|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 9.45 Billion

|

|

CAGR (2026-2031)

|

7.21%

|

|

Fastest Growing Segment

|

Private

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 14.35 Billion

|

Market Overview

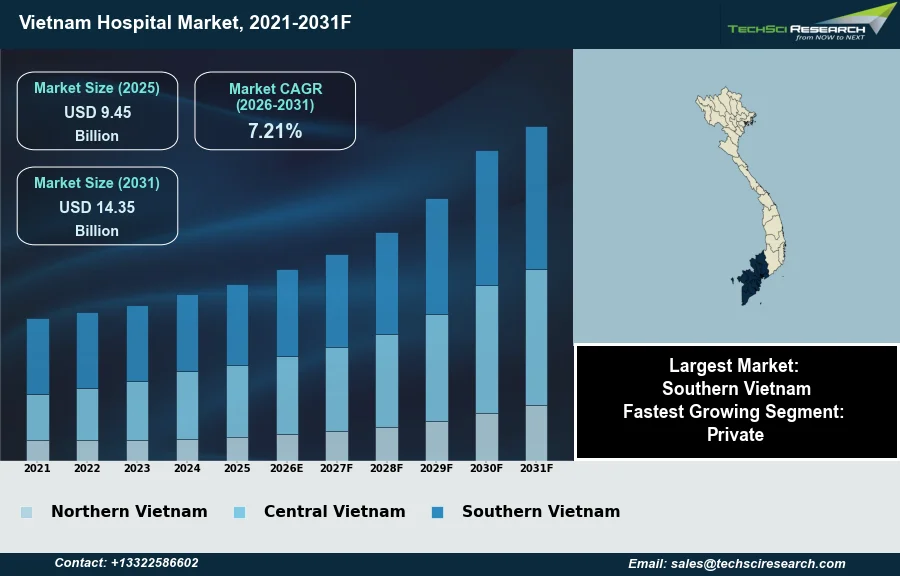

The Vietnam Hospital Market will grow from USD 9.45 Billion in 2025 to USD 14.35 Billion by 2031 at a 7.21% CAGR. The Vietnam Hospital Market encompasses the comprehensive provision of medical services, including diagnostic, therapeutic, and rehabilitative care, offered through both public and private healthcare institutions. Key drivers sustaining market growth include Vietnam’s consistent population expansion, rising disposable incomes leading to increased healthcare expenditure, and evolving disease patterns necessitating more specialized care. According to the General Statistics Office of Vietnam, in 2024, there were 1,531 hospitals operating nationwide.

A significant challenge impeding market expansion is the persistent shortage of adequately trained healthcare professionals, particularly in advanced specialties, which can limit the capacity for high-quality service delivery and hinder technological adoption across the hospital network.

Key Market Drivers

Rising Middle-Class Income Drives Private Healthcare Demand

Rising Middle-Class Income and Spending Power significantly drives the Vietnam Hospital Market, directly increasing demand for diverse and higher-quality medical services. As disposable incomes improve, a larger segment of the population can afford private healthcare options, including specialized treatments and advanced diagnostics, reducing reliance on public facilities. This demographic shift stimulates private sector investment to meet evolving patient expectations for enhanced comfort, shorter waiting times, and access to modern medical technologies. For instance, according to Hospital Management Asia, in May 2025, Vietnam's middle class was expected to grow from 13% of the population in 2023 to 26% by 2026. This expansion indicates a substantial increase in individuals accessing premium healthcare services.

Government Policy Support and Insurance Expansion

Supportive government policies for private healthcare investment further bolster market development by creating a favorable environment for infrastructure expansion and service innovation. The government promotes private sector participation through incentives and regulatory frameworks, aiming to alleviate pressure on public hospitals and enhance overall healthcare capacity. This direction encourages investment in new private hospitals, modernization of facilities, and adoption of advanced medical equipment. A notable policy, according to Insurance Asia, in September 2025, confirmed Vietnam's aim to achieve over 95% health insurance coverage by 2026, broadening access and financial feasibility for healthcare services. This supportive environment contributes to the broader market, with Vietnam's healthcare expenditure projected to rise to US$33.8 billion by 2030, according to Hospital Management Asia, in May 2025.

Download Free Sample Report

Key Market Challenges

Workforce shortage constrains expansion and technology adoption.

A significant challenge impeding the Vietnam Hospital Market's expansion is the persistent shortage of adequately trained healthcare professionals, particularly in advanced specialties. This deficit directly limits the capacity for high-quality service delivery across both public and private institutions. Furthermore, the lack of specialized personnel hinders the effective adoption and integration of new medical technologies throughout the hospital network, preventing facilities from offering state-of-the-art treatments and improving patient outcomes.

Projected Nursing and Resident Doctor Shortages.

This human resource constraint directly hampers the overall growth of the market by restricting the ability of hospitals to expand their services, meet the increasing demand for complex care, and compete regionally. According to the Department of Medical Services Administration under the Ministry of Health, in November 2025, Vietnam had approximately 14-15 nurses per 10,000 people, falling significantly short of the target of 25 nurses per 10,000 people set for the same year. Additionally, a survey conducted by the University of Medicine and Pharmacy under the Vietnam National University, Hanoi, found that the demand for resident doctors in 2026 and 2027 could reach approximately 7,500 positions across central and provincial hospitals, indicating a substantial need for specialist medical staff.

Key Market Trends

Digital Transformation and AI Adoption in Vietnamese Hospitals

Digital transformation and telemedicine expansion are profoundly reshaping the operational landscape and service delivery models within the Vietnam Hospital Market. Hospitals are increasingly integrating advanced digital solutions to enhance efficiency, improve patient outcomes, and broaden access to care, particularly in remote areas. This shift involves implementing electronic health records, artificial intelligence powered diagnostics, and virtual consultation platforms. The accelerated adoption of these technologies indicates a strategic move towards building a more interconnected and responsive healthcare ecosystem. According to the Vietnam Medical Informatics Association, in June 2026, a total of 1,238 hospitals across Vietnam had commenced applying artificial intelligence and digital technologies in their healthcare services, establishing a foundation for future smart hospital development.

Vietnam as a Medical Tourism Destination

The emergence of Vietnam as a significant medical tourism destination is another pivotal trend influencing the hospital market. The country is leveraging its competitive advantage in cost-effective yet high-quality medical services, attracting a growing number of international patients for various treatments including dental care, cosmetic surgery, and fertility treatments. This influx stimulates investment in specialized facilities and services tailored for foreign visitors, elevating international standards of care within the domestic market. According to the health sector, as reported by Vietnam News in April 2026, the turnover from medical tourism in 2025 reached US$850 million, demonstrating the market's increasing appeal and economic contribution.

Segmental Insights

Private Segment Growth Fueled by Demand, Affluence, and Policy Support

The private segment is currently the fastest-growing within the Vietnam Hospital Market, driven by a confluence of significant socioeconomic and governmental factors. Rapid expansion is primarily fueled by the increasing strain and overcrowding in public hospitals, particularly in major urban areas, which creates a demand for alternative, higher-quality services. Concurrently, the rise of Vietnam's middle class and increasing disposable incomes enable a greater willingness to pay for improved healthcare experiences. Furthermore, the nation's rapidly aging population contributes to a heightened need for specialized and long-term care. Supportive government policies, championed by the Ministry of Health, actively encourage private sector investment and public-private partnerships to alleviate pressure on the public system and enhance overall healthcare capacity and quality across the country.

Regional Insights

Ho Chi Minh City Drives Southern Vietnam's Hospital Market

Southern Vietnam leads the national hospital market, predominantly driven by Ho Chi Minh City's role as a major economic and financial hub. This concentration fosters substantial healthcare investment and advanced infrastructure development within the region. The city's high population density and significant urbanization generate a large and diverse patient base, fueling strong demand for both general and specialized medical services. Consequently, Southern Vietnam benefits from a greater number of top-tier hospitals, specialized clinics, and private healthcare facilities, further attracting patients and medical tourists. Local authorities, such as the Ho Chi Minh City People's Committee, actively support infrastructure expansion and healthcare system restructuring, reinforcing the region's market dominance.

Recent Developments

-

In April 2025, GE HealthCare and the global IT firm FPT announced a Strategic Cooperation Agreement to expand their commercial alliance, driving digital transformation in the Vietnam Hospital Market. This partnership evolved from project-based engagements to a long-term alliance, with FPT becoming a channel partner for promoting and delivering GE HealthCare’s digital solutions across Vietnam. A key component of the agreement included the establishment of an FPT Competency Center in Vietnam, dedicated to supporting product strategy, innovation, and co-developing new digital healthcare products to enhance operational efficiency and patient care.

-

In September 2024, Vinmec Healthcare System achieved a significant breakthrough in the Vietnam Hospital Market by successfully performing the first 3D-printed titanium chest reconstruction surgery in Southeast Asia. This complex procedure, conducted at Vinmec Times City International Hospital, involved the radical removal of an 11.5 cm mediastinal tumor and subsequent chest wall reconstruction using patient-specific 3D-printed titanium material. This innovation represented a new direction in the treatment of cardiopulmonary conditions, particularly for patients requiring artificial bones, setting a new standard for high-tech medical interventions within the region.

-

In June 2024, Hoa Lam Group and Siemens Healthineers entered into a strategic partnership aimed at enhancing high-quality healthcare services in Vietnam. This collaboration positioned Siemens Healthineers as a key technology partner, responsible for providing advanced medical imaging equipment, including modern CT scanners, MRI machines, and mammography systems, to hospitals under Hoa Lam Group. The partnership also focused on establishing and developing oncology and nuclear medicine centers, alongside efforts to standardize and improve the digital capabilities of Hoa Lam's medical facilities through AI tools and general management consulting services.

-

In May 2024, Hoan My Medical Group, Vietnam's largest private healthcare network, significantly increased its advanced medical care capabilities and expanded its clinical network. The group invested in state-of-the-art equipment to support diagnoses and enhance surgical capabilities across various specialties, including vascular, cardiac, and orthopedics. This expansion also saw the launch of the Hoan My Tan Phu Medical Centre in Ho Chi Minh City, marking the network's first large-scale polyclinic model. These initiatives aimed to meet the growing demand for early detection and effective treatment of complex diseases, while simultaneously increasing bed capacity across its 14 hospitals and seven clinics.

Key Market Players

- Cleveland Clinic

- Burjeel Hospital

- American Hospital

- NMC Royal Hospital

- Mediclinic

- Aster Hospital

- Mafraq Hospital

- Sheikh Shakhbout Medical City

- Zayed Military Hospital

- Rashid Hospital

|

By Ownership

|

By Type

|

By Type of Services

|

By Bed Capacity

|

By Region

|

|

|

- General

- Multispecialty

- Specialty

|

- In-Patient Services and Out-Patient Services

|

- Above 500 beds

- 100-500 beds

- up to 100 beds

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam Hospital Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam Hospital Market, By Ownership:

-

Vietnam Hospital Market, By Type:

-

General

-

Multispecialty

-

Specialty

-

Vietnam Hospital Market, By Type of Services:

-

In-Patient Services and Out-Patient Services

-

Vietnam Hospital Market, By Bed Capacity:

-

Above 500 beds

-

100-500 beds

-

up to 100 beds

-

Vietnam Hospital Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam Hospital Market.

Available Customizations:

Vietnam Hospital Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam Hospital Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com