Market.

Available Customizations:

France Retail Pharmacy Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

France Retail Pharmacy Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com