|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 6.48 Billion

|

|

CAGR (2026-2031)

|

13.98%

|

|

Fastest Growing Segment

|

Carbon Steel Rebar

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 14.21 Billion

|

Market Overview

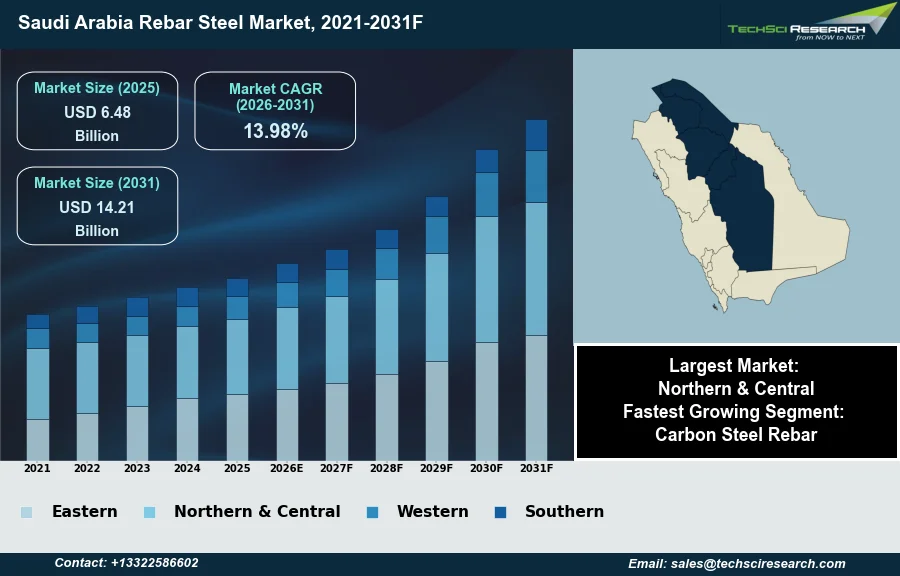

The Saudi Arabia Rebar Steel Market will grow from USD 6.48 Billion in 2025 to USD 14.21 Billion by 2031 at a 13.98% CAGR. Rebar steel, or reinforcing bar, is a critical component in reinforced concrete and masonry structures, providing essential tensile strength and enhancing overall structural integrity. The Saudi Arabia rebar steel market is significantly propelled by robust government-led initiatives, notably the ambitious Vision 2030, which encompasses extensive mega-projects such as NEOM and the expansion of national infrastructure. Furthermore, rapid urbanization and sustained population growth are continuously stimulating demand for both residential and commercial construction across the Kingdom.

These growth drivers are evident in market metrics. According to the Arab Iron and Steel Union, in January 2025, the average price per ton of rebar in Saudi Arabia reached SAR 2,962, representing a 2.9% increase from SAR 2,878 in January 2024. Despite this positive momentum, a significant impediment to market expansion remains the volatility of raw material prices, including iron ore and scrap metal, which can impact production costs and overall profitability.

Key Market Drivers

Vision 2030 and mega-projects drive rebar steel demand

Saudi Vision 2030 and its accompanying mega-project development represent a primary catalyst for the Saudi Arabia rebar steel market. These governmental initiatives drive immense construction activity across the Kingdom, encompassing futuristic cities, extensive infrastructure networks, and diverse urban developments. The sheer scale and ambitious timelines of projects such as NEOM, The Red Sea Project, and King Salman International Airport necessitate substantial volumes of rebar steel for foundational and structural reinforcement. This sustained investment in national transformation creates a robust and consistent demand for reinforcing materials, as evidenced by Saudi Arabia's total contractor awards value estimated at nearly US$66.4 billion in 2025, according to Ventures Onsite in December 2025.

Urbanization and population growth underpin rebar demand

Complementing this, rapid urbanization and sustained population growth are fundamental drivers of rebar demand. As urban centers expand to accommodate a growing populace, there is a continuous need for new residential, commercial, and social infrastructure. This demographic expansion directly fuels the construction sector, requiring significant quantities of rebar for various building types. For example, according to Kallanish, in October 2025, Saudi steel demand was projected to grow 9-10% year-on-year in 2026, significantly supported by a young generation with a 4% population growth. This underlying demographic impetus contributes to the overall market strength, with Saudi Arabia's steel output rising 12.3% to 10.784 million tons in 2025, as reported by the Arab Iron and Steel Union in February 2026.

Download Free Sample Report

Key Market Challenges

Volatility in Raw Material Prices Impedes Growth and Planning

The volatility of raw material prices, specifically iron ore and scrap metal, presents a significant impediment to the growth of the Saudi Arabia rebar steel market. Fluctuations in these essential input costs directly impact the production expenses for domestic rebar manufacturers. This unpredictability hinders effective long-term planning and consistent pricing strategies, leading to uncertainty in operational budgets.

Profit Margin Pressure and Investment Constraints from Material Cost Volatility

Consequently, manufacturers face compressed profit margins, which can discourage investment in capacity expansion or technological upgrades necessary to meet the increasing demand from large-scale projects like Vision 2030 and rapid urbanization. According to Fastmarkets, the steel scrap HMS 1&2 index, domestic composite, delivered Saudi Arabia, reached 1,479.05 riyals per tonne on April 7, 2026, increasing from 1,439.81 riyals per tonne the week prior. Such rapid shifts in raw material costs necessitate frequent adjustments in production strategies and pricing, contributing to market instability. This constant adaptation consumes resources and diverts focus from strategic growth initiatives, thereby directly constraining the overall expansion of the rebar steel market within the Kingdom.

Key Market Trends

Localization strategy to bolster domestic steel supply and value chains

A strategic push for domestic steel manufacturing localization significantly shapes the Saudi Arabia rebar steel market by fostering self-sufficiency and strengthening local supply chains. This initiative aims to reduce reliance on imports and integrate the steel sector more deeply into the national economy. A key aspect of this drive is encouraging major national entities to source materials locally, thereby generating substantial opportunities for domestic producers. According to Metal Expert, October 2025, the Saudi Minister of Industry and Mineral Resources highlighted that six leading state-owned companies collectively spend nearly SAR 500 billion ($133 billion) annually, creating extensive opportunities for the development of domestic value chains, including steel. This governmental emphasis provides a stable framework for investments in local production capabilities, ensuring consistent supply for the Kingdom's extensive construction projects.

Technology-driven modernization of rebar production

Concurrently, the rising adoption of advanced steel manufacturing technologies is transforming production processes within the Saudi rebar steel market. This trend is driven by the need to enhance efficiency, improve product quality, and meet stringent performance requirements for modern infrastructure. Manufacturers are increasingly investing in automation, digitalization, and innovative production methods to optimize operations. For instance, according to Mining Beacon, May 2025, Saudi Iron & Steel Company (Hadeed) outlined plans for investments totaling up to US$6 billion by 2030, aiming to double its steel production to approximately 10 million tonnes per annum, indicating significant technology modernization efforts. These technological advancements enable higher precision, reduced waste, and the production of more sophisticated rebar, which is crucial for the Kingdom's ambitious and complex construction undertakings.

Segmental Insights

Carbon Steel Rebar Growth Driven by Vision 2030 Infrastructure Initiatives

The Saudi Arabia Rebar Steel Market is experiencing robust expansion, with Carbon Steel Rebar identified as the fastest-growing segment. This rapid growth is primarily driven by the Kingdom's ambitious Vision 2030 initiatives, which entail massive investments in diverse construction and infrastructure projects. Extensive development across smart cities, transportation networks, tourism destinations, and industrial facilities, including iconic undertakings such as NEOM, the Red Sea Project, and various housing programs, generates substantial demand for reinforcement steel. Carbon steel rebar is fundamental to these large-scale structures due to its inherent strength and suitability for reinforced concrete applications, consistently meeting the stringent quality and performance requirements mandated by the Saudi Standards, Metrology and Quality Organization (SASO).

Regional Insights

Riyadh-Driven Growth in the Northern & Central Rebar Market Under Vision 2030

The Northern & Central region stands as the leading force in the Saudi Arabia Rebar Steel Market, primarily driven by the ambitious urban and infrastructure development agenda under Saudi Vision 2030. This dominance is anchored by Riyadh, which serves as a pivotal economic and administrative hub, concentrating a significant volume of large-scale construction projects. Key initiatives such as the Riyadh Metro, Diriyah Gate, and King Salman Park, alongside entertainment mega-projects like Qiddiya City, generate immense demand for reinforcing steel. Furthermore, Riyadh's position as an industrial center, housing numerous steel processing and construction material enterprises, ensures a consistent supply chain. The Ministry of Municipalities and Housing's ongoing efforts and local authorities' enforcement of rigorous building codes also contribute to sustained demand for high-quality rebar in the region's transformative developments.

Recent Developments

-

In January 2025, Saudi Iron & Steel Company (Hadeed) announced substantial investments and acquisitions totaling approximately SAR 25 billion (USD 6.67 billion) to significantly expand its annual steel production capacity to 10 million tonnes. This strategic growth initiative is a core component of Saudi Arabia's Vision 2030, aimed at bolstering the country's industrial base and supporting its extensive infrastructure projects. Furthermore, Hadeed formalized a Memorandum of Understanding with Baosteel, a prominent Chinese steel manufacturer, establishing a strategic cooperation to address the escalating demand for steel, including rebar, within the rapidly developing Saudi Arabian market.

-

In December 2024, NEOM Investment Fund and Samsung C&T Corporation entered into a joint venture, committing an initial investment exceeding SAR 1.3 billion ($345 million) towards advancements in construction robotics. This partnership is specifically focused on automating rebar cage assembly using sophisticated robotic welding and tying techniques, enabling the efficient fabrication of large, pre-manufactured reinforcement cages. This breakthrough in construction automation is anticipated to significantly reduce manual labor by up to 80% and cut rebar assembly costs by as much as 40%, enhancing efficiency and safety within Saudi Arabia's rebar steel market.

-

In January 2024, a Memorandum of Understanding was signed between the Royal Commission for Jubail and Yanbu in Saudi Arabia and the Brazilian mining major, Vale Company. This collaboration focuses on developing an iron ore briquettes project, which is a key step towards decarbonizing the steelmaking industry in the Kingdom. The planned Mega Hub project in Ras Al-Khair Industrial City aims to produce high-quality agglomerated products, designed to reduce carbon dioxide emissions by 60%, thereby fostering the establishment of a green steel industry vital for the Saudi Arabia rebar steel market's sustainable future.

-

In 2024, Essar Group began its investment of approximately $4 billion into establishing a low-carbon steel plant in Ras Al-Khair, Saudi Arabia. This new facility, which is projected to have an annual production capacity of 4 million tonnes, will utilize advanced gas-based direct reduced iron and electric arc furnace technologies. This initiative represents a significant step towards developing sustainable steel production capabilities within the Kingdom, intending to satisfy the growing domestic demand for various steel products, including rebar, crucial for Saudi Arabia's ongoing construction and infrastructure development.

Key Market Players

- Saudi Iron & Steel Company (HADEED)

- Al Ittefaq Steel Products Co.

- Rajhi Steel Industries Company Ltd.

- Watania Steel Factory Corporation

- Al Yamamah Company for Reinforcing Steel Bars

- Saudi National Steel Factory

- Baghlaf Steel

- Mass Steel

- Madar Building Materials, LLC

- Bahra Steel Co.

|

By Type

|

By End Use

|

By Process

|

By Finishing Type

|

By Region

|

|

|

- Residential Sector

- Commercial Sector

- Industrial Sector

- Public Sector

|

- Basic Oxygen Steelmaking

- Electric Arc Furnace

|

- Epoxy-Coated Rebar

- Carbon Steel Rebar

- Others

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Rebar Steel Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Rebar Steel Market, By Type:

-

Saudi Arabia Rebar Steel Market, By End Use:

-

Residential Sector

-

Commercial Sector

-

Industrial Sector

-

Public Sector

-

Saudi Arabia Rebar Steel Market, By Process:

-

Basic Oxygen Steelmaking

-

Electric Arc Furnace

-

Saudi Arabia Rebar Steel Market, By Finishing Type:

-

Epoxy-Coated Rebar

-

Carbon Steel Rebar

-

Others

-

Saudi Arabia Rebar Steel Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Rebar Steel Market.

Available Customizations:

Saudi Arabia Rebar Steel Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Rebar Steel Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com