|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 3.03 Billion

|

|

CAGR (2026-2031)

|

6.29%

|

|

Fastest Growing Segment

|

Pickup Truck

|

|

Largest Market

|

Dubai

|

|

Market Size (2031)

|

USD 4.37 Billion

|

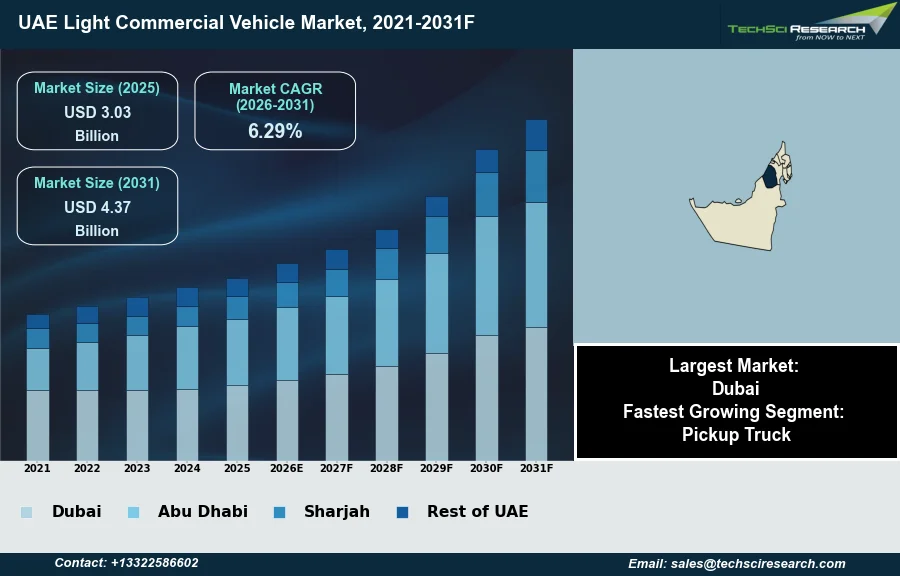

Market Overview

The UAE Light Commercial Vehicle Market will grow from USD 3.03 Billion in 2025 to USD 4.37 Billion by 2031 at a 6.29% CAGR. Light Commercial Vehicles (LCVs) are commercial transport vehicles with a gross vehicle weight typically up to 3.5 or 4.5 metric tons, designed for the efficient movement of goods or specialized equipment and commonly including pickup trucks, vans, and light-duty trucks. The UAE LCV market's expansion is primarily driven by substantial government investments in infrastructure and logistics projects, alongside the growth of key sectors such as construction, e-commerce, and diversified industries. These factors necessitate robust transportation solutions for materials and last-mile delivery services. According to the International Organization of Motor Vehicle Manufacturers, in 2024, new commercial vehicle sales in the UAE reached 37,403 units, demonstrating sustained market activity.

However, the market faces a significant challenge from increasingly stringent environmental regulations, which necessitate considerable fleet upgrades to meet evolving emission standards. This requirement often involves substantial capital expenditure for businesses, potentially impeding market expansion as operators weigh the costs of compliance against operational profitability.

Key Market Drivers

Infrastructure Growth Drives LCV Demand

Robust infrastructure development and significant construction projects are primary drivers of the UAE Light Commercial Vehicle Market. These initiatives demand extensive logistical support for transporting materials, equipment, and personnel across various sites, directly stimulating the need for LCVs like pickup trucks and vans. For instance, according to Gulf Construction, in December 2024, the 'Tasreef' initiative, aimed at developing Dubai's rainwater drainage network, was announced with a cost of AED30 billion, showcasing substantial ongoing investment in critical urban infrastructure. Such large-scale undertakings create sustained demand for versatile and durable light commercial vehicles.

E-commerce Expansion and Economic Momentum

Furthermore, the surging e-commerce sector and the escalating demand for last-mile delivery services are profoundly influencing the market. The expansion of online retail necessitates efficient and swift delivery networks, with LCVs forming the backbone of these operations for urban and suburban distribution. According to Stratrich Consulting, in 2023, Amazon opened a new fulfillment center in the UAE, increasing its total storage capacity in the country by 70%, underscoring the rapid growth in e-commerce infrastructure. This growth, coupled with the overall economic activity, is anticipated to maintain strong demand for light commercial vehicles. Broader economic indicators also highlight the favorable environment for LCVs, as according to Knight Frank, in 2024, the UAE's construction output reached a record $107.2 billion, demonstrating robust sector performance that underpins a wide range of commercial vehicle needs.

Download Free Sample Report

Key Market Challenges

EURO 6B Compliance Drives Fleet Upgrades and Capex

The UAE Light Commercial Vehicle market faces a significant challenge from increasingly stringent environmental regulations. These mandates, particularly the requirement for new imported light and heavy vehicles to comply with EURO 6B standards starting in January 2026, necessitate considerable fleet upgrades to meet evolving emission benchmarks. This imposes substantial capital expenditure on businesses as they invest in newer, compliant vehicles or consider upgrading existing fleets, directly impacting their operational profitability.

Investment Reassessment Delays Modernization and Market Growth

Operators are compelled to reassess their investment strategies, often delaying fleet modernization and reducing the acquisition of new light commercial vehicles. This re-evaluation of capital allocation directly impedes market expansion as businesses prioritize regulatory adherence and the associated compliance costs over immediate fleet growth and replacement cycles. This shift in investment priorities poses a direct constraint on the market's natural expansion.

Key Market Trends

Electrification of LCVs in the UAE Drives Adoption

Electrification of Light Commercial Fleets represents a pivotal transformation, driven by a global push for sustainability and stricter environmental regulations in the UAE. This trend mandates fleet operators to transition towards electric LCVs to reduce carbon footprints and achieve long-term operational cost savings through lower fuel and maintenance expenditures. For instance, according to LogisticsGulf, in January 2025, Aramex, a prominent logistics provider, launched its first commercial fleet of electric trucks in the UAE, signaling its ambitious goal to convert 98% of its entire fleet to electric by 2030, underscoring the tangible shift towards cleaner transport solutions. This commitment by major players is fostering an ecosystem supportive of electric vehicle adoption, influencing procurement decisions across the market.

Telematics and Connectivity Transform LCV Fleet Management

The integration of Advanced Telematics and Connectivity Solutions is fundamentally reshaping LCV fleet management. These systems provide real-time data insights, enabling optimized route planning, improved driver behavior monitoring, and predictive maintenance. Such technological adoption leads to enhanced operational efficiency, heightened safety standards, and better resource allocation across the supply chain. Demonstrating this impact, according to the Government of Dubai Media Office, in October 2025, the Dubai Roads and Transport Authority's Smart Vehicle Network, which leverages cooperative intelligent transport systems to manage traffic, successfully reduced delays by 25% and cut operational costs by up to 30%. This highlights the measurable benefits derived from advanced connectivity for commercial fleet operations in the region.

Segmental Insights

Pickup Trucks: Fastest-Growing Segment Fueled by Infrastructure, Construction, and E-commerce

The UAE Light Commercial Vehicle market is experiencing significant growth, with pickup trucks emerging as the fastest-growing segment. This rapid expansion is primarily driven by the nation's substantial investment in infrastructure development and ongoing construction projects, which necessitate robust vehicles for material transport and operational support. Furthermore, the booming e-commerce sector and the increasing demand for last-mile delivery services across the Emirates are fueling the adoption of pickup trucks due to their adaptability, efficiency, and cost-effectiveness for businesses. Their inherent versatility and utility for various commercial applications further solidify their position as a key growth driver in the market.

Regional Insights

Dubai Drives the UAE Light Commercial Vehicle Market.

Dubai leads the UAE Light Commercial Vehicle market, primarily due to its robust commercial activity and strategic role as a pivotal logistics and financial hub. The emirate's dense urban infrastructure, coupled with its advanced port facilities and extensive free zones, generates substantial demand for light commercial vehicles to support goods distribution, courier services, and vital last-mile delivery operations within its burgeoning e-commerce sector. Significant government investment in sophisticated road networks and ongoing infrastructure development further facilitates efficient LCV deployment. Moreover, sustained expansion across the retail, hospitality, and construction industries continually fuels the requirement for these vehicles to meet diverse commercial and operational needs throughout the region.

Recent Developments

-

In October 2025, a significant milestone in smart mobility was achieved with the launch of the UAE's first commercial fleet of autonomous electric trucks. This initiative resulted from a collaboration between Evocargo, a developer of autonomous transport systems, and RAK Ceramics, a global ceramics manufacturer. The newly deployed Evocargo N1 electric trucks now operate daily within the Al Jazeera Al Hamra industrial zone, transporting ceramics and sanitary products. These unmanned vehicles, equipped with advanced autopilot systems, exemplify breakthrough research and innovation in sustainable commercial logistics within the UAE.

-

In April 2025, MAN Truck & Bus officially launched its MAN TGE van in the United Arab Emirates, marking the brand's international expansion of its van business beyond Europe. The launch event in Dubai, held in cooperation with local importer Darwish bin Ahmed & Sons (DBA), introduced the MAN TGE in station wagon and minibus variants, alongside ambulance conversions by local bodybuilders. This strategic entry aims to cater to the growing demand for versatile light commercial vehicles from various sectors, including shuttle services, mobile technicians, and specialized transport in the UAE market.

-

In March 2025, Al-Futtaim Industrial Equipment collaborated with BYD Commercial Vehicles to introduce BYD's new energy commercial vehicle lineup in the United Arab Emirates. The official launch in Dubai featured four fully electric models, including light and medium-duty trucks (ETM6, T5, ETH8) and the B12 electric bus, all equipped with advanced Blade Battery technology. These vehicles offer enhanced safety, rapid charging capabilities, and extended range, providing zero-emission alternatives for urban logistics, freight, and public transport sectors in the UAE and supporting the nation's transition towards sustainable transportation.

-

In May 2024, Al Habtoor Motors, the authorized distributor of JAC Motors in the UAE, unveiled a new fleet of JAC commercial vehicles, enhancing the country's light commercial vehicle segment. The launch event in Dubai showcased an expanded range of models, including the Sunray and M4 minibuses, cargo vans, and light trucks. These vehicles were specifically designed for the UAE market, featuring robust structures, advanced engines, and improved fuel efficiency to handle various applications and demanding conditions. This introduction aimed to offer greater reliability, versatility, and innovation for businesses in logistics, construction, and transportation sectors across the UAE.

Key Market Players

- Toyota UAE

- Ford Middle East

- Hyundai UAE

- Nissan Middle East

- Volkswagen UAE

- Mercedes-Benz Vans UAE

- Isuzu UAE

- Mitsubishi Motors UAE

- Renault UAE

- Peugeot UAE

|

By Vehicle Type

|

By Fuel Type

|

By End Use

|

By Region

|

- Pickup Truck

- Van & Light Bus

|

|

- Individuals Vs Fleet Owner

|

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

|

Report Scope:

In this report, the UAE Light Commercial Vehicle Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

UAE Light Commercial Vehicle Market, By Vehicle Type:

-

Pickup Truck

-

Van & Light Bus

-

UAE Light Commercial Vehicle Market, By Fuel Type:

-

UAE Light Commercial Vehicle Market, By End Use:

-

Individuals Vs Fleet Owner

-

UAE Light Commercial Vehicle Market, By Region:

-

Dubai

-

Abu Dhabi

-

Sharjah

-

Rest of UAE

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the UAE Light Commercial Vehicle Market.

Available Customizations:

UAE Light Commercial Vehicle Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

UAE Light Commercial Vehicle Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com