|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 3.89 Billion

|

|

CAGR (2026-2031)

|

15.17%

|

|

Fastest Growing Segment

|

Payment

|

|

Largest Market

|

Dubai

|

|

Market Size (2031)

|

USD 9.08 Billion

|

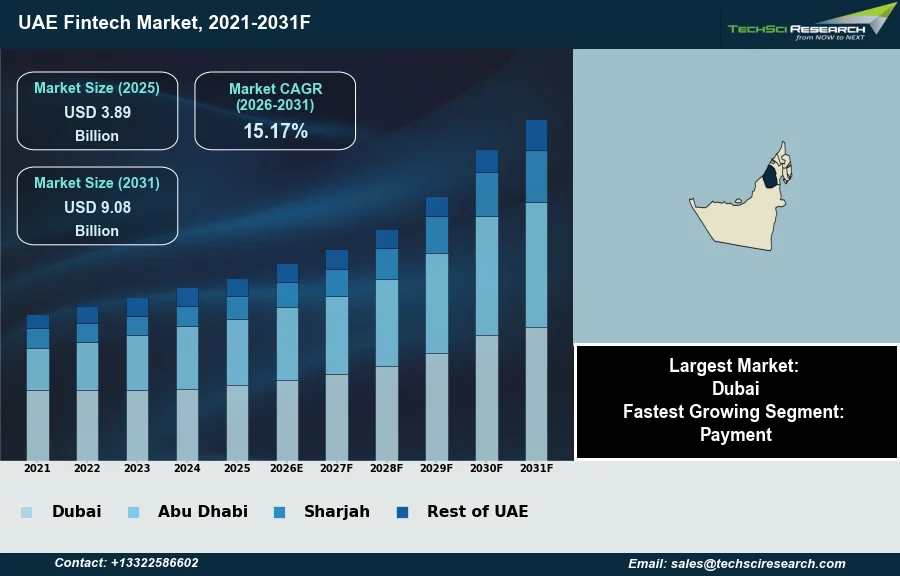

Market Overview

The UAE Fintech Market will grow from USD 3.89 Billion in 2025 to USD 9.08 Billion by 2031 at a 15.17% CAGR. Financial technology, or Fintech, in the UAE integrates technology into financial services, enhancing delivery and accessibility across digital payments, lending, and investment platforms. Key market growth drivers include proactive government initiatives via supportive regulatory frameworks and innovation hubs, along with a robust digital infrastructure enabling high smartphone penetration. Consumer adoption of digital financial solutions further propels expansion. According to the Dubai International Financial Centre (DIFC) in February 2026, FinTech and AI organizations within DIFC reached 1,677 in 2025, marking a 35% rise.

This robust development is also evident in regulatory advancements. According to the UAE Central Bank's annual report for 2025, the number of licensed fintechs doubled from 18 in 2024 to 36 in 2025. A significant challenge impeding market expansion, however, is the complexity derived from a fragmented regulatory landscape, where distinct authorities oversee various financial service segments.

Key Market Drivers

Government-Led Digitization and Cashless Agenda

Government-Led Digital Transformation Initiatives significantly propel the UAE Fintech Market by establishing a supportive national vision and infrastructure for digital finance. The UAE government actively implements strategies to digitize various sectors, fostering an environment where fintech innovations can thrive. This proactive approach includes initiatives aimed at creating a cashless economy. For instance, according to MEXC News, May 2026, in "Dubai Pushes Toward a Cashless Future as Digital Payments Near 90% of Transactions by 2026," authorities aim for nearly 90 percent of all transactions across public and private sectors in Dubai to become fully digital by the end of 2026. Such governmental mandates and strategic visions directly stimulate demand for and adoption of digital financial services, driving innovation in payments, lending, and investment platforms.

Venture Capital Driving UAE Fintech Growth

The robust investment and venture capital landscape in the UAE is another critical driver, providing essential funding that fuels the growth and expansion of fintech companies. This strong financial backing enables startups to develop advanced technologies, scale operations, and enhance their offerings, thereby enriching the overall fintech ecosystem. For example, according to INTLBM, March 2026, in "The UAE's Venture Capital & Angel Investor Ecosystem," the UAE's venture capital and angel investment market is estimated at $1.5–$2 billion annually by 2026, positioning it as the largest in the MENA region. This substantial capital inflow, coupled with strategic global hub positioning, attracts both local and international investors, creating a dynamic environment for fintech innovation. Overall, the market benefits from high digital adoption, with around 89% of UAE consumers using digital-first bank accounts.

Download Free Sample Report

Key Market Challenges

Fragmented Regulation Elevates Compliance Costs and Delays Market Entry

A significant challenge impeding expansion in the UAE Fintech market is the complexity stemming from a fragmented regulatory landscape, where distinct authorities oversee various financial service segments. This creates a challenging environment for fintech companies, particularly those aiming to offer innovative solutions that span multiple areas such as payments, lending, or investment. Such fragmentation necessitates navigating diverse licensing requirements and compliance frameworks from separate regulators, leading to increased operational costs and prolonged time to market.

Regulatory Complexity Impedes Growth and Scaling

This complex environment can slow the growth and scalability of emerging fintech ventures. For example, according to the Dubai Chamber of Digital Economy, in 2025, fintech companies comprised 12 percent of the 1,690 digital startups supported in Dubai. While this demonstrates a robust entrepreneurial spirit, the need for fintechs to understand and adhere to differing rules across various jurisdictions or regulatory bodies within the UAE directly impedes their ability to efficiently scale their offerings nationally and attract further investment with clear regulatory pathways. This friction can divert resources from innovation and product development towards compliance overheads, thereby hampering overall market development.

Key Market Trends

Open Banking and API Ecosystems Drive UAE Fintech Innovation

The shift toward Open Banking and API ecosystems profoundly influences the UAE Fintech Market, fostering greater interoperability and innovation across financial services. This trend facilitates secure data sharing between institutions and third-party providers, enabling integrated, personalized customer experiences. Consumers gain more control over their financial data, driving the creation of new products, from advanced personal finance management tools to streamlined payment solutions. According to the Central Bank of the UAE's Annual Report for 2025, the Open Finance initiative, Al Tareq, launched in 2025, with two banks and two Third-Party Providers meeting regulatory requirements to offer services via Open Banking APIs. This development underpins a collaborative, competitive financial ecosystem, promoting efficiency and service diversification.

CBDC Advancement and Stablecoin Regulation in UAE Fintech

The integration of digital currencies and stablecoin frameworks is another pivotal trend reshaping the UAE Fintech landscape, particularly in cross-border payments and digital asset innovation. The Central Bank of the UAE is actively advancing a Central Bank Digital Currency, the Digital Dirham, alongside robust regulatory frameworks for stablecoins and virtual assets. This initiative aims to enhance payment efficiency, reduce transaction costs, and strengthen the UAE's global digital finance hub standing. For instance, according to the MENA Fintech Association, April 2026, Project mBridge, involving the UAE Central Bank, processed 4,047 transactions totaling $55.49 billion as of November 2025, utilizing distributed ledger technology for CBDC-based transfers. This progress demonstrates a tangible move towards leveraging tokenized assets for faster, more secure, and transparent financial transactions.

Segmental Insights

Rapid Growth Fueled by Digital Payments, E-Commerce, and Regulatory Support

The Payment segment is the fastest-growing area within the UAE Fintech Market, primarily driven by the increasing adoption of digital payment solutions and mobile wallets among a technologically adept population. This rapid expansion is also significantly propelled by the thriving e-commerce sector and a strong government push towards a cashless economy. Initiatives such as the Central Bank of the UAE's Financial Infrastructure Transformation Programme are actively fostering payment innovation by establishing advanced infrastructure, including instant payment platforms and a domestic card scheme. Additionally, the supportive regulatory environments provided by entities like the Central Bank of the UAE, Abu Dhabi Global Market, and Dubai International Financial Centre encourage the development and widespread acceptance of secure and efficient payment technologies to meet evolving consumer and business demands.

Regional Insights

Dubai's Fintech Leadership: Regulation and Ecosystem

Dubai leads the UAE Fintech market due to its strategic initiatives and a supportive regulatory environment. The Dubai International Financial Centre (DIFC), a prominent financial free zone, serves as a significant hub, offering a robust ecosystem for fintech innovation. The Dubai Financial Services Authority (DFSA), the independent regulator within DIFC, facilitates growth through programs like the Innovation Testing Licence, which provides a controlled environment for firms to develop new financial products and services. Furthermore, the establishment of the Virtual Assets Regulatory Authority (VARA) by the Dubai government has specifically attracted virtual asset service providers, reinforcing the emirate's position by providing clear regulatory frameworks. These concerted efforts, coupled with investments in technology infrastructure, are pivotal to Dubai's dominance.

Recent Developments

-

In July 2025, United Arab Bank (UAB) entered a strategic partnership with Lune, a UAE-based FinTech company specializing in AI-driven transaction enrichment and financial data analytics. This collaboration was intended to significantly enhance UAB's upcoming mobile banking experience within the UAE. By leveraging Lune's technology, UAB aimed to transform raw transaction data into meaningful financial insights through a user-friendly interface. This move positioned the bank to deliver smarter, data-driven, and hyper-personalized customer journeys, fostering improved financial transparency and informed decision-making for its clients.

-

In December 2024, First Abu Dhabi Bank (FAB) selected Broadridge Financial Solutions, a global FinTech leader, to develop its global agency securities finance business. This partnership represented a significant step towards expanding securities lending activities within the UAE and the broader Middle East. By utilizing Broadridge's advanced Securities Finance and Collateral Management solution, FAB aimed to enhance its coverage of global fixed income and equities markets. The collaboration was intended to meet the growing regional demand for securities lending and borrowing, aligning with local regulatory requirements and international best practices.

-

In April 2024, First Abu Dhabi Bank (FAB) and Microsoft announced a strategic business partnership in the UAE to develop new AI-based banking capabilities. This collaboration aimed to launch an 'AI Innovation Hub' for financial services, focusing on innovation, sustainability, and customer experience. The initiative positioned FAB to leverage Microsoft's Azure AI services, including generative AI, to automate and revolutionize operations across the FAB Group. Potential areas of enhancement included Banking-as-a-Service and Risk-as-Service, covering digital services, lending, and payments within various banking segments.

-

In the second quarter of 2024, Al Ansari Digital Pay, a subsidiary of Al Ansari Financial Services, prepared to launch a new digital wallet in the UAE. The company had received initial approval from the UAE Central Bank for a store value facilities and retail payment service provider license. This new product was designed to serve unbanked populations by offering services such as salary receipts, domestic and international money remittances, and bill settlements. The digital wallet aimed to provide a comprehensive and seamless peer-to-peer transfer solution, contributing to the nation's digital payment ecosystem.

Key Market Players

- Bayzat

- Tabby

- Tamara

- PayTabs

- Telr

- HyperPay

- Mamo Pay

- Salla

- Zand Bank

- Rain

|

By Technology

|

By Service

|

By Application

|

By Region

|

- API

- AI

- Blockchain

- Distributed Computing

- Others

|

- Payment

- Fund Transfer

- Personal Finance

- Loans

- Insurance

- Others

|

- Banking

- Insurance

- Securities

- Others

|

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

|

Report Scope:

In this report, the UAE Fintech Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

UAE Fintech Market, By Technology:

-

API

-

AI

-

Blockchain

-

Distributed Computing

-

Others

-

UAE Fintech Market, By Service:

-

Payment

-

Fund Transfer

-

Personal Finance

-

Loans

-

Insurance

-

Others

-

UAE Fintech Market, By Application:

-

Banking

-

Insurance

-

Securities

-

Others

-

UAE Fintech Market, By Region:

-

Dubai

-

Abu Dhabi

-

Sharjah

-

Rest of UAE

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the UAE Fintech Market.

Available Customizations:

UAE Fintech Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

UAE Fintech Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com