|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

Market Size (2025)

|

USD 567.88 Million

|

|

CAGR (2026-2031)

|

4.81%

|

|

Fastest Growing Segment

|

Heavy Duty

|

|

Largest Market

|

Eastern

|

|

Market Size (2031)

|

USD 752.79 Million

|

Market Overview

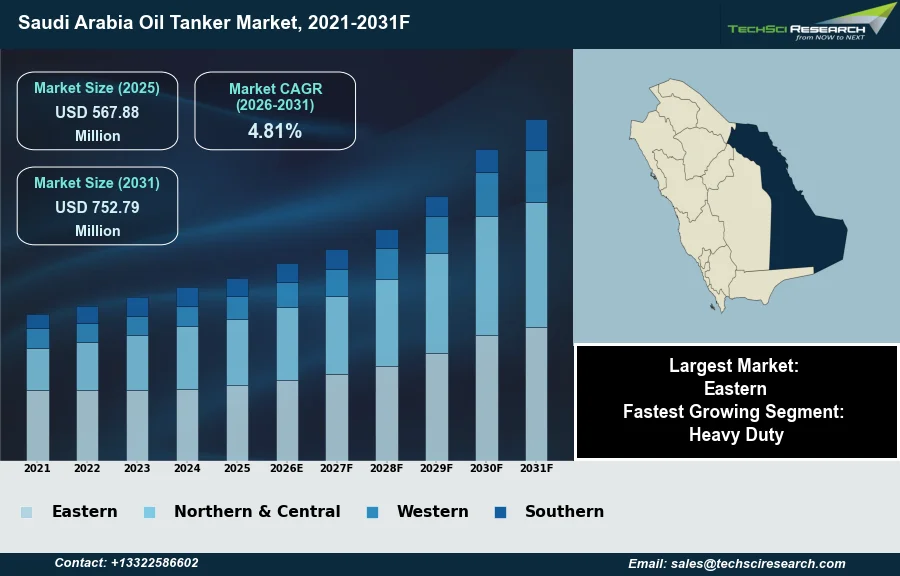

The Saudi Arabia Oil Tanker Market will grow from USD 567.88 Million in 2025 to USD 752.79 Million by 2031 at a 4.81% CAGR. Oil tankers are specialized maritime vessels primarily constructed for the bulk transport of crude oil or refined petroleum products. The Saudi Arabia oil tanker market's growth is predominantly supported by consistent global demand for oil, the Kingdom's expanding crude oil production capacity, and strategic investments in its port and refining infrastructure. These factors ensure a continuous need for efficient maritime transportation to meet international energy requirements. According to OPEC, Saudi Arabia's crude oil output averaged approximately 9.48 million barrels per day in 2025.

A significant challenge impeding market expansion is the inherent geopolitical instability in the region, which can severely disrupt critical shipping routes and impact export volumes. This instability introduces considerable risk and unpredictability for tanker operations. For instance, according to the Joint Organisations Data Initiative, Saudi Arabia's crude oil exports significantly declined to 4.974 million barrels per day in March 2026, reflecting the direct impact of regional conflicts on tanker market activity.

Key Market Drivers

Sustained Saudi crude output underpins tanker demand

Saudi Arabia's sustained crude oil production and export volumes form the fundamental bedrock of the Kingdom's oil tanker market. The consistent output ensures a steady demand for very large crude carriers and other tanker types to transport crude to international markets. Despite global market fluctuations, the Kingdom has maintained its role as a key supplier, necessitating reliable maritime logistics. This stability directly correlates with tanker demand, as a significant portion of the country's crude output is destined for export. For instance, according to House of Saud, May 2026, in 'Saudi Arabia Oil Industry: Production, Aramco & Future', Saudi crude oil production stood at approximately 10.1 million barrels per day as of early 2026, underscoring the substantial volumes that require seaborne transport.

Downstream capacity growth and product exports boost product-tanker demand

Concurrently, the expanding domestic refining capacity and subsequent refined product exports are another crucial driver, creating diversified demand for specialized product tankers. As Saudi Arabia invests in its downstream sector, more crude is processed domestically, leading to higher volumes of refined products such as gasoline, diesel, and jet fuel available for export. This strategic shift enhances value capture and necessitates a robust fleet capable of handling various petroleum products. The Kingdom's total refining capacity is estimated at approximately 6.6 million barrels per day as of 2026, according to House of Saud, May 2026, in 'Saudi Arabia Oil Industry: Production, Aramco & Future', highlighting the growing need for product tanker services. This robust activity within the broader maritime sector is reflected in the financial performance of key players; for example, according to Marine Link, in 2026, Saudi national shipping company Bahri posted a record full-year profit of $2.43 billion for 2025.

Download Free Sample Report

Key Market Challenges

Geopolitical Instability Impedes Saudi Oil Tanker Market Growth

Geopolitical instability in the region represents a significant impediment to the growth of the Saudi Arabia oil tanker market. Such instability directly threatens the predictability and safety of critical maritime shipping routes, which are essential for the unimpeded global distribution of Saudi crude oil and refined products. This environment of heightened risk and uncertainty discourages consistent tanker operations and can lead to re-routing, increased transit times, and elevated insurance premiums for vessels operating in the affected areas.

Export Decline from Regional Conflicts Dampens Tanker Demand

The direct impact of regional conflicts on export volumes is evident. According to the International Energy Agency, in April 2026, Saudi Arabia's total crude exports averaged 4.2 million barrels per day, a notable decline from 7.3 million barrels per day in February 2026. This substantial reduction in export volumes directly curtails the demand for oil tanker services, thereby impeding the growth of the Saudi Arabian oil tanker market by diminishing the available cargo for transport. The volatility introduced by these geopolitical factors creates an unpredictable operational landscape, impacting long-term investment and capacity planning within the market.

Key Market Trends

Adoption of dual-fuel and LNG-powered tankers to advance decarbonization

The adoption of dual-fuel and LNG-powered tankers represents a significant trend in the Saudi Arabia oil tanker market, driven by increasing environmental regulations and the global push for decarbonization within the maritime industry. This shift aims to reduce greenhouse gas emissions and improve operational efficiencies through cleaner fuel alternatives. For instance, ADNOC Logistics & Services took delivery of "Al Sadaf," the fourth of six new-build LNG carriers with advanced dual-fuel main engines, in December 2025, with the remaining two scheduled for delivery in the first half of 2026. This trend reflects the commitment of major players to invest in environmentally compliant vessels, positioning the fleet for future international shipping standards and potentially offering operational cost advantages.

Diversification of routes and sovereign fleet expansion to strengthen strategic independence

Concurrently, the diversification of maritime routes and sovereign fleet development is another pivotal trend, enhancing Saudi Arabia's strategic independence and logistical resilience. This involves expanding the national carrier's capacity and reach beyond traditional crude oil transport, reducing reliance on third-party operators, and securing trade lines. For example, Saudi shipping company Bahri announced plans in October 2025 to nearly double its fleet by adding more than 90 vessels over the next decade, including very large crude carriers and bulk cargo carriers. This strategic expansion enables the Kingdom to better manage its own seaborne trade, explore new commercial opportunities in varied cargo types, and reinforce its position as a global logistics hub.

Segmental Insights

Drivers of Heavy-Duty Tanker Growth in Saudi Arabia

The Heavy Duty segment is experiencing rapid growth within the Saudi Arabia Oil Tanker Market, primarily driven by the nation's steadfast commitment to its role as a principal global oil exporter. This expansion is fueled by the necessity for high-capacity vessels capable of transporting substantial volumes of crude oil and refined products over long distances to international markets. Furthermore, strategic investments in maritime logistics infrastructure, alongside increased crude oil production and refinery outputs, create sustained demand for efficient bulk transportation. Geopolitical dynamics, including the strategic rerouting of shipments via Red Sea ports like Yanbu, as managed by entities such as Saudi Aramco, also underscore the critical role of heavy-duty tankers in ensuring uninterrupted global energy supply.

Regional Insights

Eastern region dominates the oil tanker market through concentrated hydrocarbons and export infrastructure

The Eastern region leads the Saudi Arabia Oil Tanker Market due to its unparalleled concentration of hydrocarbon resources and extensive export infrastructure. This province is home to most of the Kingdom's major oil fields, including the Ghawar Field, the world's largest onshore oil field, and the Safaniya Field, the world's largest offshore oil field. Consequently, the Eastern region hosts critical export terminals like Ras Tanura, recognized as the world's largest oil port, which handles a significant portion of the Kingdom's hydrocarbon exports, and also includes key ports such as Jubail. These strategically located ports along the Arabian Gulf provide direct access to vital international shipping routes, including the Strait of Hormuz. This robust infrastructure, managed by Saudi Aramco, the national oil company, facilitates the high-volume transportation of crude oil and refined products, especially to major Asian markets, thereby cementing the Eastern region's dominance.

Recent Developments

-

In October 2025, Bahri announced plans to substantially expand its fleet, with a strategic objective to nearly double its current vessel count. As part of this initiative, the company intends to acquire 20 Very Large Crude Carriers (VLCCs) from International Maritime Industries (IMI) for delivery between 2029 and 2030. This collaboration with IMI, a joint venture partly owned by Bahri and Aramco, represents a significant new product launch for the Saudi Arabia Oil Tanker Market. The expansion is designed to enhance Bahri's share of the nation's oil trade and reinforce its global leadership in VLCC operations.

-

In October 2025, Bahri renewed its long-term contract of affreightment with S-Oil Corporation, a major South Korean refiner. This 10-year agreement ensures that Bahri will continue to transport crude oil cargoes on its Very Large Crude Carriers (VLCCs) from the Arabian Gulf and the Red Sea to Onsan, South Korea. The collaboration is expected to facilitate the movement of a minimum of 70 million barrels of crude oil annually, providing predictable revenue streams for Bahri and solidifying its fleet utilization within the Saudi Arabia Oil Tanker Market.

-

In April 2025, Saudi Aramco announced the discovery of 14 new oil and natural gas sites across Saudi Arabia's Eastern Province and the Empty Quarter. This breakthrough in exploration included six new oil fields, four natural gas reservoirs, two standalone gas fields, and two additional oil reservoirs. The combined initial production from these new oil fields and reservoirs was reported at 8,126 barrels per day of Arabian light and heavy crude. These discoveries are crucial for sustaining Saudi Arabia's energy leadership and enhancing operational flexibility, directly impacting the future supply for the Saudi Arabia Oil Tanker Market.

-

In August 2024, Bahri, Saudi Arabia's national shipping company, finalized a significant $1 billion deal to acquire nine Very Large Crude Carriers (VLCCs). This strategic fleet expansion, with deliveries anticipated to extend into the first quarter of 2025 and the final vessel received by Q3 2025, directly enhances Bahri's capacity within the Saudi Arabia Oil Tanker Market. The new tankers are equipped with advanced technologies, including eco-scrubbers and cost-efficient designs, underscoring the company's commitment to modernizing its fleet and prioritizing sustainable operations. This acquisition further solidified Bahri's position as a leading global VLCC owner.

Key Market Players

- Al Futtaim Tanker

- Al Naboodah Tanker

- United Motors Tanker

- Al Jaber Tanker

- Bin Laden Tanker

- Al Rajhi Tanker

- Manlift Tanker

- Local Tanker Companies KSA

- Volvo Tanker KSA

- Scania Tanker KSA

|

By Type

|

By Capacity

|

By Material

|

By Region

|

- Light Duty

- Medium Duty

- Heavy Duty

|

- Less than 10

- 000L

- 10

- 000L - 20

- 000L

- 20

- 000L - 30

- 000L

- and Above 30

- 000L

|

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Oil Tanker Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Oil Tanker Market, By Type:

-

Light Duty

-

Medium Duty

-

Heavy Duty

-

Saudi Arabia Oil Tanker Market, By Capacity:

-

Less than 10

-

000L

-

10

-

000L - 20

-

000L

-

20

-

000L - 30

-

000L

-

and Above 30

-

000L

-

Saudi Arabia Oil Tanker Market, By Material:

-

Saudi Arabia Oil Tanker Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Oil Tanker Market.

Available Customizations:

Saudi Arabia Oil Tanker Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Oil Tanker Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com