|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 38.77 Billion

|

|

CAGR (2026-2031)

|

7.91%

|

|

Fastest Growing Segment

|

New Construction

|

|

Largest Market

|

Dubai

|

|

Market Size (2031)

|

USD 61.22 Billion

|

Market Overview

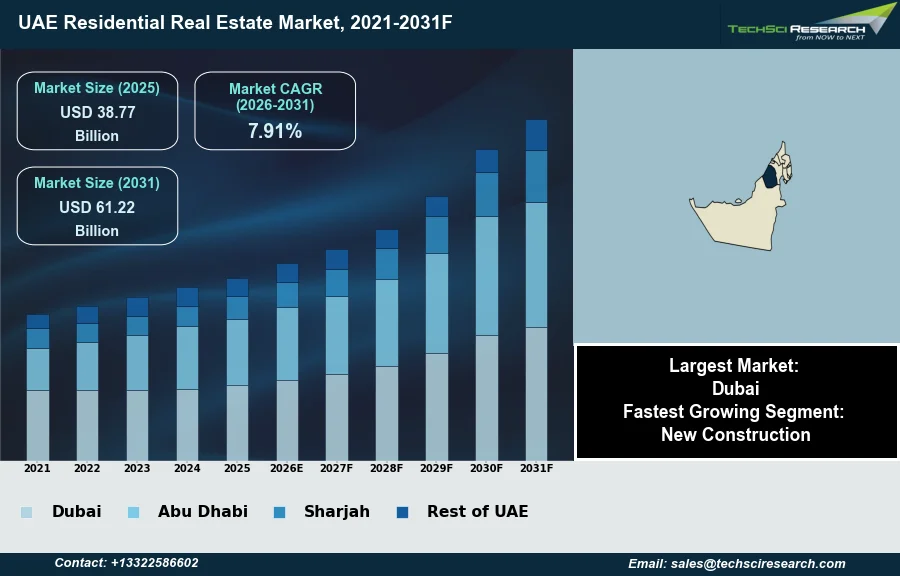

The UAE Residential Real Estate Market will grow from USD 38.77 Billion in 2025 to USD 61.22 Billion by 2031 at a 7.91% CAGR. The UAE Residential Real Estate Market comprises properties for habitation, including apartments, villas, and townhouses, spanning ownership and rental arrangements. Key growth drivers include progressive government visa reforms, sustained economic diversification, strategic infrastructure development, and robust population expansion from expatriate inflows. According to the Dubai Land Department, in Q1 2026, total residential real estate transactions in Dubai reached AED 252 billion, reflecting a 31% year-on-year increase in value.

Investor-friendly policies and a transparent regulatory environment further bolster this growth. However, a significant challenge that could impede market expansion is the potential for oversupply within specific urban sub-segments, potentially increasing competition and pressuring pricing. According to the Abu Dhabi Real Estate Centre, in 2025, residential unit sales in Abu Dhabi reached AED 76.1 billion across 23,600 transactions, representing a 67% increase in value compared to the prior year.

Key Market Drivers

Population Growth and Long-Term Residency Drive Housing Demand

Increasing population and sustained expatriate inflows significantly bolster the UAE residential real estate market by generating consistent demand for various property types. Progressive government policies, including new visa reforms, actively attract skilled professionals, entrepreneurs, and families seeking long-term residency, transforming the UAE into a more permanent home rather than a temporary work destination. This sustained influx directly translates into a higher requirement for both owned and rented accommodations across apartments, villas, and townhouses. For instance, according to the Dubai Statistics Center, as of June 2025, Dubai's population surpassed 3.75 million. This demographic expansion creates a fundamental demand floor, driving residential absorption rates and supporting the overall market's resilience and growth trajectory.

Investor Confidence and Capital Inflows Drive Market Momentum

Robust investor confidence and substantial foreign direct investment continue to be pivotal drivers for the UAE residential real estate market, infusing significant capital and stimulating development activity. The transparent regulatory environment, coupled with attractive returns and a diversified economy, positions the UAE as a secure and appealing destination for global investors. This confidence is evident in the substantial capital inflows, particularly into the luxury and off-plan segments. According to data from the Dubai Land Department, as cited by ZAWYA, foreign investment value in Dubai's real estate sector rose to AED148.35 billion in Q1 2026, marking a 26% increase. This sustained investment also reflects in the broader market activity; for example, according to data from the Dubai Land Department, as reported by Provident Estate, Dubai's market recorded more than 270,000 real estate transactions with a total value of approximately AED 917 billion in 2025.

Download Free Sample Report

Key Market Challenges

Oversupply Risks and Shifting Market Leverage

A significant challenge impeding the growth of the UAE Residential Real Estate Market is the potential for oversupply within specific urban sub-segments. This directly increases market competition and pressures pricing dynamics. A notable influx of new properties grants buyers and tenants more extensive options, thereby shifting market leverage and encouraging a more selective approach to property acquisition and leasing.

Supply Surge and Its Impacts on Rents and Values

The impact of this heightened supply is evident in market performance metrics. According to ValuStrat, a record estimated supply pipeline of 131,234 new residential units is forecasted for Dubai in 2026. This substantial volume of new inventory contributes to increased competition among developers and property owners. Consequently, rental growth is anticipated to stabilize, with ValuStrat expecting a 0% increase in 2026 as rents approach affordability and demand thresholds across key segments. Furthermore, according to Cavendish Maxwell, residential prices in Dubai rose 12.1% in 2025, marking a deceleration from the 16.5% growth recorded in 2024, indicating the moderating effect of increasing supply on overall market momentum. These trends collectively suggest direct pressure on property values and rental yields, influencing investment returns and market liquidity.

Key Market Trends

Shift toward Long-Term Resident Ownership and Permanent Habitation

The UAE residential real estate market is increasingly witnessing a significant shift towards long-term resident and end-user ownership, moving beyond its historical reliance on short-term speculative investment. This trend is driven by progressive government policies that encourage extended residency, fostering a deeper sense of commitment among residents. Such stability transforms the market into a destination for permanent habitation rather than temporary stay, aligning property acquisitions with lifestyle and family needs. According to Arabian Business, May 2026, in the article 'Dubai real estate market shifts from boom to long-term growth story as investor confidence holds,' resident investors accounted for more than half of all investment by value during 2025, signaling a clear move away from purely speculative activity.

Rising Demand for Villas and Low-Density Housing

Another prominent trend is the sustained premium on villas and low-density housing, reflecting evolving buyer preferences for spacious living environments, privacy, and community amenities. This preference is particularly pronounced among families and those seeking an upgraded lifestyle, as opposed to the previously dominant apartment segments. The limited supply of such properties in established and desirable locations further exacerbates this demand, leading to notable price appreciation. According to fäm Properties and DXBinteract, April 2026, in their Q1 2026 market data, median villa prices in the primary market increased by 35.3% to AED 4.1 million, underscoring the strong demand for larger-format residential units.

Segmental Insights

Government Policy and Strategic Planning Drive Fastest-Growing New Construction

The New Construction segment stands as the fastest-growing area within the UAE Residential Real Estate Market, primarily propelled by robust government initiatives and sustained population expansion. Strategic urban development plans, such as the Dubai 2040 Urban Master Plan and Abu Dhabi Economic Vision 2030, actively foster an environment conducive to new projects by enhancing infrastructure and promoting economic diversification. This growth is further underpinned by favorable regulatory frameworks introduced by bodies like the Dubai Land Department and the Real Estate Regulatory Agency (RERA), alongside supportive visa policies that attract a growing expatriate and investor base seeking modern, high-quality residential offerings.

Regional Insights

Dubai as the Leading Regional Driver: Diversification, Policy Support, and Regulatory Oversight

The UAE residential real estate market demonstrates robust performance, with Dubai consistently emerging as the leading regional driver. Dubai's dominance stems from its strategic economic diversification efforts, significantly reducing reliance on oil and fostering growth in trade, tourism, and finance. This stability is augmented by comprehensive government policies, including investor-friendly long-term visa options and clear freehold ownership regulations for expatriates. The Dubai Land Department (DLD) and its regulatory arm, the Real Estate Regulatory Agency (RERA), play a crucial role in ensuring market transparency and investor protection through robust transactional oversight and escrow account supervision for off-plan developments. Furthermore, continuous investment in world-class infrastructure and its status as a global connectivity hub enhance its appeal to international investors and residents alike.

Recent Developments

-

In August 2025, EBG Realty announced a strategic collaboration with Alba Homes, a real estate company based in Dubai, to facilitate property investments for Indian buyers in the Dubai market. This partnership provides Indian investors with access to a portfolio of properties and local market expertise through an advisory-led approach. The collaboration includes exclusive listings, insights into the local market, and comprehensive transactional support, aiming to streamline the investment journey for international clients in the UAE Residential Real Estate Market.

-

In July 2025, Dubai initiated a new program aimed at first-time homebuyers residing in the UAE, designed to encourage homeownership within the emirate. This initiative involved a collaboration supported by 13 developers and five banks, offering discounted property prices, more favorable mortgage terms, and waived registration fees for eligible properties under AED 5 million. The program's objective was to convert long-term renters into homeowners, thereby stimulating growth and stability within the UAE Residential Real Estate Market.

-

In January 2025, DAMAC Properties introduced Riverside Views, its initial residential development for the year, positioned within the recently launched DAMAC Riverside community in Dubai. This project combines urban accessibility with suburban appeal, offering one and two-bedroom apartments distributed across eight distinctively themed clusters. The design emphasizes connecting residents with nature and community through ample green spaces and water features. Riverside Views aimed to offer a wellness-centric lifestyle within the competitive UAE Residential Real Estate Market.

-

In July 2024, Emaar Properties launched Palace Residences Creek Blue, a new residential development situated in Dubai Creek Harbour. The project offers a selection of one to three-bedroom apartments, designed to provide residents with contemporary living spaces. Amenities within the complex include a multi-purpose area, a games zone, a swimming pool, a glass-enclosed gymnasium, and dedicated barbecue spots. The development aimed to cater to demand for upscale residential units in a sought-after waterfront location within the UAE Residential Real Estate Market.

Key Market Players

- Emaar Properties PJSC

- DAMAC Properties

- Meraas Holding

- Nakheel

- Wasl Asset Management

- Aldar Properties

- Majid Al Futtaim Properties

- Dubai Properties

- Jumeirah Group

- Emirates Real Estate

|

By Type

|

By Category

|

By Mode

|

By Region

|

|

|

- Flats & Apartments

- Individual Houses or Private Dwellings

- Condominium

- Townhouses

- Others

|

|

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

|

Report Scope:

In this report, the UAE Residential Real Estate Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

UAE Residential Real Estate Market, By Type:

-

UAE Residential Real Estate Market, By Category:

-

Flats & Apartments

-

Individual Houses or Private Dwellings

-

Condominium

-

Townhouses

-

Others

-

UAE Residential Real Estate Market, By Mode:

-

UAE Residential Real Estate Market, By Region:

-

Dubai

-

Abu Dhabi

-

Sharjah

-

Rest of UAE

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the UAE Residential Real Estate Market.

Available Customizations:

UAE Residential Real Estate Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

UAE Residential Real Estate Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com