|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

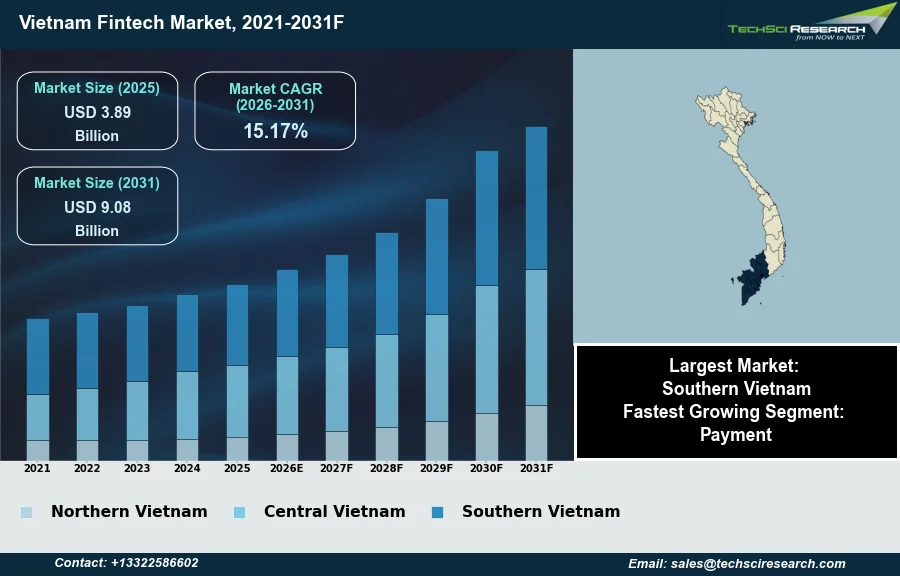

Market Size (2025)

|

USD 3.89 Billion

|

|

CAGR (2026-2031)

|

15.17%

|

|

Fastest Growing Segment

|

Payment

|

|

Largest Market

|

Southern Vietnam

|

|

Market Size (2031)

|

USD 9.08 Billion

|

Market Overview

The Vietnam Fintech Market will grow from USD 3.89 Billion in 2025 to USD 9.08 Billion by 2031 at a 15.17% CAGR. Financial technology, commonly known as Fintech, refers to the innovative application of technology to enhance and automate financial services, encompassing various domains such as digital payments, lending, and wealth management. The Vietnam Fintech market's expansion is primarily propelled by high mobile internet penetration, a considerable segment of unbanked and underbanked individuals seeking accessible financial solutions, and proactive governmental policies fostering digital transformation within the financial sector.

According to the Vietnam Banks Association, in the first 11 months of 2025, QR Code transactions demonstrated substantial growth, increasing by 54.45% in volume and 141.02% in value. A significant impediment to sustained market expansion is the continuously evolving and occasionally fragmented regulatory framework, which necessitates constant adaptation from market participants to ensure compliance and build consumer confidence.

Key Market Drivers

E-commerce Growth Drives Fintech Adoption

The rapid expansion of e-commerce and digital payments significantly drives the Vietnam Fintech market, fostering an environment where cashless transactions are increasingly prevalent across various sectors. The burgeoning online retail landscape necessitates robust digital payment infrastructure, directly accelerating the adoption of fintech solutions such as e-wallets, mobile banking, and instant payment systems. According to the National Payment Corporation of Vietnam (NAPAS), in March 2026, Vietnam's online payment market recorded a significant milestone, with transaction volumes increasing by more than 25% in 2025 compared to 2024. This growth underscores a clear shift in consumer behavior towards digital channels for everyday transactions, integrating fintech services deeper into daily economic activities.

Venture Capital Fuels Fintech Expansion

Increasing venture capital investment in Fintech is another pivotal factor propelling the market, providing essential funding for innovation and expansion. This influx of capital enables fintech startups to develop new technologies, scale operations, and enhance service offerings, thereby attracting more users and fostering market maturity. According to the Vietnam Innovation and Private Capital Investment Report 2026, published in May 2026, venture capital funding in Vietnam rose to US$508 million, marking a 28% increase from a year earlier. This capital infusion supports the development of diverse fintech sub-segments. Concurrently, the overall market demonstrates substantial user adoption; according to a report released by the State Bank of Vietnam in February 2026, the number of individual payment accounts had exceeded 232 million by December 2025, representing a 13.68% increase compared to the same period in 2024. This highlights the broad reach and acceptance of digital financial services.

Download Free Sample Report

Key Market Challenges

Regulatory Fragmentation Elevates Compliance Costs and Delays Market Entry

The continuously evolving and occasionally fragmented regulatory framework is a significant challenge for the Vietnam Fintech market. This environment necessitates constant adaptation from market participants, diverting resources towards compliance rather than innovation or expansion. The ambiguity and frequent changes in regulations create uncertainty, which can deter both domestic and international investment. Companies face increased operational costs due to the need for dedicated legal and compliance teams to monitor and interpret new guidelines, potentially delaying product launches and market entry for new services.

Regulatory Unpredictability Hampers Growth and Investor Confidence

Such regulatory unpredictability directly hampers market growth by increasing the risk profile for fintech ventures. This complexity makes it harder for companies to scale operations efficiently or introduce new offerings across various sectors without extensive regulatory navigation. According to the State Bank of Vietnam, by the end of 2025, the value of cashless transactions reached approximately 28 times the country's GDP. While this highlights a robust digital payment landscape, the underlying regulatory environment's fragmented nature complicates sustained innovation and investor confidence necessary for future growth beyond basic transactional volumes.

Key Market Trends

Expansion of digital lending and alternative financing in Vietnam

The expansion of digital lending and alternative financing solutions represents a significant trend within the Vietnam Fintech market, addressing the credit needs of underserved segments, including individuals and small and medium-sized enterprises. These innovative models leverage technology to provide more accessible and flexible credit options beyond traditional banking channels. The increasing demand for such services indicates a growing reliance on non-traditional avenues for capital. For example, the International Finance Corporation is considering providing up to $86 million in long-term financing to Vietnam's Southeast Asia Commercial Joint Stock Bank (SeABank) to expand lending to small businesses, women entrepreneurs, and affordable housing, according to Crowdfund Insider, June 2026. This trend is further supported by the emergence of new-generation pawnshop chains and a rise in payday lending platforms, indicating diversification in available credit products.

AI adoption in Vietnam's financial sector

Another pivotal trend transforming the Vietnam Fintech market is the increasing integration of artificial intelligence in financial services. AI applications are enhancing operational efficiencies, personalizing customer experiences, and strengthening risk management frameworks across various financial institutions. This technological adoption moves beyond initial experimentation, becoming embedded in core operations. According to the Finastra Financial Services State of the Nation 2026 report, released in February 2026, 94% of financial institutions in Vietnam plan to increase investment in artificial intelligence over the next 12 months, signaling a decisive shift in the country's banking landscape. Such investments are prioritized to improve payment and lending processing speeds, reinforcing the strategic imperative of AI in modernizing the financial sector.

Segmental Insights

Payments Growth Fueled by Digital Adoption and SBV Cashless Initiatives

In the dynamic Vietnam Fintech Market, the Payment segment stands out as the fastest-growing area, driven by a convergence of favorable factors. This rapid expansion is primarily fueled by high smartphone penetration and extensive internet usage, which have cultivated a tech-savvy population accustomed to digital interactions. Furthermore, the Vietnamese government's proactive initiatives, championed by the State Bank of Vietnam (SBV), actively promote a cashless economy through supportive policies and regulatory frameworks, such as Decree No. 52/2024/ND-CP on cashless payments. This environment fosters widespread adoption of convenient digital payment solutions like mobile wallets and QR code transactions, further propelled by the booming e-commerce sector and the seamless integration of payments within various digital platforms.

Regional Insights

Southern Vietnam: A Leading Fintech Hub Fueled by Urban Growth, Investment, and Institutional Support

Southern Vietnam is the leading region in the Vietnam Fintech Market, primarily driven by its robust economic foundation and high urbanization, particularly in Ho Chi Minh City. This key commercial and financial center cultivates a dense ecosystem of enterprises, startups, and digitally active consumers, driving demand for digital financial services. The region boasts a thriving fintech environment, attracting investment and housing numerous startups, traditional financial institutions, and technology accelerators. High technology adoption, including extensive smartphone penetration and widespread internet access, further accelerates the uptake of innovative financial solutions. Institutional support, such as the Ho Chi Minh City People's Committee’s initiatives and the new Fintech Hub, solidifies the region's prominent position.

Recent Developments

-

In July 2025, Cake Digital Bank announced a strategic collaboration with Mobile World Investment Corporation (MWG) to launch MWG PayLater, a new product in the Vietnam Fintech Market. This service marked MWG’s first branded buy-now-pay-later offering within its retail ecosystem, providing flexible payment solutions for mass-market consumers purchasing items like mobile devices and home appliances. Cake Digital Bank functioned as the exclusive provider of both credit capital and the underlying technology infrastructure, leveraging its expertise in digital finance to expand accessible credit options for customers across MWG's extensive retail network.

-

In February 2025, TPBank introduced its innovative ChatPay feature, earning recognition as the "Best Social Banking Initiative in Asia Pacific 2025." This breakthrough integrated artificial intelligence (AI) and advanced security technologies directly into popular messaging platforms. Customers could execute various financial transactions, such as money transfers and bill payments, while engaging in chat conversations. The system utilized generative AI (GenAI) and Optical Character Recognition (OCR) technology to facilitate quick transfers by simply pasting payment information from messages, thereby streamlining the digital payment experience in the Vietnam Fintech Market.

-

In November 2024, Vietcombank and Global Telecommunications Technology Corporation (GTEL) collaborated to introduce a service enabling the linkage of Vietcombank accounts with the GtelPay e-wallet. This partnership allowed customers holding a Vietcombank current account and utilizing VCB Digibank to seamlessly transfer funds between their bank accounts and the GtelPay e-wallet. The initiative aimed to provide greater flexibility and accessibility for digital transactions within the Vietnam Fintech Market, offering customers a convenient method for managing their funds without incurring fees for linking accounts or conducting deposit/withdrawal operations.

-

In October 2024, Vietnam International Bank (VIB) pioneered a new product launch in the Vietnam Fintech Market by becoming the first bank to issue credit cards online through integration with the VNeID electronic identification and authentication system. This innovative process allowed customers with a level-2 VNeID account to apply for a credit card in approximately three to five minutes, with card issuance typically completed within 15 to 30 minutes. This development enhanced the efficiency of credit card applications and strengthened data security by directly connecting with the national identification system.

Key Market Players

- Bayzat

- Tabby

- Tamara

- PayTabs

- Telr

- HyperPay

- Mamo Pay

- Salla

- Zand Bank

- Rain

|

By Technology

|

By Service

|

By Application

|

By Region

|

- API

- AI

- Blockchain

- Distributed Computing

- Others

|

- Payment

- Fund Transfer

- Personal Finance

- Loans

- Insurance

- Others

|

- Banking

- Insurance

- Securities & Others

|

- Northern

- Central

- Southern

|

Report Scope:

In this report, the Vietnam Fintech Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Vietnam Fintech Market, By Technology:

-

API

-

AI

-

Blockchain

-

Distributed Computing

-

Others

-

Vietnam Fintech Market, By Service:

-

Payment

-

Fund Transfer

-

Personal Finance

-

Loans

-

Insurance

-

Others

-

Vietnam Fintech Market, By Application:

-

Banking

-

Insurance

-

Securities & Others

-

Vietnam Fintech Market, By Region:

-

Northern

-

Central

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Vietnam Fintech Market.

Available Customizations:

Vietnam Fintech Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Vietnam Fintech Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com