|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

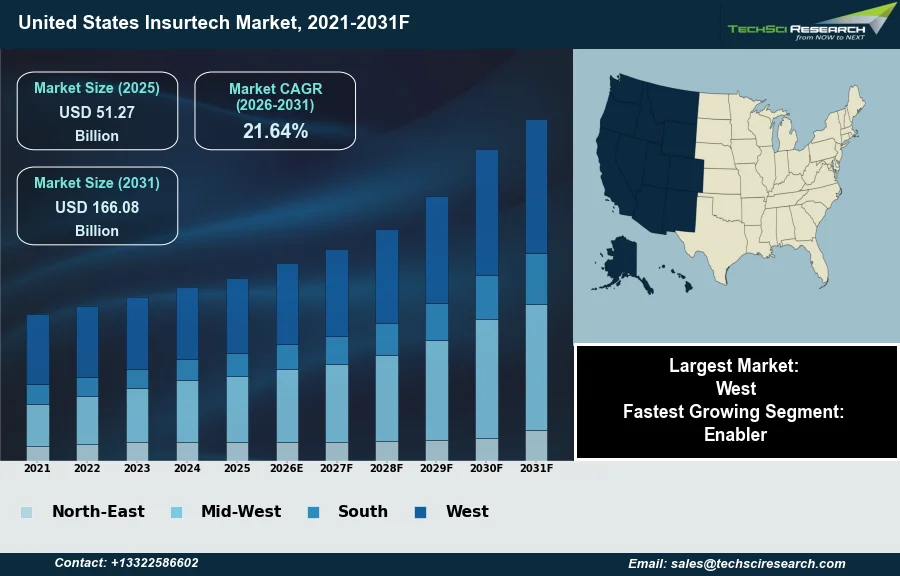

Market Size (2025)

|

USD 51.27 Billion

|

|

CAGR (2026-2031)

|

21.64%

|

|

Fastest Growing Segment

|

Enabler

|

|

Largest Market

|

West

|

|

Market Size (2031)

|

USD 166.08 Billion

|

Market Overview

The United States Insurtech Market will grow from USD 51.27 Billion in 2025 to USD 166.08 Billion by 2031 at a 21.64% CAGR. Insurtech, an abbreviation for insurance technology, encompasses the application of innovative technologies to enhance efficiency, customer experience, and product offerings across the insurance value chain. The United States Insurtech market growth is primarily supported by the increasing consumer expectation for digital services, the insurance industry's drive for operational efficiencies through automation, and the proliferation of accessible data analytics capabilities. For instance, according to the National Association of Insurance Commissioners, in 2026, its Big Data and Artificial Intelligence Working Group is piloting an AI Systems Evaluation Tool across 12 participating states, demonstrating significant regulatory engagement with advanced technologies.

Despite these drivers, a significant impediment to market expansion remains the complex and fragmented regulatory landscape across individual states. Adhering to diverse state-specific compliance requirements often necessitates substantial legal and operational resources, creating a formidable barrier for new entrants and hindering the rapid scaling of innovative solutions.

Key Market Drivers

AI/ML Adoption Elevates Analytics, Personalization, and Efficiency in US Insurtech

Advanced Artificial Intelligence and Machine Learning Adoption is a pivotal driver transforming the United States Insurtech Market by enabling sophisticated analytics and automation. These technologies allow insurers to significantly enhance their capabilities in risk assessment, fraud detection, and personalized product development. AI-powered tools streamline operational processes, from underwriting to claims management, fostering greater efficiency. According to the International Risk Management Institute, in its June 2026 "2025 Insurance Year in Review and 2026 Developments" article, approximately 77 percent of insurers in the US reported piloting or implementing AI initiatives in 2025, demonstrating widespread engagement with these advanced solutions. This integration facilitates the creation of dynamic and usage-based insurance models that better cater to evolving consumer preferences and risk profiles.

Venture Capital Funding Accelerates Insurtech Innovation

Increased Venture Capital Funding and Startup Innovation further propels the market by injecting capital necessary for the development and scaling of disruptive insurtech solutions. This financial support empowers new entrants to introduce novel business models and technological advancements that challenge traditional insurance practices. The influx of investment fosters a competitive environment, stimulating both incumbent insurers and startups to accelerate innovation and digital transformation. According to Reinsurance News, in its February 2026 article "Global Insurtech Funding Surges on Record Re/Insurance Investments: Gallagher Re," the global deal share of U.S.-based insurtechs rose to 55.74% in 2025, highlighting the nation's leading role in attracting investment for insurance technology. Moreover, the broader financial health of the sector provides a favorable backdrop; according to the International Risk Management Institute, in 2025, US property and casualty insurers posted a net underwriting gain of approximately $60.9 billion.

Download Free Sample Report

Key Market Challenges

State-by-State Regulatory Fragmentation Hampers Insurtech Growth

The complex and fragmented regulatory landscape across individual states represents a significant impediment to the growth of the United States Insurtech market. This environment necessitates that insurtech firms allocate substantial legal and operational resources to navigate diverse state-specific compliance requirements. Such extensive demands create a formidable barrier for new entrants and significantly hinder the rapid scaling of innovative insurance solutions. The requirement to secure approvals and adhere to varying rules in each jurisdiction prolongs market entry and increases operational costs, diverting capital and effort from product development and customer acquisition.

Protracted State Regulatory Reviews Constrain Agility and Expansion

For instance, according to the American Property Casualty Insurance Association, in December 2025, the New York Department of Financial Services required an average of 285 days to review each insurer request for a rate or filing change, exemplifying the protracted timelines associated with navigating individual state regulations. This complexity ultimately stifles the agility and expansion potential critical for insurtech innovation by increasing the time and cost involved in bringing new offerings to market across multiple jurisdictions.

Key Market Trends

Embedded Insurance at the Point of Sale

The Rise of Embedded Insurance Offerings represents a significant trend in the United States Insurtech market, fundamentally altering traditional distribution models by integrating coverage directly into the purchase of products and services. This approach enhances customer convenience by providing immediate, contextually relevant protection at the point of sale, eliminating separate application processes. Insurtechs leverage APIs to seamlessly embed insurance into various digital platforms, from e-commerce sites to mobility services, fostering new partnerships and revenue streams. According to the U.S. Census Bureau, in its May 2026 'Quarterly Retail E-Commerce Sales Report', e-commerce sales in the first quarter of 2026 increased 9.7 percent from the first quarter of 2025. This reflects the growing digital environments where embedded insurance thrives.

IoT and Telematics for Dynamic Risk Assessment

The Widespread Adoption of IoT and Telematics for Dynamic Risk Assessment is another transformative trend, enabling insurers to gather real-time data on asset usage and behavior. This technology, particularly prevalent in auto and home insurance, moves beyond static demographic factors to create highly personalized risk profiles. Telematics devices and applications monitor driving habits or property conditions, allowing for usage-based insurance models and proactive loss prevention. According to the Insurance Information Institute, in its June 2026 'U.S. Telematics Market Size, Share, & Growth, 2034' report, personal auto insurance premiums in the United States rose by 16.8% in 2023, creating an incentive for consumers to adopt telematics programs. This data-driven approach enables more accurate underwriting and improved customer engagement.

Segmental Insights

Enablers Drive Rapid Modernization in US Insurtech

Within the United States Insurtech Market, the Enabler segment is experiencing the most rapid expansion, serving as a critical catalyst for industry modernization. Enablers provide essential technology infrastructure, such as API-driven solutions, software, and data analytics platforms, directly to incumbent insurance carriers and managing general agents. This rapid growth stems from the strong demand among traditional insurers to enhance operational efficiency, reduce costs, and deliver superior customer experiences without replacing their core systems entirely. By integrating advanced technologies like artificial intelligence and machine learning, Enablers empower these established players to streamline underwriting, improve claims processing, and introduce personalized products, thereby driving digital transformation across the insurance value chain.

Regional Insights

West Leads U.S. Insurtech Through Tech Strength, VC Funding, and Digital Transformation

The West stands as the leading region in the United States Insurtech Market, driven primarily by its robust technology sector and extensive startup ecosystems. This dominance is significantly fueled by the substantial presence of venture capital, particularly in California's Silicon Valley, which attracts crucial investment for insurtech innovation. Regional carriers widely adopt digital insurance platforms and allocate considerable budgets to digital transformation initiatives, further accelerating market growth. The region benefits from a concentrated pool of innovative talent and established innovation hubs, fostering a dynamic environment for developing advanced insurance technologies. This unique combination of capital, technological infrastructure, and entrepreneurial culture solidifies the West's market leadership.

Recent Developments

-

In February 2025, Duck Creek Technologies, a provider of solutions for the property and casualty and general insurance industry, announced a strategic partnership with Worldpay, a global leader in payments technology. This collaboration was designed to enhance payment processing capabilities for insurers in the United States, offering a scalable solution for the industry's evolving requirements. The integration of Worldpay’s global payments infrastructure into Duck Creek Payments aimed to provide carriers with a streamlined, comprehensive payment management platform, thereby improving operational efficiency for U.S. insurtech stakeholders.

-

In January 2025, the American InsurTech Council (AITC) and the InsurTech Association (ITA) formed a strategic alliance to guide the integration of artificial intelligence and digital technologies within the United States insurance sector. This collaboration aimed to provide crucial insights to policymakers developing regulatory standards for AI in insurance. By combining their expertise, the non-profit organizations sought to foster innovation in regulatory policies and drive positive industry transformation, specifically in technology adoption and advancement, for the benefit of insurtech companies operating in the U.S.

-

In October 2024, MassMutual, a prominent United States insurer, introduced free access to Wysa Assure for its eligible policyholders. This AI-powered conversational mental health application was developed by Wysa in collaboration with Swiss Re. The offering marked MassMutual as the first insurer in the U.S. to provide such an AI-guided mental health support service. This initiative represented a new product launch aimed at leveraging artificial intelligence to enhance policyholder well-being and demonstrated a commitment to integrating advanced technology within the U.S. insurtech landscape for customer support.

-

In July 2024, Insurity, a cloud software provider for insurance carriers, brokers, and managing general agents in the United States, announced a strategic partnership with Coherent. Coherent operates a platform dedicated to streamlining and accelerating insurance product development. This collaboration sought to improve capabilities for property and casualty insurance organizations by facilitating system modernization and enhancing operational efficiency within the U.S. insurtech market. A key aspect of the partnership involved Coherent's Spark solution, which translates traditional spreadsheet business logic into user-friendly application programming interfaces.

Key Market Players

- Lemonade Inc.

- Root Inc.

- Hippo Holdings Inc.

- Oscar Health Inc.

- Clover Health Investments Corp.

- Next Insurance Inc.

- Policygenius Inc.

- Metromile Inc.

- Bolttech Management Limited

- Shift Technology S.A.

|

By Insurance Type

|

By Business Model

|

By Region

|

- Life Insurance

- Non-Life Insurance

|

- Enabler

- Carrier

- Distributor

|

- Northeast

- Midwest

- South

- West

|

Report Scope:

In this report, the United States Insurtech Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

United States Insurtech Market, By Insurance Type:

-

Life Insurance

-

Non-Life Insurance

-

United States Insurtech Market, By Business Model:

-

Enabler

-

Carrier

-

Distributor

-

United States Insurtech Market, By Region:

-

Northeast

-

Midwest

-

South

-

West

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the United States Insurtech Market.

Available Customizations:

United States Insurtech Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

United States Insurtech Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com