|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 1.56 Billion

|

|

CAGR (2026-2031)

|

11.27%

|

|

Fastest Growing Segment

|

Epoxy-Coated Rebar

|

|

Largest Market

|

Dubai

|

|

Market Size (2031)

|

USD 2.96 Billion

|

Market Overview

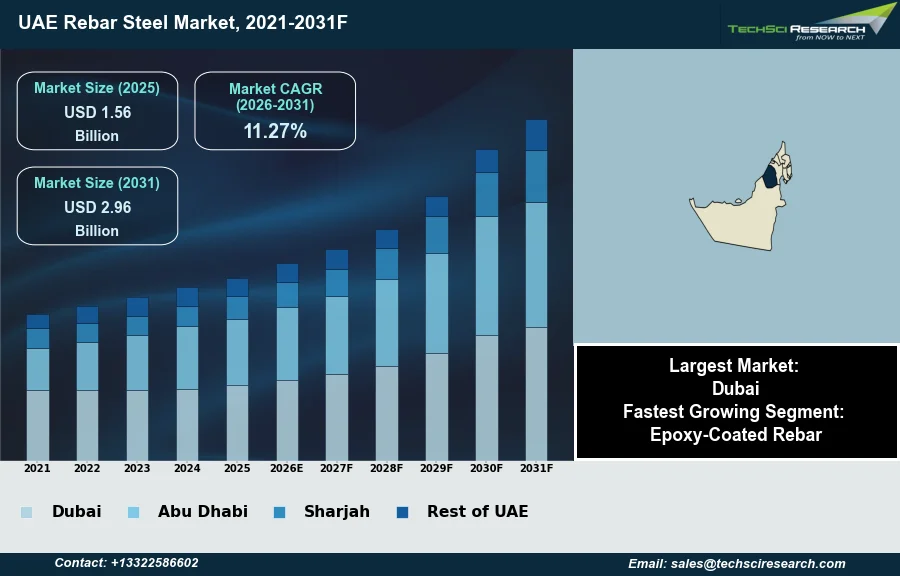

The UAE Rebar Steel Market will grow from USD 1.56 Billion in 2025 to USD 2.96 Billion by 2031 at a 11.27% CAGR. Rebar steel, or reinforcing bar, is a fundamental construction material extensively utilized to enhance the tensile strength of concrete and masonry structures, thereby preventing cracking and structural failure. The UAE Rebar Steel Market's expansion is significantly supported by robust construction and infrastructure development, encompassing numerous mega-projects in urban, residential, and transport sectors across the Emirates. Additionally, government investment in economic diversification initiatives, such as the UAE Vision 2030, actively stimulates demand across the construction and industrial landscape. According to the World Steel Association, the UAE produced 3.7 million tons of crude steel in 2024, demonstrating the scale of domestic industrial output supporting these developments.

Continued rapid urbanization, particularly in major cities like Dubai and Abu Dhabi, further underpins the sustained demand for rebar in various building projects. However, a significant challenge impeding market expansion is the volatility in raw material prices, notably iron ore and scrap metal, exacerbated by global supply chain disruptions and geopolitical dynamics that directly influence production costs.

Key Market Drivers

Infrastructure Pipeline as Primary Catalyst for Rebar Demand

Robust Infrastructure and Mega Project Pipeline stands as a primary catalyst for the UAE Rebar Steel Market, directly fueling demand through extensive development activities. The sheer scale of ongoing and planned projects, particularly in major urban centers, necessitates a substantial and consistent supply of reinforcing steel. For instance, Dubai’s record-breaking budget for 2026 allocates approximately AED 47.8 billion towards infrastructure and construction projects, signaling continued investment in large-scale developments such as the expansion of Al Maktoum International Airport and the Dubai Metro Blue Line. This sustained pipeline ensures a steady requirement for rebar in foundations, structural frameworks, and intricate architectural designs, underpinning market stability and growth.

Diversification and Non-Oil Growth Propel Rebar Demand

Concurrently, Strategic Government Vision and Economic Diversification Plans significantly bolster the market by driving non-oil sector expansion, with construction at its core. The UAE’s commitment to reduce reliance on hydrocarbons has spurred substantial investments in various sectors including tourism, logistics, and manufacturing, all requiring new facilities and infrastructure. This strategic direction led to the UAE's non-oil gross domestic product increasing by 6.8% in 2025, with the construction sector itself demonstrating an impressive 11.1% growth, showcasing its critical role in the diversification agenda. Such robust activity across diverse segments of the economy supports the broader rebar market, with monthly rebar demand in the country experiencing growth from 350,000 tonnes in January 2025 to 500,000 tonnes by November 2025.

Download Free Sample Report

Key Market Challenges

Raw-material price volatility constrains UAE rebar market expansion

A significant challenge impeding the expansion of the UAE Rebar Steel Market is the volatility in raw material prices, notably for iron ore and scrap metal. These fluctuations, often driven by global supply chain disruptions and complex geopolitical dynamics, directly increase production costs for rebar manufacturers. Such instability in input costs makes it difficult for construction firms and developers in the UAE to undertake accurate financial planning and long-term project budgeting.

Scrap-price outlook to raise rebar costs and curb construction investment

For example, according to the World Steel Association's Short Range Outlook from October 2025, ferrous scrap prices (Turkish HMS 1&2 (80:20), CFR basis) are projected to remain within a range of $350 to $380 per ton through 2026 and 2027. This demonstrates ongoing price movement for essential raw materials. When raw material costs are unpredictable, rebar producers either absorb reduced profit margins or transfer these higher expenses to consumers. This directly leads to elevated rebar prices, which subsequently inflates the overall cost of construction projects across the Emirates. This upward pressure on project expenses can deter new investments, cause delays in ongoing developments, or necessitate re-evaluations of project viability, thereby directly restricting the growth of the UAE's infrastructure and construction sectors. The resulting market uncertainty undermines investor confidence and amplifies financial risks throughout the entire rebar supply chain.

Key Market Trends

Rise of Low-Carbon Rebar Driven by Regulation and Sustainability

Increased adoption of sustainable and low-carbon rebar production is a pivotal trend transforming the UAE Rebar Steel Market. This shift is driven by a growing environmental consciousness, stringent regulatory frameworks, and developers' increasing focus on embodied carbon reduction in construction projects. Manufacturers are investing in advanced technologies and processes to minimize their environmental footprint, such as utilizing recycled materials and cleaner energy sources. For instance, according to Fastmarkets, November 2025, in "UAE demand for low-carbon steel rises as regulators tighten standards: AGSI", Arabian Gulf Steel Industries (AGSI) has achieved an emissions profile of 0.14 tonnes of CO2 equivalent per tonne of crude steel, which is approximately 95% lower than traditional blast furnace-based steelmaking. This trend is fostering innovation in production methods and creating a competitive advantage for companies that can supply environmentally responsible rebar solutions.

Rising Demand for High-Strength, Corrosion-Resistant Rebar

Concurrently, the rising demand for high-strength and corrosion-resistant rebar is significantly influencing market dynamics, reflecting the UAE's challenging environmental conditions and the increasing complexity of its infrastructure and high-rise developments. Projects in coastal areas and those designed for longevity necessitate materials that can withstand harsh elements and provide superior structural integrity. This demand pushes manufacturers to develop specialized rebar grades that offer enhanced durability and reduced maintenance requirements over the lifecycle of a structure. According to Forbes Middle East, May 2026, EMSTEEL's ES600 high-performance rebar is designed to reduce steel consumption in major projects by up to 24%, highlighting the efficiency and material optimization benefits of advanced rebar products.

Segmental Insights

Rising Epoxy-Coated Rebar Demand in the UAE Driven by Harsh Environment and Regulatory Standards

The Epoxy-Coated Rebar segment is experiencing rapid growth within the UAE Rebar Steel Market, primarily driven by the nation's challenging environmental conditions and extensive infrastructure development. The UAE's high humidity, coastal proximity, and saline groundwater create an aggressive environment that significantly accelerates corrosion in conventional steel reinforcement, necessitating superior protection for long-term structural integrity. Consequently, project owners and regulatory guidance, such as adherence to specifications like ASTM A775, increasingly prioritize epoxy-coated rebar for its robust corrosion resistance, ensuring enhanced durability and reduced maintenance across critical infrastructure and mega-construction projects.

Regional Insights

Dubai: Primary Driver of UAE Rebar Steel Demand

Dubai consistently leads the UAE Rebar Steel Market due to its robust position as the nation's primary economic and commercial center. This dominance is driven by aggressive urbanization, sustained population growth, and substantial government-led investment in extensive infrastructure development. The emirate's strategic urban master plans and ongoing commitment to diversifying its economy fuel a continuous pipeline of large-scale construction projects across residential, commercial, and transportation sectors. This environment generates significant demand for rebar steel, essential for supporting the structural integrity of numerous high-rise buildings and expansive urban developments.

Recent Developments

-

In November 2025, Bekaert and EMSTEEL Building Materials PJSC entered into a partnership aimed at advancing the production and market entry of high-end, sustainable products and solutions utilizing UAE-made steel. This collaboration sought to expand EMSTEEL's wire rod portfolio and explore downstream investments, enabling the manufacture of higher value-adding products, including steel fiber reinforced concrete solutions. The agreement highlighted efforts to promote sustainable construction materials across GCC markets. This initiative reinforced the commitment of companies within the UAE rebar steel market to innovation and environmental responsibility through strategic technical collaboration.

-

In May 2025, Aldar, a prominent developer, collaborated with EMSTEEL Group to introduce hydrogen-based steel rebar into construction projects within the Middle East and North Africa region. This partnership marked a significant advancement in decarbonizing the built environment, with the innovative rebar being utilized for Abu Dhabi's inaugural net-zero carbon mosque. The project aimed to achieve LEED Zero Carbon certification, demonstrating a commitment to reduced emissions in both production and energy consumption through low-carbon materials. This initiative by EMSTEEL supported the region's transition towards sustainable construction practices within the UAE rebar steel market.

-

In December 2024, Modon Real Estate, a master developer, formed a strategic alliance with EMSTEEL Group, the UAE's largest steel and building materials manufacturer, to integrate low-carbon steel into its development projects. This collaboration positioned Modon as the first real estate developer in the UAE to adopt such materials. The initiative underscored both companies' roles in driving the construction industry's transition towards sustainability and decarbonization, aligning with the UAE's Net-Zero 2050 Strategy. The green steel was sourced from the EMSTEEL Group and Masdar's pioneering green hydrogen pilot project, establishing a new standard for responsible construction within the UAE rebar steel sector.

-

In January 2024, Conares, a major UAE steel manufacturer, announced its commitment to achieving net-zero carbon emissions by 2050. This strategic pledge aligned with the UAE's broader environmental objectives and positioned the company as a leader in sustainable manufacturing within the rebar steel market. A key part of this sustainability endeavor involved a strategic collaboration between Conares and DP World, leveraging its trade and logistics capabilities. This partnership aimed to bolster Conares' efforts in green steel production, with the company setting a target to achieve 50 percent of its net-zero goals by 2040 and contributing to the UAE's carbon emission reduction targets.

Key Market Players

- Emirates Steel

- Al Ghurair Iron & Steel

- Qatar Steel

- ArcelorMittal

- Hadeed Emirates

- Conares Metal Supply

- JSW Steel

- Tata Steel UAE

- Al Futtaim Group

- Saudi Steel

|

By Type

|

By End Use

|

By Process

|

By Finishing Type

|

By Region

|

|

|

- Residential

- Commercial

- Industrial

- Public

|

- Basic Oxygen Steelmaking

- Electric Arc Furnace

|

- Epoxy-Coated Rebar

- Carbon Steel rebar

- Others

|

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

|

Report Scope:

In this report, the UAE Rebar Steel Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

UAE Rebar Steel Market, By Type:

-

UAE Rebar Steel Market, By End Use:

-

Residential

-

Commercial

-

Industrial

-

Public

-

UAE Rebar Steel Market, By Process:

-

Basic Oxygen Steelmaking

-

Electric Arc Furnace

-

UAE Rebar Steel Market, By Finishing Type:

-

Epoxy-Coated Rebar

-

Carbon Steel rebar

-

Others

-

UAE Rebar Steel Market, By Region:

-

Dubai

-

Abu Dhabi

-

Sharjah

-

Rest of UAE

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the UAE Rebar Steel Market.

Available Customizations:

UAE Rebar Steel Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

UAE Rebar Steel Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com